US Second Quarter GDP Preview: The dollar follows growth

- Economic growth expected to decline in second quarter

- First quarter was boosted by business inventories and a narrower trade deficit

- Consumer spending to remain strong

The Bureau of Economic Analysis a division of the Commerce Department will issue its first estimate for annualized gross domestic product for the first quarter at 8:30 EDT, 12:30 GMT on Friday July 26th. This is the first of three estimates.

The Commerce Department will also issue revisions to GDP figures for 2014 through the first quarter of 2019 based on new economic data.

Forecast

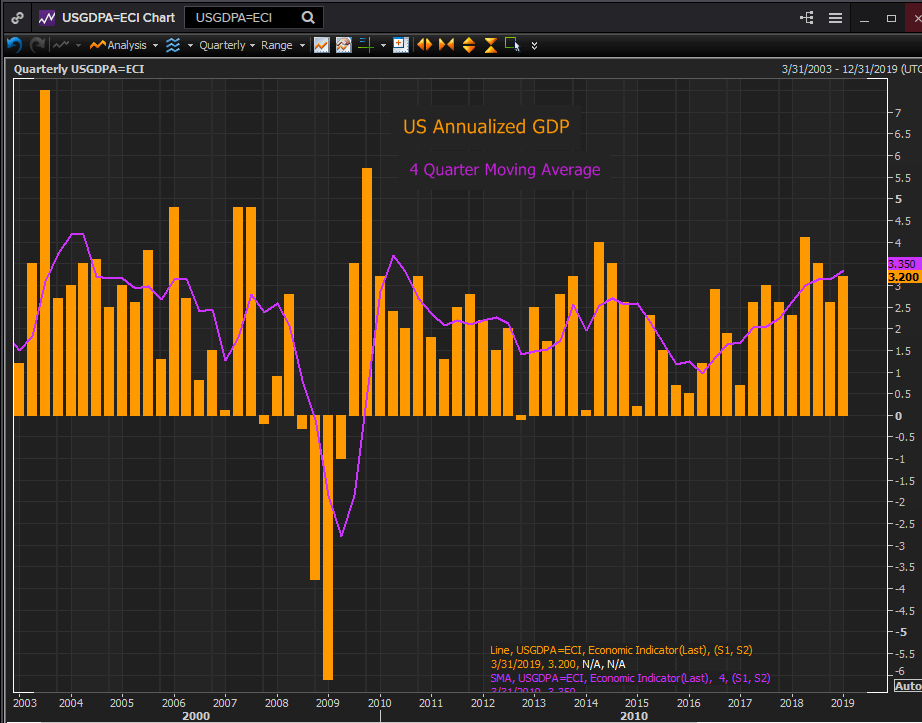

US annualized GDP is expected to decrease to 1.8% in the second quarter from 3.1% in the first three months of the year and 2.2% in the final quarter of 2018. The range of estimates in the Reuters Survey of economists is 1.1% to 2.9%.

Reuters

Consumer spending and sentiment

Household consumption is about 70% of US economic activity. Alone it is not enough to push the economy to higher rates of growth but without it rapid expansion is impossible.

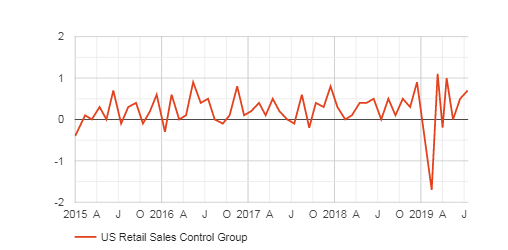

Retail sales had a good quarter. The so-called control group the Census category that informs the GDP calculation rose in all three months averaging 0.6% for the quarter. Personal consumption expenditures were positive in April and May at 0.2% each and the annual gain is expected to be 4.3% in the second quarter.

FXStreet

Job creation remains strong with 224,000 new positions in June and a 50 year record 3.7% unemployment rate. Wage gains at 3.1% in June are near the top of their range for the last decade. Initial jobless claims also at a five decade low are indicative of an economy at full employment.

Consumer sentiment reflects the labor market. The Conference Board consumer confidence index averaged 127.3 for quarter, down from the nearly two decade highs in the second half of last year but still among the best scores of the past 20 years. The Michigan Consumer Survey shows a similar robust placing for consumer attitudes.

Business spending and confidence

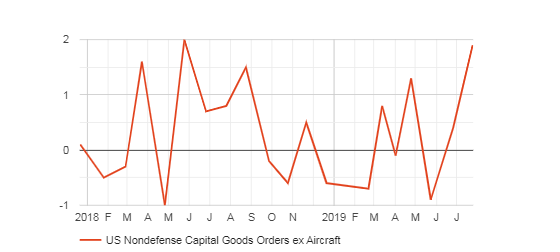

Business investment is one of the questions for the second quarter. The durable goods class of non-defense capital goods excluding aircraft and part, a general proxy for business spending averaged a 0.467% increase in the quarter that compares to the 0.667% average in the first three months of the year. In addition, the inventory build that helped to drive growth in the first quarter will restrain spending to the degree that the goods are unsold.

FXStreet

Business sentiment is at a low ebb of the past three years. The manufacturing purchasing managers survey registered 51.7 in June, the weakest it has been since the 2016 election. The index for new orders just skirted contraction in June at 50 and that is the poorest since December 2015.

Sentiment in the service sector fared better in absolute terms at 55.1 in June but that is still the lowest reading in two years. The new order index score of 55.8 is the lowest since December 2017 and more ominously it is well below all post-election figures except that one December number cited above.

Business sentiment has been riddled by the trade war with China which has been running for 18 months and shows no sign of settlement. The early optimism of last year has settled into grinding concerns about tariff induced price increases, supply chain disruptions, the potential cost of relocating manufacturing out of China and the overall drag on global growth.

Brexit has also returned to the news with the promise of Britain’s new Prime Minister Boris Johnson to honor the October 31st withdrawal date with or without a departure deal with the EU.

The effect of international trade on GDP is another point of potential damage. In the government's accounting of economic activity exports add to GDP and imports subtract from it. Boeing Company of Chicago, the nation's largest single exporter, took its largest ever charge against profits in the second quarter as its bestselling aircraft the 737 MAX remains grounded.

Conclusion

The American consumer economy is healthy but business sentiment has struck its lowest level of the past three years. Concerns over global growth, trade disputes and Brexit have cut into the willingness of business to spend for future consumption. Even the robust US economy is not enough to replace global consumption for many US firms that generate large amounts of sales in foreign markets.

The Atlanta Fed GDPNow model estimates 1.3% annualized growth in the second quarter, considerably lower than market forecasts. For the first quarter the final GDP Now prediction was 2.7%. The advance figure was 3.2%.

Despite the pending 0.25% Fed rate cut on the 31st the dolllar has been supported by good US economic figures that have helped reduce the chance of additional rate cuts after July. The ECB has played a part as well with Mario Draghi’s promise to cut rates and restart QE if the economic situation warrants keeping the euro on the defensive.

The dollar will likely trade in step with GDP. The better the second quarter number the better for the greenback.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.