USD/CAD Weekly Forecast: Where is the Canadian optimism?

- USD/CAD posts first weekly gain in two months.

- WTI loses 5.1% on the week, 12.2% on the month.

- BOC leaves rate unchanged at 0.25%, cautions on departure from the zero bound.

The USD/CAD scored its first weekly gain in two months as a sharp drop in oil prices weighed on Canadian economic prospects and the central bank stressed that the pandemic recovery is a long term project.

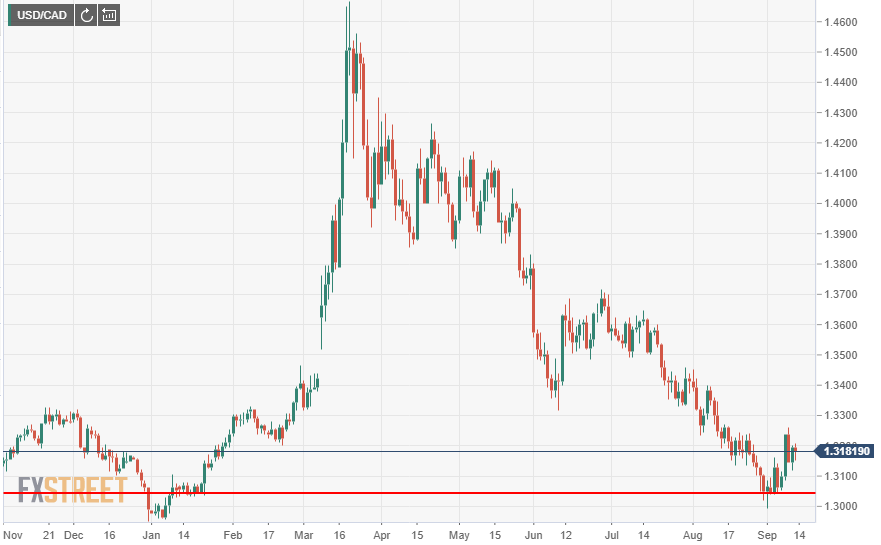

After opening at 1.3064 on Monday the USD/CAD touched 1.3260 on Wednesday after the Bank of Canada meeting, its highest since August 17 and finished at 1.3178 on Friday.

West Texas Intermediate (WTI) had started the week at $39.74 but Tuesday’s 5.8% drop with a close at $37.12, largely on demand concerns, set the stage for the remainder of the sessions with Thursday and Friday’s finishes at $37.26 and $37.66 the lowest since June 15.

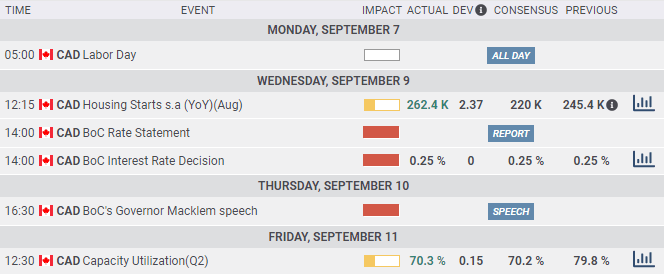

The Bank of Canada left its main interest rate unchanged at 0.25% as universally expected and maintained its quantitative easing program.

Governor Tiff Macklem noted that while the Canadian economy had had a strong recovery from the pandemic closures he expected the pace of the improvement to start to slow.

“Let me underline, it’s really very premature to start talking about exit. That’s some ways off and that’s really reflected in our decision yesterday to continue our QE program at the current pace,” Mr. Macklem said in a speech on Thursday.

The Canadian labor market has rehired almost two-thirds of the workers laid off or fired in the shutdowns of March and April. In the United States the rate is just under half.

Canadian data was sparse. Housing starts jumped to 262,400 on the year in August from 245,400 in July well ahead of the 220,000 estimate and the highest rate since September 2007 at the height of the housing bubble.

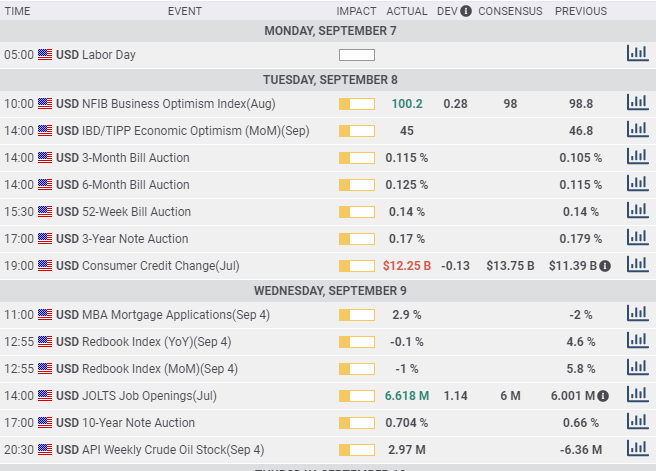

American statistics were mixed. The JOLTS job opening list for July at 6.618 million was better than 6 million forecast and June number but is still below the 7 million average for January and February. Consumer prices were firmer than forecast in August, 0.4% vs 0.3% in the overall and 0.4% vs 0.2% in core with 1.3% vs 1.2% and 1.7% vs 1.6% on the year, suggesting rising consumption.

