Week ahead - Fed and BoJ decide on monetary policy [Video]

-

US CPI data and Fed to determine the dollar’s fate.

-

Will the BoJ signal that another rate hike is looming?

-

Pound traders await UK employment and GDP numbers.

-

RBA hike bets shrink ahead of AU jobs and China CPI data.

![Week ahead - Fed and BoJ decide on monetary policy [Video]](https://editorial.fxstreet.com/images/Macroeconomics/CentralBanks/FED/federal-reserve-facade-7769724_XtraLarge.jpg)

Mind the dots

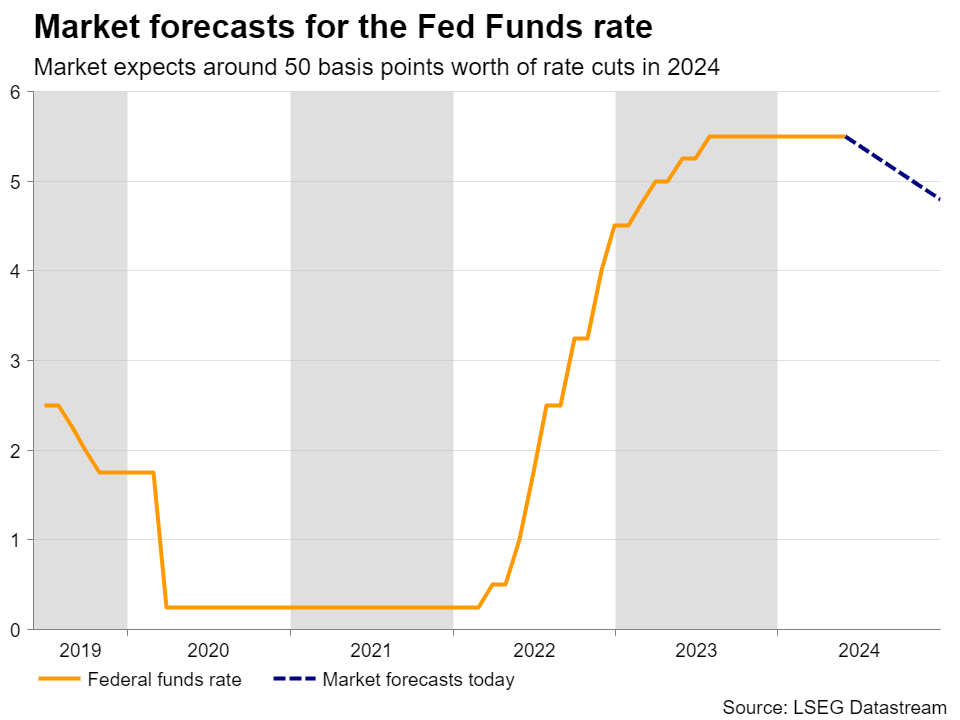

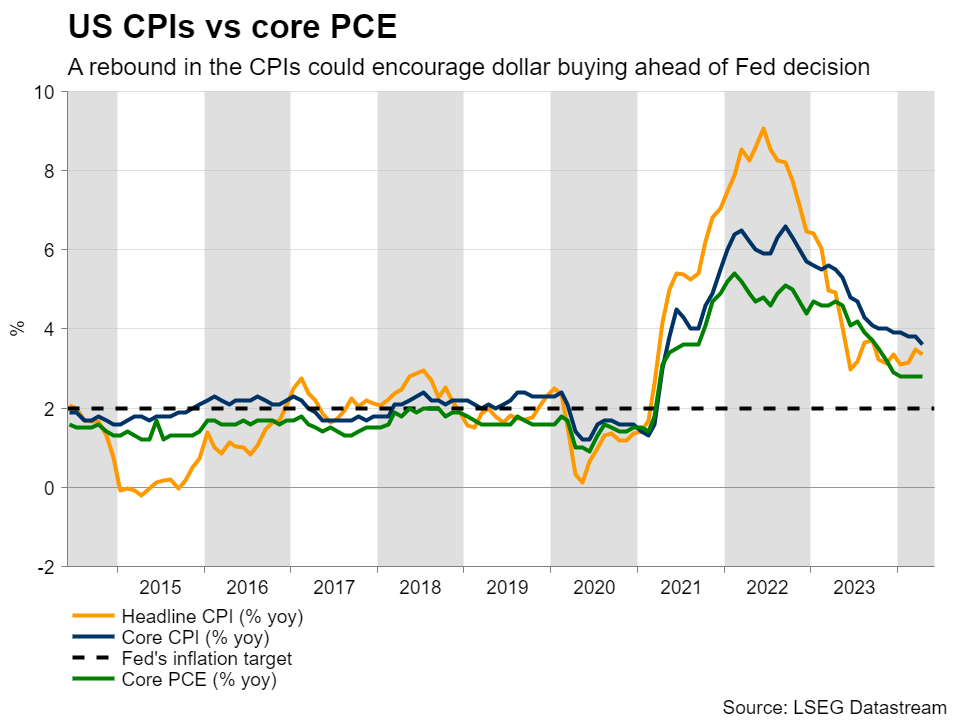

With US inflation resuming its downtrend in April and the ISM manufacturing PMI for May disappointing, investors remained convinced that the Fed will begin lowering interest rates at some point this year. Currently, they are penciling in nearly two quarter-point reductions by December, assigning around an 80% probability for the first one to be delivered in September.

Ergo, as they try to figure out when Fed officials will hit the rate cut button, traders are likely to lock their gaze on Wednesday’s FOMC decision next week. This will be one of the more significant meetings that is accompanied by updated economic projections and a new dot plot.

Bearing in mind policymakers’ ‘higher for longer’ mantra, market participants are nearly certain that the Committee will refrain from acting at this gathering. Therefore, the spotlight will fall on the statement and especially the new interest rate projections. The March plot pointed to three 25bps cuts this year and another three in 2025.

