Five Fundamentals for the week: Fed fears, Nonfarm Payrolls, Middle East promise an explosive week

- Higher inflation is set to push Fed Chair Powell and his colleagues to a hawkish decision.

- Nonfarm Payrolls are set to rock markets, but the ISM Services PMI released immediately afterward could steal the show.

- Ceasefire negotiations in the Middle East and reverberations from Japan's perceived currency intervention add to the action.

April ends with a bang in the Japanese Yen – and May kicks off with the world's most powerful central banker taking the stage. In a turbulent week, several key scheduled events and also crossing headlines are to watch out for. Here are five fundamentals for the week:

1) Yen intervention reverberations

Over 500 pips have shifted on Japanese Yen (JPY) crosses within hours on Monday – in what seems like an intervention to strengthen the Yen. A bank holiday in Japan meant lower liquidity and extra hours for officials at the Ministry of Finance in Tokyo.

Where next for the Yen from here? Near-zero interest rates in Japan hobble any efforts to shore up its value, but several moves in markets may burn some speculators, potentially leading to a bet in favor of the battered currency.

Action in the Yen is not only the best show in currency town, but has implications for broader markets. If the Bank of Japan is eventually forced to raise rates to buoy the currency, others could follow. If intervention eventually succeeds, other central banks would also consider it.

The biggest test is the Federal Reserve's decision. Unless the Fed surprises with a dovish twist – extremely unlikely – the lights in Tokyo will be up for long hours, and action in the Yen will remain in focus.

2) Middle East at a crossroads

Are Israel-Hamas negotiations close to a breakthrough? The row between two Israeli ministers about a deal whose details are unclear is evidence that talks are making some progress.

Any ceasefire – even if it lasts for only six weeks – would substantially reduce the odds for a regional war with implications on global trade. Yemen's Houthis will likely stop attacking commercial ships in the Red Sea and clashes between Iran and Israel would return to the shadows.

A ceasefire would hurt Oil, as the risk of disruptions would diminish, and also Gold, which has benefited from tensions since Hamas attacked Israel on October 7. It would be good news for stocks.

However, talks could fizzle – as they have in recent months. In case the status quo continues, Oil and Gold would enjoy a bump up, without major moves.

In case talks break down in anger and Israel carries out its plan to invade Rafah, there are greater chances for the war to expand. Fighting in the overcrowded southernmost town in Gaza could push Iranian-backed militias to more action. In such a scenario, Oil and Gold would gain while stocks would struggle.

3) Hawkish pivot at the Fed

Wednesday, 18:00 GMT. No longer a bump in the road – that was Federal Reserve Chair Jerome Powell's message in his latest remarks about inflation. The Consumer Price Index (CPI) has beaten estimates three times in a row, a fact that can be ignored. But what about the Fed's favorite gauge?

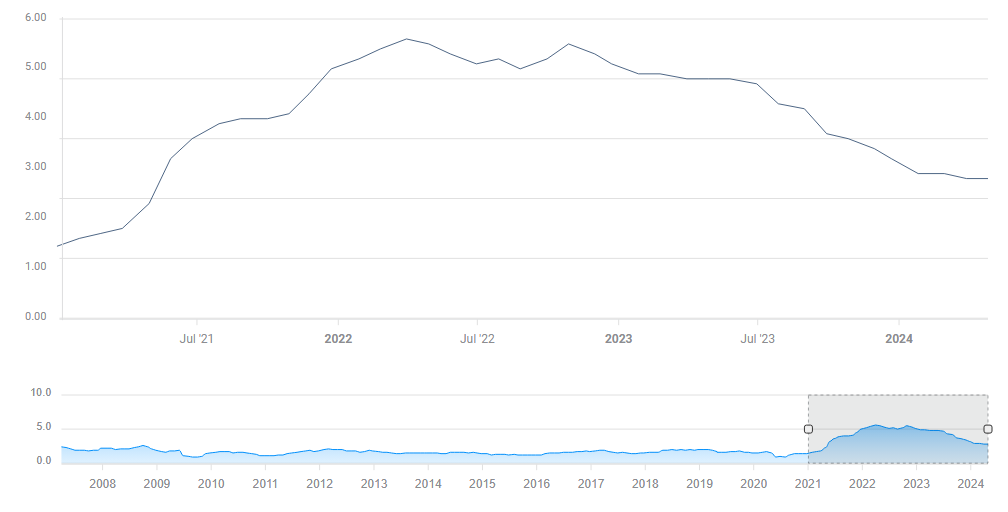

The bank focuses on core Personal Consumption Expenditure (PCE) inflation data, which uses a more flexible methodology. It has dropped, but far from enough.

