Week ahead: Data from the US, UK and Canada in focus

It was quite the week!

Top of the bill last week, of course, was the stronger-than-expected US CPI inflation print, which, immediately following the release, underpinned the dollar and US Treasury yields, as well as pushed spot gold (XAU/USD) and US equity index futures southbound. Interestingly, a hawkish repricing in the Fed funds target rate was also seen, dropping from -70bps of easing priced in for the year to -45bps, as of writing. That’s less than two rate cuts now for the year, lower than the Fed’s projection of three rate cuts, according to their latest Summary of Economic Projections (SEP).

While it was indeed a hot release, all the headline and core measures for MoM and YoY, except the YoY headline CPI, were in line with the prior readings.

The FP Markets Research Team noted the following in a follow-up post:

The only outlier was nominal YoY CPI inflation, which jumped +3.5% from +3.2% prior. From this, although it is not what the Fed wants to see and does stress stickiness, it is not a release that underscores a reflationary phase just yet. The question, therefore, is whether this is still a bump in the road for the Fed’s 2.0% inflation target or something more; one thing is for certain, though, is it has made the task of choosing a timeline when to ease policy a little more complex.

Later on in the week, the European Central Bank (ECB) was pretty much a snooze, particularly the Press Conference. Markets were expecting ECB President Christine Lagarde to underscore a dovish tone, chiefly after euro area inflation demonstrated the ongoing disinflation progress prior to the event. The Press Conference Q&A largely centred around whether the ECB is Fed-dependent regarding cutting rates.

The central bank left all three key benchmark rates unchanged, as expected. However, the accompanying rate statement did offer a little something for investors to get their dovish teeth into. The FP Markets Research Team highlighted the following passage (italics) that was likely behind the immediate pop lower in the EUR against its US counterpart, particularly the sentences in bold:

The Governing Council’s future decisions will ensure that its policy rates will stay sufficiently restrictive for as long as necessary. If the Governing Council’s updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission were to further increase its confidence that inflation is converging to the target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction.

Unsurprisingly, as of this writing, the OIS curve is pricing in -81bps of easing for the year, down from around -91bps.

The Bank of Canada (BoC) and the Reserve Bank of New Zealand (RBNZ) also claimed some of the limelight last week. Both held rates steady for a sixth consecutive meeting, which was widely expected by markets and economists.

The BoC communicated that the central bank requires further evidence that inflation is slowing, though it did echo that they’re nearing the point where rate cuts are on the table. The RBNZ did not deliver much to work with, but it did communicate that policy would remain restrictive in the near term, with inflation remaining above target, thus striking more of a hawkish tone and reinforcing the New Zealand dollar (NZD).

Looking forward

UK data

In the UK, the focus will be on Tuesday’s wage/employment numbers, Wednesday’s CPI inflation and Friday’s retail sales data.

Similar to Fed and ECB pricing, swaps traders have scaled back bets of rate cuts for the Bank of England (BoE’s) Bank Rate to below 50bps for the year, with the first 25bp cut now fully priced in for September’s meeting (-33bps), but only just as July is still firmly on the table (-24bps). This was fuelled on the back of the hotter US CPI inflation print rumbling through the financial markets and, of course, BoE’s Megan Greene (a hawk) communicating in the Financial Times that ‘rate cuts in the UK should be way off’. However, while this does emphasise a hawkish take, we must consider we also recently witnessed the BoE Governor Andrew Bailey state that rate cuts were likely at future meetings.

In terms of upcoming data, current forecasts reveal that both regular pay and pay that includes bonuses will be slightly higher in the three months to February, up +6.2% (from +6.1%) and up +5.8% (from +5.6%), respectively. This will not be welcomed news at the BoE and could prompt a spike higher in the GBP and further hawkish repricing. For the March inflation report, after February’s inflation data cooled to its lowest level since late 2021 (+3.4%), expectations heading into the event imply that we could see inflation slow further to +3.1%. Finally, serving as a key gauge of consumer spending, monthly retail sales data for the UK is anticipated to print +0.2% for March, following February’s 0.0% reading.

US data

Across the pond, US data welcomes retail sales numbers on Monday, together with regional manufacturing figures on Monday and Thursday.

For headline retail sales, market expectations indicate an increase of +0.3% for the month of March, down from the +0.6% print in February. For the ex-autos measure, economists expect a +0.4% rise versus the +0.3% reading in February.

