We continue to smell that the Fed really does not want to leave rates on hold all year

Outlook

The calendar is chock-full this week (eurozone CPI, payrolls on Friday) but the biggie will be the Fed meeting on Tuesday and Wednesday and the degree of hawkishness perceived in Mr. Powell’s press conference, if not the post-meeting statement itself. We may have gotten the data wrong on Friday, but we can note that inflation did not worsen and in some measures, like the Dallas trimmed mean, improved a tad. On the other hand, the services did worsen.

We continue to smell that the Fed really does not want to leave rates on hold all year or even raise rates. At the same time, it has to defend its commitment to managing inflation. A pickle. One idea that crops up repeatedly is tinkering with QT but that has yet to materialize.

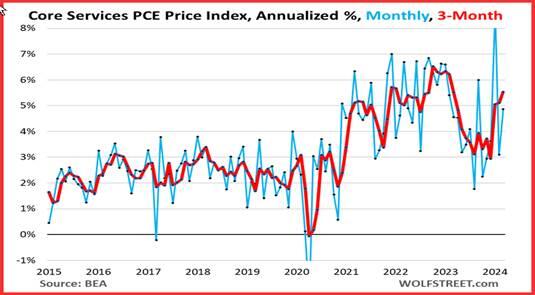

The institutional framework still favors rate cuts this year. Now we need the data to cooperate. In fact, the housing component was flat this time. But as WolfStreet points out, the core services PCE price index (ex-energy) “has been hot and is getting hotter. This is where inflation is entrenched, and where the majority of consumer spending takes place. And Fed speakers from Powell on down have pointed at this issue endlessly.

“Core services inflation had calmed down somewhat by mid-2023, but then refused to calm down further, getting stuck in the 3.5% range annualized for five months. And in January, it began spiking in a very disconcerting manner.

“The core services PCE price index jumped by 4.9% annualized In March, from February (blue). The three-month reading jumped by 5.5% annualized, the worst since February 2023.”

So the Fed may want to cut, but is struck with higher for longer until that last mile looks better.

Reasons for the Fed to Cut Rates:

Avoid embarrassment from getting inflation wrong twice.

Normalize the yield curve.

Head off any recessionary tendencies.

Help housing via mortgage rates.

Help banks rollover commercial property loans.

Help the stock market.

(Help the current White House).

Forecast: We continue to think the dollar downswing is a correction and not a reversal, but we may have to suffer to somewhere close to the 200-day in the euro (around 1.0806) before it comes to a screeching halt. This kind of heavy-duty correction is always a problem for trend-followers. When you go with the correction direction, you get punched in the head at some point. Sticking to the primary trend is safer even though it delivers losses for some days and sometimes weeks. Active traders need to go with the flow.

Intervention Tidbit: Everybody and his brother have been talking about BoJ intervention for months now. That we got the spike to the line in the sand at 160 on a Japanese holiday is very fishy. Who dunnit? Maybe a newbie, maybe an algo-driven hedge fund—but not local traders. We get a plateful of fresh data tomorrow and that could set the tone, but with Tokyo inflation falling back, implying the national will fall back too, the BoJ has little traditional cause to raise rates to fend off speculators.

Does this mean actual intervention? Japan got “permission” of sorts from G7 not to complain about currency manipulation if it does intervene. Most of the commentary today falls on the side of official intervention—but that’s a guess, not a fact. We are not so sure but have to wait nearly a month before the official data comes out. Because the timing of this move was peculiar, on a holiday, we guess the MoF/BoJ will exercise their accustomed patience. That doesn’t mean they won’t bring down the hammer at some point.

Tidbit: In Project Syndicate, the much respected El Erian outlines the Big Picture for getting better forecasts than we had last year—and they stank. The article is a bit ponderous—funny how fame does that—but worthy.

“The difficulties facing forecasters are complicated by two broader phenomena that could last for years. These can be placed in two categories: transitions and divergences. Many advanced economies have embarked on a transition from a world of deregulation, liberalization, and fiscal prudence to one oriented around industrial policy, renewed regulation, and sustained budget deficits on a scale that would have been unthinkable previously.

“Moreover, these economies’ policies are becoming more differentiated, whereas previously they represented common responses to common shocks. Internationally, globalization is giving way to fragmentation…. Moreover, some countries are much more flexible than others when it comes to adjusting factors of production and introducing policy measures to enhance productivity in the face of changing circumstances.”

Problems arise because of the upcoming wider range of outcomes. We ae not all singing the same song. But it could be okay in the end.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat