USD/CAD remains bearish ahead of Bank of Canada

The US dollar took a hit to begin the week on Monday after US President Trump issued a tweet that decried rising US interest rates amid his assessment that Russia and China are actively devaluing their respective currencies. The tweet highlighted Trump’s opposition to both foreign currency manipulation as well as a stronger US dollar, pressuring the greenback as a result. Trump’s tweet comes despite a report issued last week by the US Treasury that did not label either country as a currency manipulator. The resulting dollar tumble occurred even as data released on Monday morning detailed a strong and better-than-expected rebound for US retail sales in March.

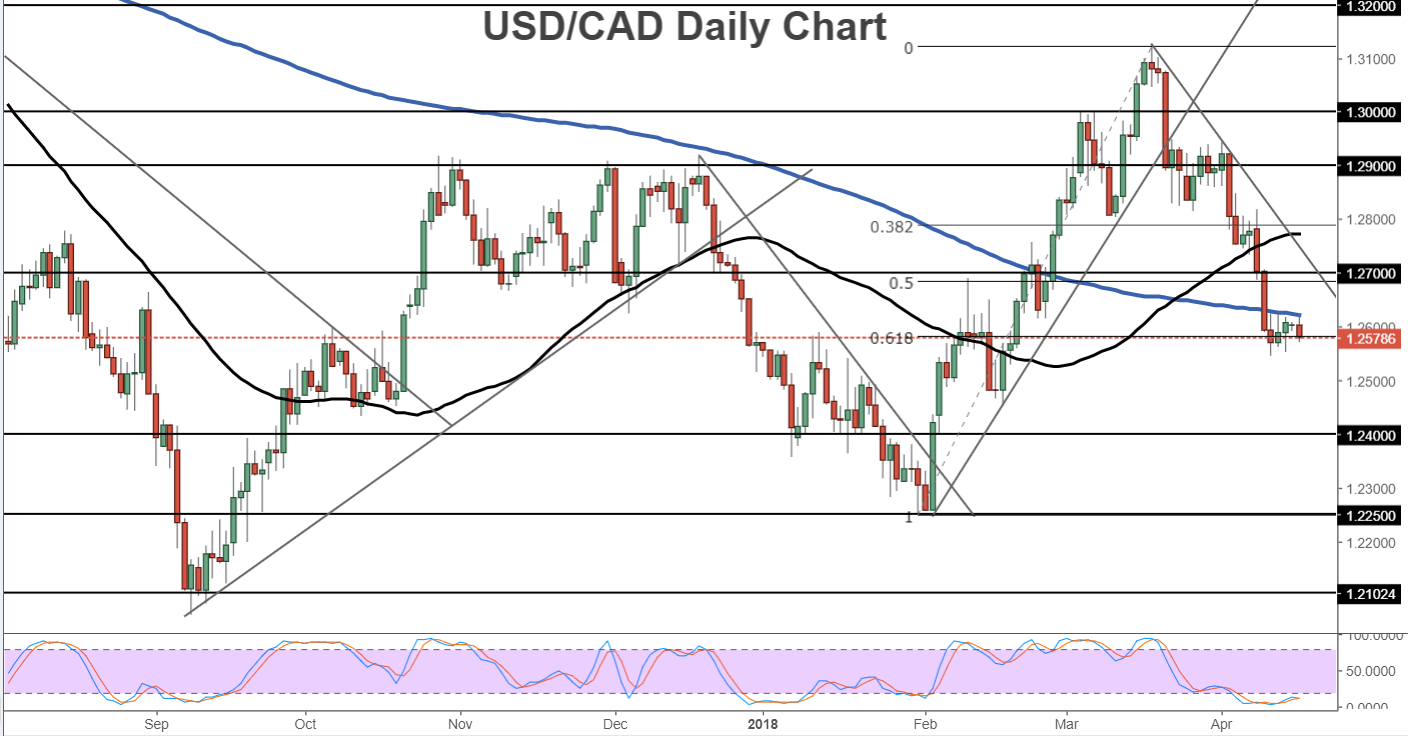

Monday’s resumption of persistent pressure on the US dollar helped to further weigh down the USD/CAD currency pair, which has been entrenched in a clear and precipitous downtrend for nearly a month. Though Monday’s USD/CAD fall did not yet establish a new low as of this writing, key market triggers this week, especially pertaining to the Canadian dollar, have the potential to further extend the USD/CAD slide.

First up will be Wednesday’s Bank of Canada interest rate and policy decision. With the BoC on a rather clear tightening track towards higher interest rates, much like the Fed, the rate decision and rhetoric surrounding it could have a strong impact on the Canadian dollar. At this time, the market consensus expects the central bank to keep its overnight rate steady at 1.25%, but any hawkish-leaning elements of its statement or within its subsequent press conference could make a significantly positive impact on the Canadian dollar, especially since recent economic indicators have generally been positive. However, if additional concerns about ongoing NAFTA talks and US trade policies are stressed more than might be expected, the Canadian dollar could instead be pressured.

Also of significant importance for the Canadian dollar will be Friday’s month-over-month Canadian CPI inflation data for March. The previous two months showed substantially higher-than-expected consumer inflation in Canada. Another higher reading could provide yet another boost for the Canadian dollar. Canadian retail sales data for February will also be released on Friday.

From a technical perspective, USD/CAD has been entrenched in an extended slide from late March. The current tumble from March’s 1.3123 peak formed a bearish head-and-shoulders pattern which was broken down in early April. Since that breakdown, the currency pair has further broken down below both its 50-day and 200-day moving averages. Within the past week, the currency pair has settled in a consolidation around the 62% Fibonacci retracement of the late-January low to the late-March high, forming a potential bear flag pattern in the process. With any major breakdown and further extension significantly below this level (around 1.2580), further pressure on the US dollar and support for the Canadian dollar could push USD/CAD towards its next major downside target around the 1.2400 support area.

Author

James Chen, CMT

Investopedia

James Chen, Chartered Market Technician (CMT), has been a financial market trader and analyst for nearly two decades.