So, with most policymakers signaling that they are in no rush to start lowering borrowing costs, there is the possibility of an upward revision. Nonetheless, a median dot pointing to two rate cuts this year may not be enough to lift the dollar, as this is what the market is already anticipating. For the dollar to stage a strong recovery, the majority of Fed officials may need to signal only one quarter-point reduction for 2024.

The US CPI data for May are due to be released just a couple of hours ahead of the decision, and a set of sticky numbers could allow the dollar bulls to start the party earlier, even if the Fed decision does not meet their expectations. After all, market participants will be aware that the CPI numbers will not be incorporated into policymakers’ projections. That said, Fed Chair Powell may receive questions about the data at the press conference. The PPI figures are scheduled for Thursday.

When is the next BoJ rate hike coming?

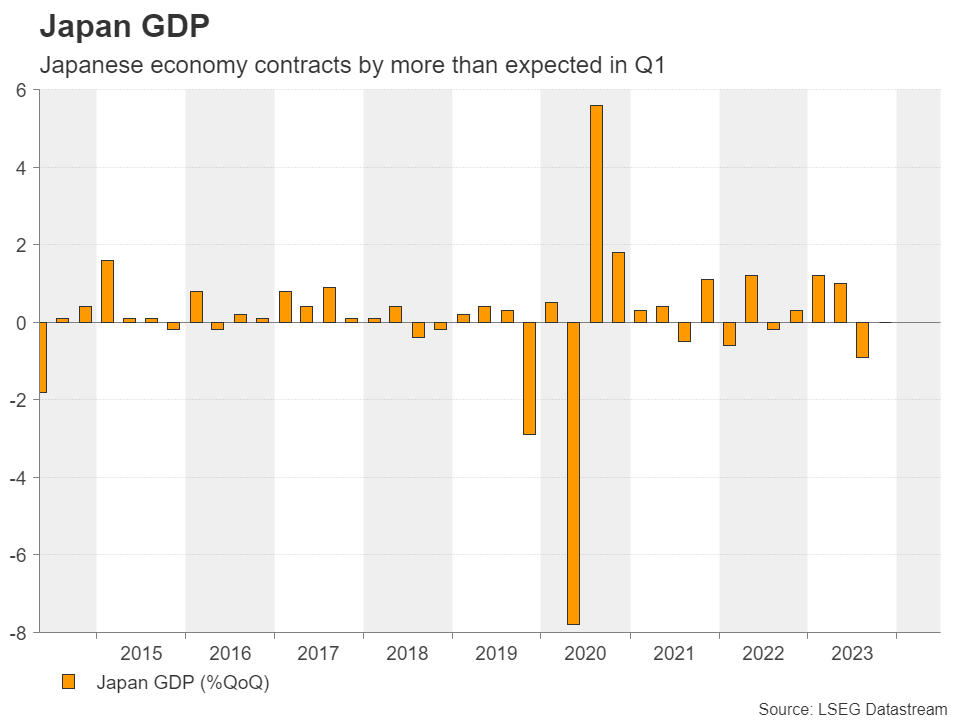

On Friday, the central bank torch will be passed to the Bank of Japan (BoJ). At its latest gathering on April 26, this Bank kept the range for its benchmark rate between 0% and 0.1% as was widely expected. Although the Bank upgraded its inflation projection, it did not signal a reduction of its bond purchases and refrained from signaling a strong intention to raise interest rates again soon. This resulted in a weakening yen and two intervention episodes by Japanese authorities in the following days.

