There have been a series of booms and busts in the world economy over the past decade, involving real and financial assets. One of the most important ones has not garnered the same headlines as some others but could be very consequential for several emerging markets. And the consequences could ripple out from there.

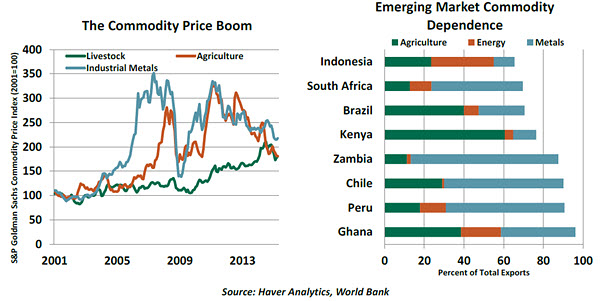

Commodity prices rose dramatically beginning in the early 2000s, a trend that was interrupted only briefly by the global financial crisis. Adfjusted for inflation, average prices for energy and base metals were three times higher in 2011 than they were 10 years previous, reaching or surpassing the peak levels of the past 50 years. While remaining below highs reached in the 1970s, food and agricultural raw material prices also rose markedly over the past decade.

Many analysts have attributed these elevated commodity prices to growth in the Chinese economy, and rightfully so. Chinese industry and consumers have demanded increasing amounts of everything from copper and iron ore to soy beans and milk. Yet China is not the sole cause of the boom; commodity demand rose across a broad range of emerging markets over the past decade. Furthermore, years of underinvestment amid the low commodity prices of the 1980s and 1990s limited suppliers’ ability to rapidly increase production to meet demand.

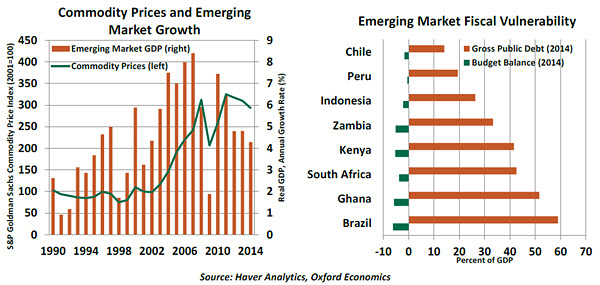

The economic windfall produced by record-high commodity prices was particularly large in emerging markets. Average annual real gross domestic product (GDP) growth for emerging markets was 2.9% higher during 2000-2014 compared with 1980-1999. In some countries, the revenue windfall was used judiciously to limit debt. But in others, spending accelerated as if the windfall were more permanent than temporary.

Prices for metals and agricultural products began weakening in 2011. Recent prices for these commodity groups are down between 30% and 50% from their peaks of four years ago. China’s growth deceleration is only part of the picture. In fact, volumes for many of China’s main commodity imports continue to rise. Ample global supply is now a significant factor, as investment during the boom years has come online.

These developments have led analysts to declare the end of the commodity boom. That declaration may be overdone, as prices for many commodities remain significantly elevated compared to historical levels. However, moderation is the new normal for emerging market commodity exporters.  With lower commodity prices, real GDP growth slows, credit growth decelerates, external balances deteriorate, fiscal balances weaken and real effective exchange rates depreciate. Those who rely more on commodities will clearly experience outsized impacts. However, the type of commodity is also a key factor. Historically, the pro-cyclical behavior is more pronounced for energy and metal exporters as compared with exporters of food and agricultural raw materials due to particularly inelastic demand for clothing and nourishment.

With lower commodity prices, real GDP growth slows, credit growth decelerates, external balances deteriorate, fiscal balances weaken and real effective exchange rates depreciate. Those who rely more on commodities will clearly experience outsized impacts. However, the type of commodity is also a key factor. Historically, the pro-cyclical behavior is more pronounced for energy and metal exporters as compared with exporters of food and agricultural raw materials due to particularly inelastic demand for clothing and nourishment.

Exchange-rate regimes can either accentuate or reduce the cyclical effects of commodity price swings. Under pegged exchange-rate regimes, output growth falls more sharply during downswings, as the exchange rate cannot fall enough to keep a country’s commodity exports competitive. Venezuela and Argentina are examples of countries that operate fixed exchange-rate regimes.

Increasing spending, enhanced subsidies or tax cuts implemented during boom years can add pro-cyclicality to commodity shifts. When commodity prices fall, governments must increase tax rates and cut spending in order to prevent fiscal deterioration. Brazil’s current and painful fiscal adjustment is a prime example of this type of pro-cyclical fiscal policy.

Other countries have adopted more enlightened fiscal measures. Under a structural surplus rule, commodity revenues are saved during boom periods and spent during periods of low prices. Both Chile and Norway operate with this type of fiscal policy rule, to name two. In practice, most economies operate somewhere in between.  Given these dynamics, lower commodity prices leave leaders and policymakers in emerging markets with the choice between popularity and fiscal sustainability. This is particularly challenging, given rising middle class demands for better governance and higher quality of public services like education, transportation, and security – implying greater public expenditure.

Given these dynamics, lower commodity prices leave leaders and policymakers in emerging markets with the choice between popularity and fiscal sustainability. This is particularly challenging, given rising middle class demands for better governance and higher quality of public services like education, transportation, and security – implying greater public expenditure.

When good times are rolling, it can be very tempting to assume that they will continue onward and upward. But the lesson of the commodity price correction is one of prudence. Commodity countries with open exchange rates and stronger fiscal positions will fare better in avoiding economic and political crisis in the coming years. But others may be facing a bitter harvest of bad policy.

Are Central Banks Fund Managers?

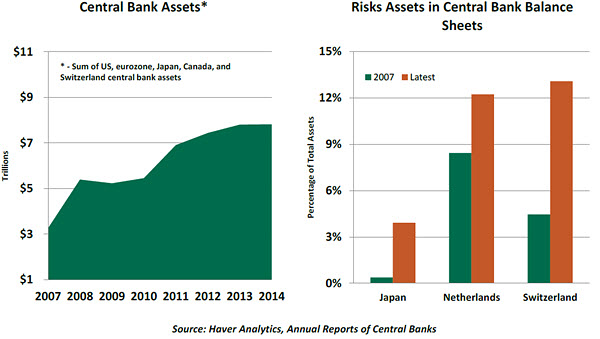

Central banks around the world have been the center of controversy since the financial crisis, with tiny interest rates and massive quantitative easing programs the norm across many countries. But in recent weeks, central banks have come under scrutiny for a different reason.

At the end of April, the Swiss National Bank (SNB) announced a US$32 billion loss for the first quarter. This came as a bit of a surprise; few are accustomed to think of central banks as making or losing any significant amounts of money. When the details behind the loss emerged, perceptions changed.

Central bankers reputedly are risk-averse. Their balance sheets are typically composed of highly liquid government securities, which are held until maturity. But the Swiss experience has exposed the fact that some central banks also hold equities and other risk assets. The 2014 report from the Official Monetary and Financial Institutions Forum, a research advisory group, noted that some central banks purchased significant amounts of publicly traded equities recently.

The Federal Reserve and Bank of England are not permitted to purchase equities directly, but the Japanese, Swiss and Dutch central banks (among others) have engaged in asset management approaches inclusive of equities. The State Administration of Foreign Exchange, a wing of the People’s Bank of China, is one of the largest holders of foreign equities in its portfolio. The increasing share of equities in central bank portfolios in the past seven years leaves us thinking about its ramifications.

Critics and advocates present compelling arguments about a central bank portfolio strategy that includes equity holdings. Some note that the low-interest-rate situation is a catalyst for ownership of equities, and they frame their argument by comparing central bankers with private-sector asset managers hunting for returns in a low-yield environment. But central bankers are not in the business of maximizing returns, and they have more room for error because of their ability to fund themselves almost indefinitely.

Countries without deep risk-free asset markets view domestic and foreign equities as alternatives. Central banks with charters to maintain exchange rate pegs are often forced to purchase significant amounts of assets not denominated in their home currency, which can create significant foreign exchange risk.

Despite these economic rationalizations, there are several pitfalls to central banks owning equities. First, central banks are answerable to taxpayers, and noticeable losses from equity holdings are likely to result in political backlash.  Second, central banks will eventually need to explain not only capital losses from equity holdings but also the selection of particular equities. The SNB holds 13% of its assets as foreign equities. A fair question is whether a central bank’s selection of shares or passive index funds renders it culpable of playing favorites in the marketplace.

Second, central banks will eventually need to explain not only capital losses from equity holdings but also the selection of particular equities. The SNB holds 13% of its assets as foreign equities. A fair question is whether a central bank’s selection of shares or passive index funds renders it culpable of playing favorites in the marketplace.

Third, a strategy to hold equities can muddy the monetary policy mission. Central bankers are mandated to maintain financial stability directly or indirectly. As large investors, they have the potential to move markets when they change the composition of their portfolios. In other words, their actions related to equity transactions may result in market movements that can undermine the financial stability objective.