Canada data

This week’s CPI inflation number from Canada on Tuesday for March will be something the Bank of Canada (BoC) will watch closely. This release follows the central bank holding its Overnight Rate at 5.0% for a sixth consecutive meeting, citing, as underlined above, the need to see evidence of further slowing inflation before considering rate cuts. You may recall that the BoC Governor Tiff Macklem communicated that ‘we are seeing what we need to see, but we need to see it for longer to be confident that progress toward price stability will be sustained. The further decline we’ve seen in core inflation is very recent. We need to be assured this is not just a temporary dip’.

The core inflation measures are largely expected to remain unchanged, matching February’s pace.

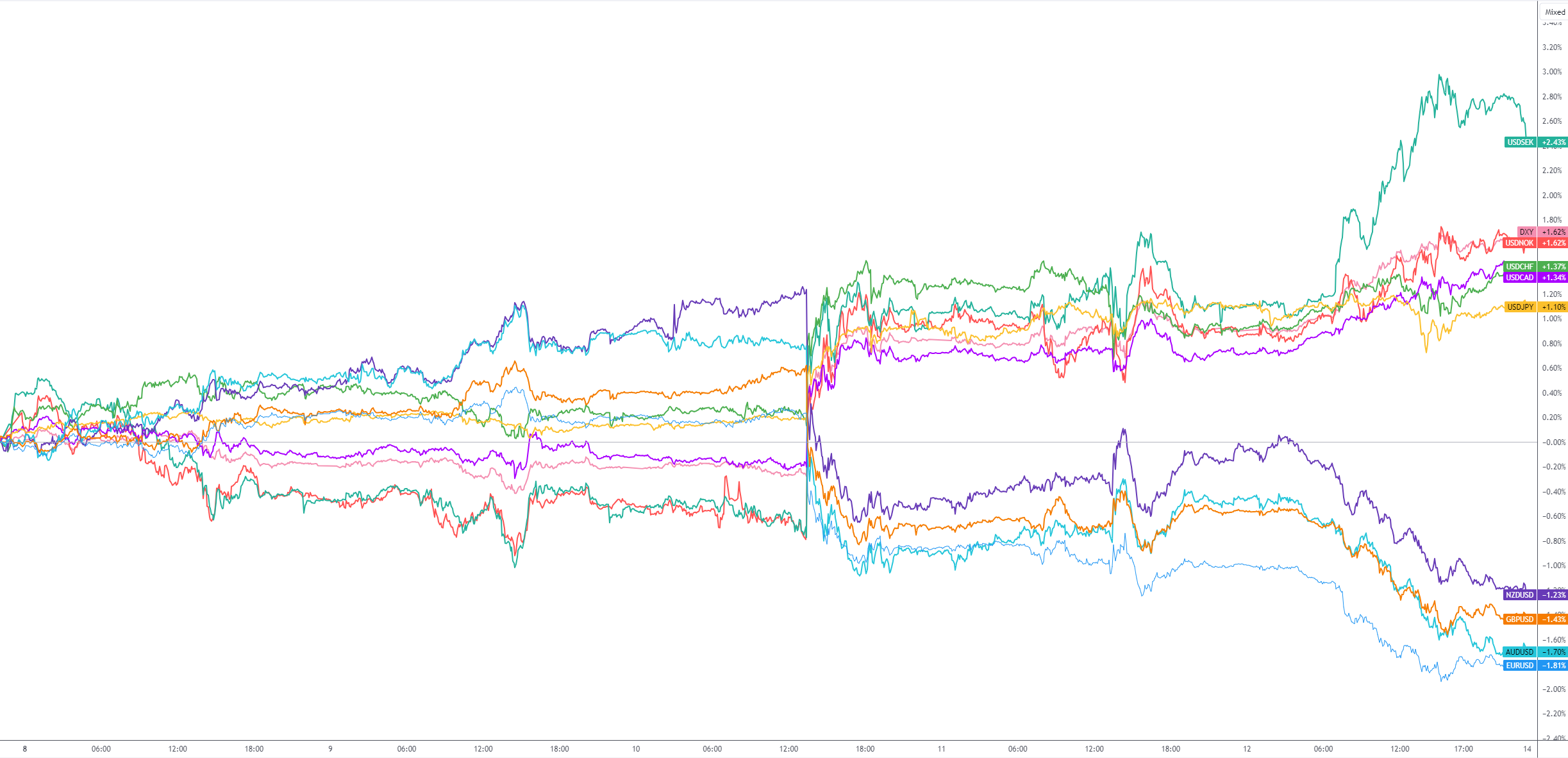

G10 FX (five-day change):

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,