However, the currency resumed its slide soon after the episodes, with the larger-than-expected economic contraction for Q1 putting obstacles in the road for the next rate increase. Investors are still assigning a strong 67% chance for another 10bps hike in July, but should the Bank avoid communicating that clearly, traders may get disappointed, and the yen could extend its slide and retest its recent lows.

UK jobs and GDP data to shake the pound

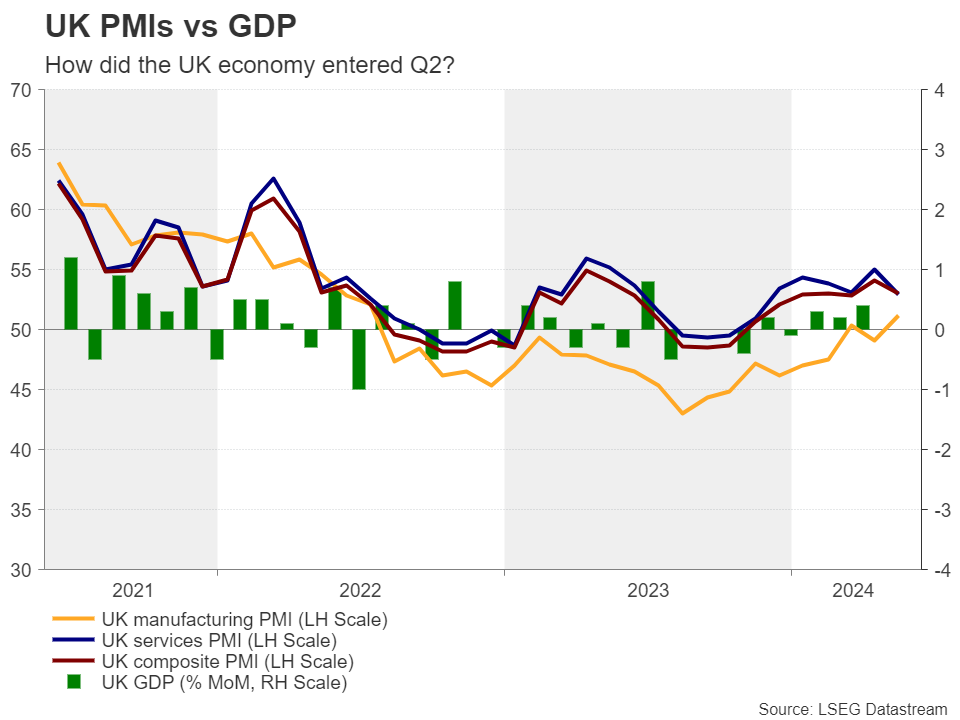

The pound is also likely to be a protagonist next week, as the UK employment report and the monthly GDP rate, both for April, are due to be released on Tuesday and Wednesday respectively.

The hotter-than-expected UK inflation numbers for April, and especially the stickiness in underlying price pressures, prompted investors to scale back their BoE rate cut bets. Currently, they are pricing in around 40bps worth of rate reductions by December, with the probability of a first quarter-point cut in September resting at around 65%.

Another month of elevated wage growth and a GDP figure corroborating the view that the UK economy entered Q2 on a solid footing may lessen the September probability and thereby help the pound trade higher.

Nonetheless, with general elections scheduled for July 4, pound traders may become more careful closer to that date. The Labor party has been portraying itself as the party of fiscal responsibility and thus, if they win, they could make the BoE’s work easier, allowing it to cut interest rates much earlier than currently expected.

China inflation, AU jobs, EU elections

Elsewhere, China’s CPI and PPI numbers are scheduled for Wednesday, while Australia’s employment report is due out on Thursday.

Although Australia’s weaker-than-expected GDP data for Q1 eliminated the few bets about a rate hike by the RBA, the Australian central bank is still seen as one of the most hawkish among the major ones, as investors seen only a 50% chance for a quarter-point reduction by the RBA this year.

Thus, a rebound in Australia’s employment combined with hotter-than-expected Chinese inflation may allow the aussie to trade higher as investors become more confident that the RBA is unlikely to press the cut button this year.

It is also worth mentioning that this Sunday is the last day of the EU Parliamentary elections. Although the outcome may not be a game changer for financial markets, a surge in right-wing support could make it more difficult for lawmakers to agree and push through reforms and policies that give the EU more power. This could weigh somewhat on the euro.

Author

Charalampos joined the XM Investment Research department in August 2022 as a senior investment analyst.