Why the COVID-19 recovery in Europe could be short-lived

On Friday, the Eurozone will be cheered up by a massive third-quarter growth figure, indicating that the rebound from lockdown has caused GDP to soar. Unfortunately, this is all old news in the fast-paced Covid-19 economy. The second wave of the virus and new restrictive measures risk putting the eurozone recovery into reverse.

Alarm bells are ringing

The second wave of the coronavirus has reached almost every corner of the eurozone and the first round of new restrictive measures has been put in place. While the third quarter was still focused on rapid economic recovery from the March-April lockdowns, the question now is whether the economy's going into reverse on the back of the new restrictions aimed at tackling the virus. As those measures become more strict, that prospect is looking increasingly likely.

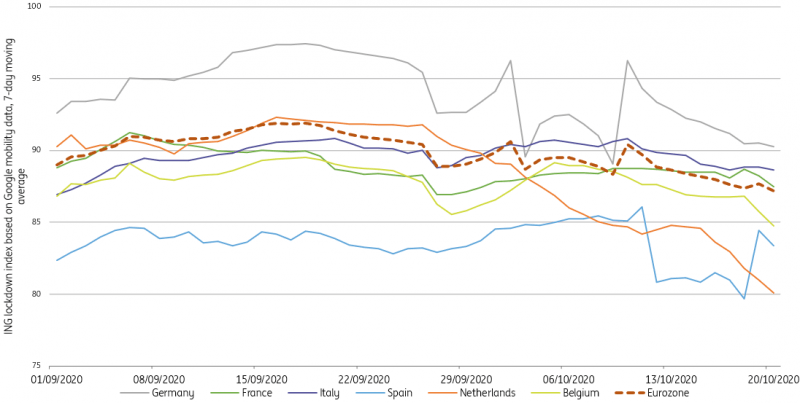

At least for now, the second wave has not had nearly as much of an impact on mobility as the first did. Yes, our index-tracking based on Google data which looks at daily visits to retail and recreation, workplaces and groceries and pharmacies has clearly peaked and is trending down, but only very modestly so far. The index peaked on September 18 at 91.9, which indicates a level of activity about 9% below the pre-corona average and has since dropped to 87.2. Still, it's far above the low of 42.5 seen during the lockdown months.

Make no mistake though, alarm bells should be going off as this gives a strong indication that the recovery is being interrupted by the second wave. The declines since September 18 have been strongest in the Netherlands as our index dropped by 13% in mobility. With data up to October 20, this includes the first effects of the latest measures taken.

Mobility is decreasing again as the second wave hits

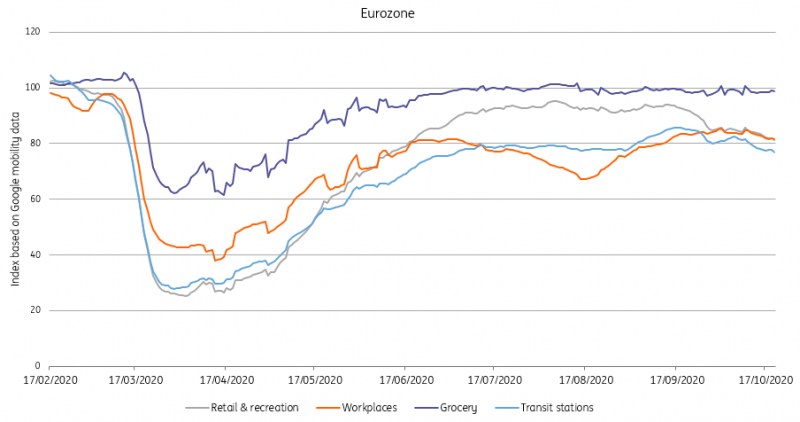

The fact that mobility did not see much of a decline until mid-October despite new restrictive measures being announced is also because the measures so far have been relatively mild. In fact, most restrictions could be labelled as a ‘smart' lockdown or a ‘recreational' lockdown. Fewer people allowed to come together, more restrictions on visiting sports matches and cultural activities and restaurants and bars closing earlier or shut down altogether have been common announcements in recent weeks.

Only Ireland has so far made the more radical steps to move back into a more or less full lockdown. The ‘recreational' lockdown is also reflected in the Google mobility data with, on average, daily visits to retail and recreation sites currently 13% below their post-lockdown peak with other indicators trending much closer to their September peaks.

The decline in activity has been largest for retail and recreation

Chances of a drop in eurozone GDP are increasing

Looking beyond Q3 GDP data, the latest restrictions have clearly increased the risk of weakening economic activity, at least in parts of the service sector. At the same time, however, the manufacturing sector could keep some of its positive momentum going into the fourth quarter, given the lagged start after the lockdowns and the continuing strength of the Chinese rebound.

As policymakers currently try to tackle the virus with smarter or more tailor-made restrictions, the adverse impact on the eurozone could also be milder. That said, given the exponential spread of the virus, the risk that additional measures will follow on top of those recently announced is high. With it, the chances of a drop in eurozone GDP in the fourth quarter are increasing too. A double-dip in the fourth quarter is becoming more of a realistic scenario by the day.

Read the original analysis: Why the COVID-19 recovery in Europe could be short-lived

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.