Yields, stocks and Gold

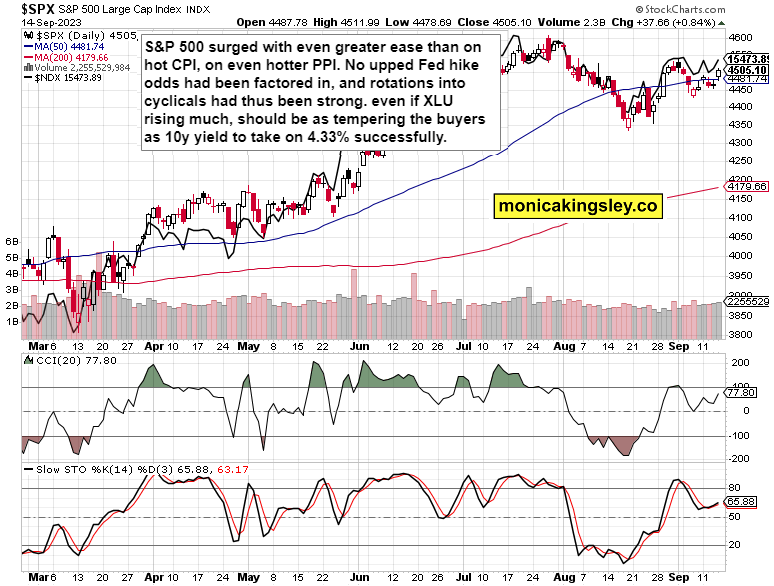

PPI brought about even more risk-on SPY move than CPI – markets disregarded how hot it came, and assigned no higher odds to Fed tightening. The focus looks to be on no Sep hike, and it requires stronger than expected incoming data to dial back the too easy Fed miscalculation, such as this Empire State manufacturing did. 4,562 daily top call turned out true, and more of a slow grind higher premarket, is being sharply reversed.

It‘s now simply about how much the daily rise in yields (stock market selloff to dampen the advance via safe haven bid coming to Treasuries) – as yields are doing now tightening for the Fed – would sink Nasdaq, followed by cyclicals and value, as these two held up yesterday (strong rotations) extraordinarily well, As said yesterday, with more evidence of inflation in the pipeline, Fed would be hard pressed not to act later this year, with bearish risk taking consequences.

Let‘s move right into the charts (all courtesy of www.stockcharts.com) – today‘s full scale article contains 3 of them.

S&P 500 and Nasdaq Outlook

4,532 turned support, and will be no small feat overcoming it today. 4,550s shouldn‘t though be overcome on a closing basis – even on this quad witching day. If momentum picks up, 4,515 isn‘t out of the question.

Gold, Silver and Miners

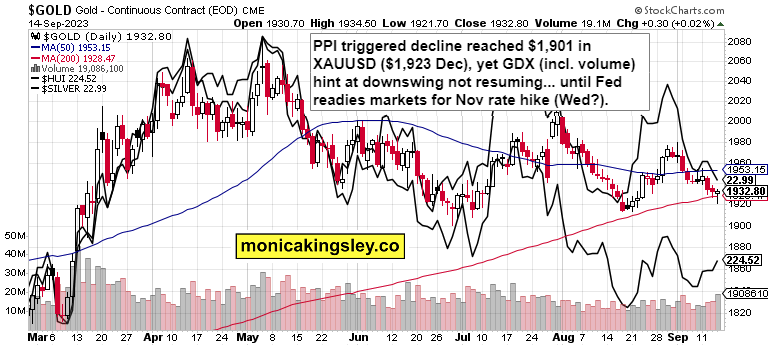

Gold turned that trouble around, and GDX offered a glass-half-full view in the end. Especially today it‘s been ignoring rising yields, also concentrating on upcoming Wednesday. High odds are that sub $1,920 targets have been cancelled by today‘s action, and $1,960 retest looms.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.