While the Federal Reserve does not hold equities, it may have a variant of the issues facing central banks with risk assets in their portfolios. The Fed currently holds nearly $1.8 trillion of mortgage-backed securities, which have favored housing over other industries. And when interest rates begin to rise, the significant gains that have stemmed from the Fed’s holdings may begin to reverse. Such an event could create political stress and heighted calls for more checks on the Fed’s independence.

The SNB’s loss should be taken with a grain of salt. It resulted from a mark-to-market of the portfolio, not from losses realized in the marketplace. Most central banks are buy-and-hold investors and are in a position to wait for values to recover.

However, recent events have called into question the perception that central bankers are conservative and that their sole purpose is to manage interest rates. And with their balance sheets growing, these issues are not going away.

Australia: Reducing the Froth in the Real Estate Market

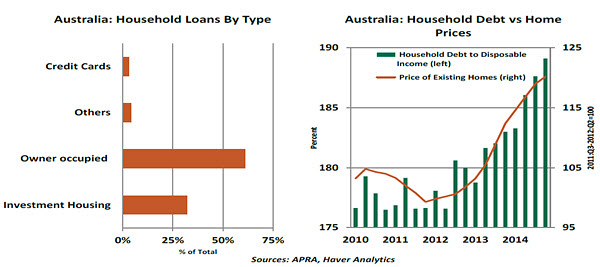

It is becoming increasingly difficult to look at the Australian real estate market and argue that it does not bear the hallmarks of a bubble. An analysis of the situation — and what authorities are trying to do about it — serves as a global case study.

As with other markets, low interest rates, positive net migration and low vacancy rates have encouraged the boom. However, the downside risks such as slow wage growth, rising unemployment and high household debt-to-disposable income ratios are pushing authorities to intervene in hopes of reining in price and credit growth.

Of the three types of borrowers – owner-occupiers, domestic investors and foreign investors – the latter two are causing most of the price runup, as owner-occupiers are priced out of the market. With the central bank easing to promote domestic demand, responsibility for slowing demand has fallen elsewhere.  The financial regulator has taken aim at domestic investors by imposing a currently unheeded 10% credit growth speed limit on investment housing loans. Following the discovery of disparities in underwriting standards, macroprudential measures including increased capital requirements are expected; however, the regulator has indicated that new measures will likely be targeted and confidential.

The financial regulator has taken aim at domestic investors by imposing a currently unheeded 10% credit growth speed limit on investment housing loans. Following the discovery of disparities in underwriting standards, macroprudential measures including increased capital requirements are expected; however, the regulator has indicated that new measures will likely be targeted and confidential.

Meanwhile, the federal government is tackling foreign investors (anecdotally Asian buyers) by stiffening penalties for those caught violating the prohibition on foreigners buying existing dwellings. The government faces an uphill battle to stem demand, with Chinese demand for property in Sydney and Melbourne accounting for more than 20% of new supply, and their investment in the overall market totaled AUD 12.4 billion in 2014. Similar to Singapore and the state of Victoria, the government could resort to imposing additional stamp duties on foreign buyers.

Despite the signs of stress, the Australian market fundamentally differs from the pre-crisis U.S. market. All loans are full-recourse, and there is not a large supply overhang. The most likely conclusion to the cycle will be a flattening rather than a crash in prices. But other markets may face greater imbalances and, therefore, a greater risk of a worst-case outcome.

Recommended Content

Editors’ Picks

EUR/USD holds above 1.0700 after German inflation data

EUR/USD trades modestly higher on the day above 1.0700. The data from Germany showed that the annual HICP inflation edged higher to 2.4% in April. This reading came in above the market expectation of 2.3% and helped the Euro hold its ground.

USD/JPY recovers above 156.00 following suspected intervention

USD/JPY recovers ground and trades above 156.00 after sliding to 154.50 on what seemed like a Japanese FX intervention. Later this week, Federal Reserve's policy decisions and US employment data could trigger the next big action.

Gold holds steady above $2,330 to start the week

Gold fluctuates in a relatively tight channel above $2,330 on Monday. The benchmark 10-year US Treasury bond yield corrects lower and helps XAU/USD limit its losses ahead of this week's key Fed policy meeting.

Week Ahead: Bitcoin could surprise investors this week Premium

Two main macroeconomic events this week could attempt to sway the crypto markets. Bitcoin (BTC), which showed strength last week, has slipped into a short-term consolidation.

Five Fundamentals for the week: Fed fears, Nonfarm Payrolls, Middle East promise an explosive week Premium

Higher inflation is set to push Fed Chair Powell and his colleagues to a hawkish decision. Nonfarm Payrolls are set to rock markets, but the ISM Services PMI released immediately afterward could steal the show.