Core PCE. Source: FXStreet

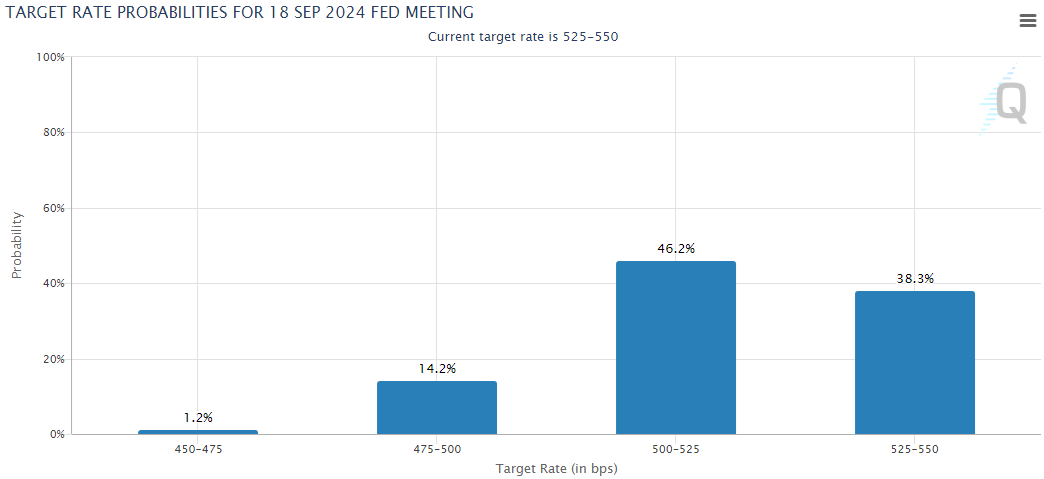

Markets expect the Fed to leave rates unchanged once again and probably to signal that a cut is off the cards for June. Will Powell at least be open to slashing borrowing costs in September? Investors would like to see it coming as early as July, but there is a higher chance of action when new forecasts are released, such as in June, September or December.

While the autumn is far, that is the next big window for the bank to act, and markets give a cut in September more chances than not.

Odds of a rate Source: CME Group

The more Powell talks about inflation, the lower the chances of a cut. If he has become worried – contrary to his previous tone in March – the US Dollar might find fresh strength while Gold and stocks suffer. A more cautious tone, giving room to nuances around core PCE and other factors, could weigh on the Greenback and boost other assets.

What about the labor market? The bank has two mandates – price stability and full employment. After last month's blockbuster Nonfarm Payrolls report showing an increase of 303,000 jobs, Powell will likely praise the current strength and move on. However, if he surprises by describing hiring as moderating, it would not only be dovish, but serve as a hint toward Friday's Nonfarm Payrolls release for April.

I expect a hawkish tone from Powell and his colleagues, aligning themselves with higher inflation. But, as I am not the only one awaiting this scenario, price action could be wild – US Dollar strength ahead of the event, in anticipation of hawkishness, and a "buy the rumor, sell the fact" afterwards.

If Powell is not extremely hawkish, markets could voice a collective sigh of relief, boosting stocks and Gold, while weighing on the Greenback.

4) Nonfarm Payrolls to defy gravity again

Friday, 12:30 GMT. Immigration is filling some of America's labor shortages – that is the best explanation for the massive expansion of the US labor market, which rarely disappoints. In the past 12 months, headline Nonfarm Payrolls missed estimates only three times, the last was in October 2023.

This time, the economic calendar shows an estimate for 243,000, the highest consensus since September 2022. Are economists too optimistic now? It is essential to note that real estimates might rise or fall in response to the ADP private-sector employment report on Wednesday, but these changes are minor.

I expect another upbeat labor market report, which will likely boost the US Dollar, hurt Gold, and have a mixed impact on stocks. Markets want a strong economy but also lower interest rates.

In case of a moderate miss, the Greenback would be the sole loser, and in the unlikely scenario of a devastating report, the US currency could benefit from safe-haven flows. The most likely outcome is a small beat.

5) ISM Services PMI to have the final word of the week

Friday, 14:00. The show is not over after the Nonfarm Payrolls. The ISM Services PMI, due 90 minutes after the NFP, has the final say, and it may unleash strong volatility. Investors hang onto forward-looking surveys and adhere to their guidance – even though they are only "soft data" and not hard evidence.

The services sector is America's largest, and inflation developments are of high interest. A small increase to 52 for the headline index is expected, a figure that would reflect slightly stronger, yet still moderate, growth. The 50-point mark separates between contraction and expansion.

The Prices Paid component could steal the show if it drops from 53.4 to below 50, indicating moderating inflation. Any increase would be worrying.

The publication of the ISM Services PMI may unleash wild volatility, as that would be the moment when all the week's figures are out. Price action would further increase if the ISM Services PMI goes in the same direction as the NFP, either beating or missing estimates.

Final thoughts

The list above focuses on five fundamentals to watch, but there are other economic indicators as well as end-of-month flows. I recommend trading with care, especially around the Fed decision, but also when it comes to the Yen or geopolitical headlines.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.