Initial jobless claims for first week in September were worse than expected, 884,000 vs 846,000 and identical to the week before. Continuing claims rose to 13.385 million from 13.292 million, almost half a million more than the 12.925 prediction.

USD/CAD outlook

The September 1 drop to 1.2994, the first time the USD/CAD had been below 1.3000 since January 8 is beginning to look like the post-pandemic bottom. The brief foray, the lack of subsequent attempts and the firm support at 1.3040 argue that the USD/CAD has exhausted its downward momentum.

The weak US dollar scenario which was behind the general August decline in the greenback was based on the suspicion that the American economy was entering a second wave Covid retraction. Though that did not occur there has not been sufficient improvement in US statistics, particularly the still high weekly unemployment claims numbers, for a full reverse. The US economy is not retreating but it is not advancing strongly either and the indecision has infected the dollar.

Because the current level of the USD/CAD is the result of a misapprehension of the US economy the potential for a run to the 1.3400-1.3500 range of July is likely. All that is required is the cooperation of the US economy.

Canada statistics September 7-September 11

US statistics September 7-September 11

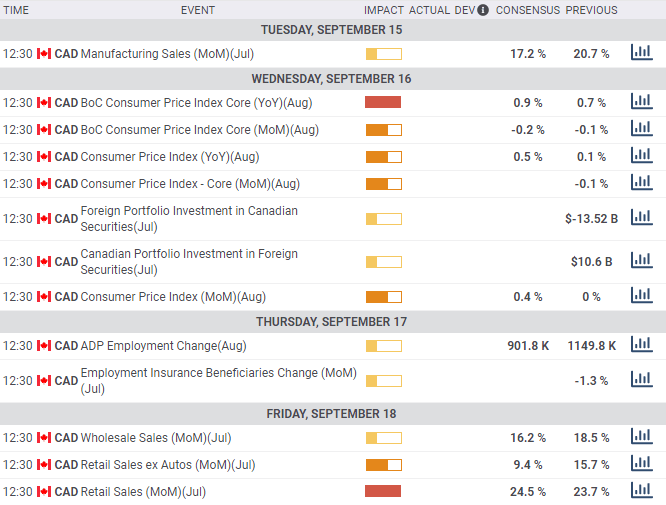

Canada statistics September 14-September 18

US statistics September 14-September 18

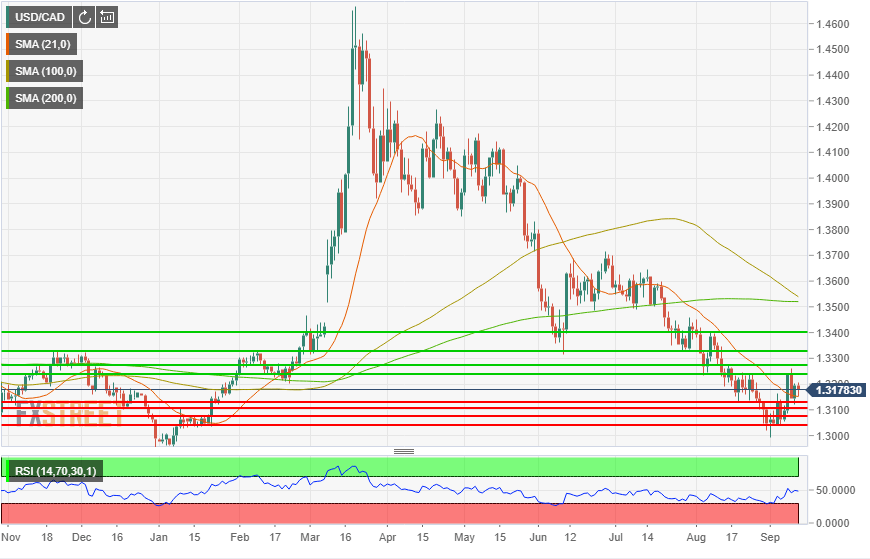

USD/CAD technical outlook

21-day moving average: 1.3151

100-day moving average: 1.3539

200-day moving average: 1.3526

Resistance: 1.3235; 1.3270; 1.3325; 1.3400

Support: 1.3130; 1.3100; 1.3075; 1.3040

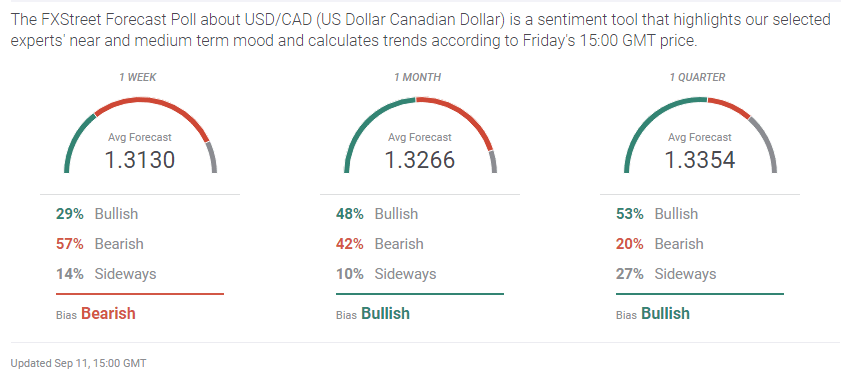

USD/CAD sentiment poll

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.