US versus the Eurozone: Inflation divergence causes monetary desynchronization

Historically there is a very close correlation between changes in US Treasury yields and German Bund yields. This is relevant at the current juncture, considering that the recent hawkish twist in the tone of the Federal Reserve might continue to push US long-term interest rates higher and put upward pressure on bond yields in the Eurozone. However, since the start of the year, the increase in Bund yields is lower than expected based on the past statistical relationship. This probably reflects a conviction by investors that the ECB will start cutting its policy rate earlier than the Federal Reserve. This monetary desynchronisation is linked to a notable difference in terms of inflation with the US. Therefore, when the ECB signals that it will cut policy rates in the near term, markets are not surprised. What’s more, the message from the ECB is credible because it is underpinned by the view that monetary policy thus far has been successful in bringing and keeping inflation on a path towards its target. Successful disinflation thus cushions the impact of higher US Treasury yields on long-term interest rates in the Eurozone.

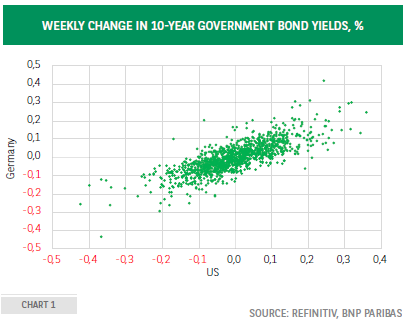

The evolution of long-term government bond yields tends to be highly correlated internationally. This may reflect the synchronization of real growth, inflation and monetary policy, the role of fluctuations in risk appetite -which are also very correlated globally- as well as international capital flows by investors seeking attractive opportunities in terms of yield.

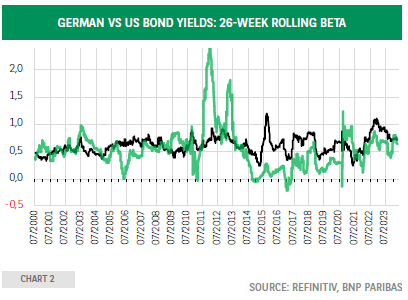

Chart 1 illustrates this phenomenon for US and German 10-year yields. Clearly, the relationship between weekly changes in both markets is very close -the changes having the same sign in about 80% of observations1- but, as shown in chart 2, it fluctuates over time. Historically, the beta from the regression of the weekly change in German yields as a function of the weekly change in US yields has fluctuated more for 2-year yields than for 10-year yields.

This may reflect a bigger influence on the former of the near-term outlook for monetary policy. Sometimes this is highly synchronised -which is associated with a high beta- and sometimes it isn’t, in which case the beta will be low. Since 2014, the beta for longterm bond yields has been higher than for short-term yields most of the time. To a large extent this is related to a stable and very accommodative monetary policy, with rates being at the zero lower bound in the US and even in negative territory in the Eurozone for a considerable number of years. This weighs on the beta for 2-year bonds, whereas for 10-year bonds, fluctuations in the term premium play a bigger role.

The high correlation between changes in long-term yields in the US and Germany is particularly important at the current juncture, considering the change in tone from the Federal Reserve. Until recently, the message was that the Fed would soon become sufficiently confident that inflation would move sustainably to 2%.2

However, against a background of ongoing growth resilience and stubborn inflation, this message has now changed, with Fed Chairman Jerome Powell noting that “it will likely take more time for officials to gain the necessary confidence that price growth is headed toward the Fed’s 2% goal before lower borrowing costs.”3 This vindicates developments in the US Treasury market, which has seen an increase in 10-year yields since the start of the year of 75 basis points.

Should the likelihood increase that the Federal Reserve refrains from cutting rates this year, Treasury yields would probably continue to rise, which, given the bond market correlation discussed above, could put upward pressure on yields in the Eurozone.

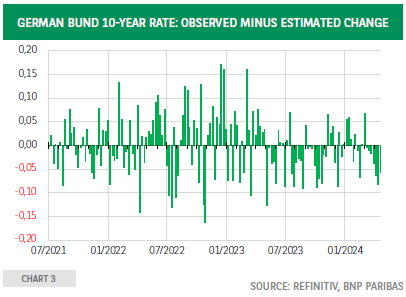

Such a development would be most unwelcome because it might delay the economic recovery there. This concern is warranted. After all, in Germany, the 10-year Bund yield has increased 46 bp since the start of the year, much less so than in the US. This reflects, for a part, a repricing of the monetary policy outlook with rate cuts starting later -June rather than April- and being more gradual. The increase in US yields has certainly also played a role, in line with the historical relationship. How does the rise in German yields compare to expectations based on the statistical relationship between both bond markets and given the change in US yields?

Chart 3 shows the difference between the observed change in Bund yields and the estimated change. In recent weeks, this difference -which corresponds to the regression residual- has become increasingly negative, implying that the rise in German yields has been smaller than expected. This probably reflects a conviction by investors that the ECB will start cutting its policy rate earlier than the Federal Reserve4. This monetary desynchronisation is linked to a notable difference in terms of inflation, which continues to decline in the Eurozone whereas this movement has stopped, at least for the time being, in the US.

Therefore, when the ECB signals5 that it will cut policy rates in the near term, markets are not surprised. What’s more, they consider such a move is warranted: the message from the ECB is credible because it is underpinned by the view that monetary policy thus far has been successful in bringing and keeping inflation on a path towards its target. Successful disinflation thus cushions the impact of higher US Treasury yields on long-term interest rates in the Eurozone.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.