US recession fears retreat as markets, jobs rally

Recession fears have receded in the US as job creation has proved resilient to the decline in business spending and the yield curve has returned to a normal spread after a brief inversion in late August.

Over the past two years the labor market has been the backbone of the US economic expansion. Plentiful jobs, rising wages and historically low unemployment rates have kept the consumer side of the economy humming.

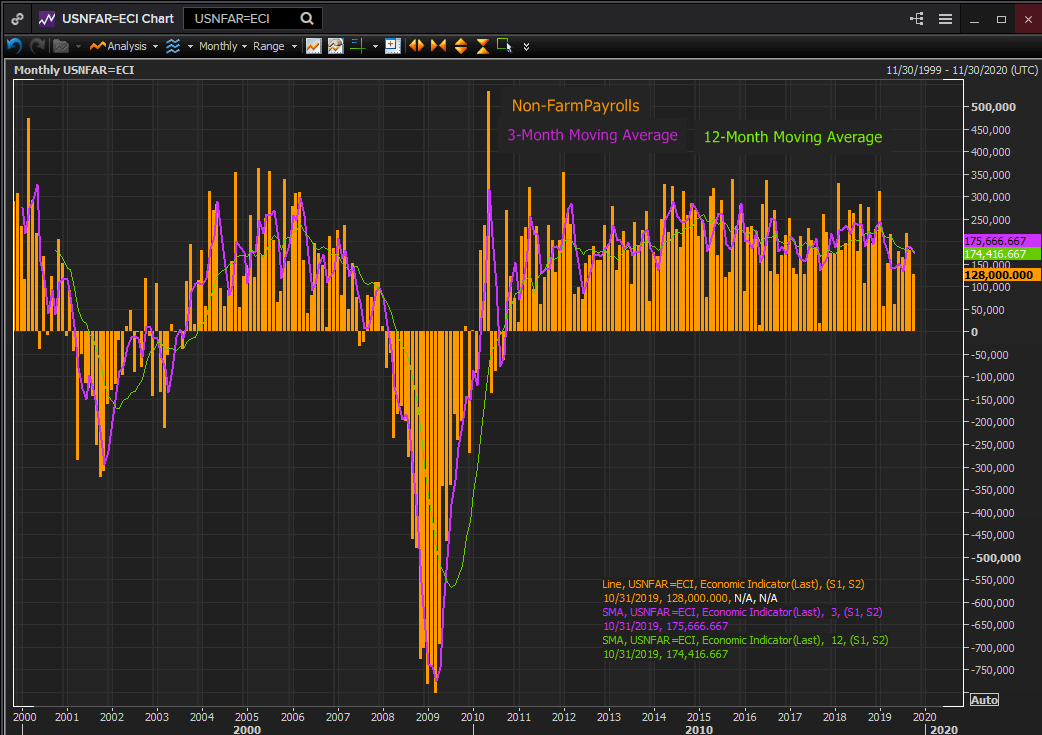

American firms have steadily produced more jobs than there were workers to fill them. Even though non-farm payrolls declined from a three-month average of 245,000 in January to 176,000 in October jobs remained well above the number of new entrants to the labor markets.

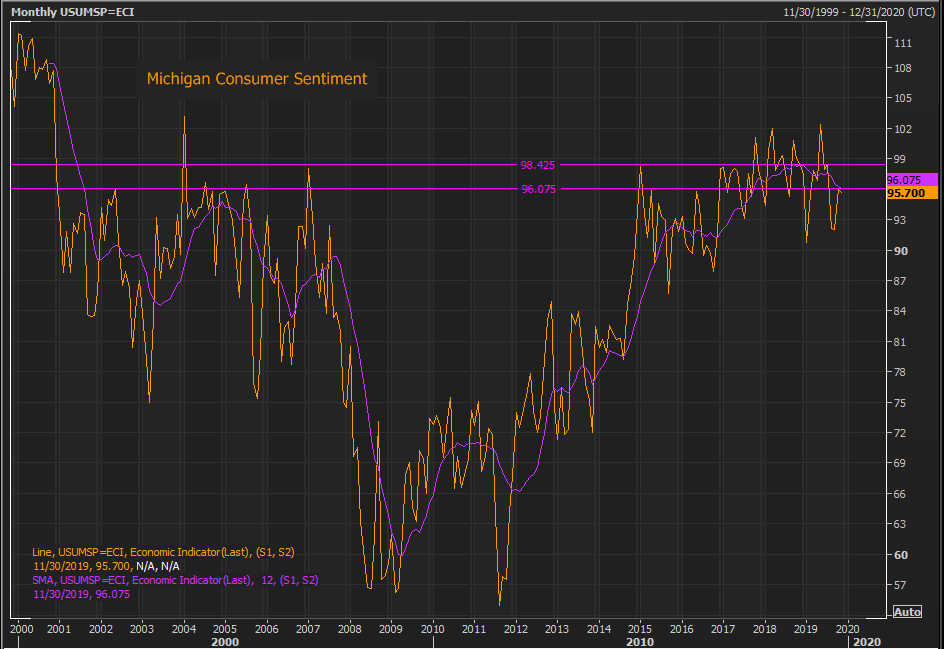

Consumer confidence has reflected the strength of employment. The average in the Michigan Consumer Sentiment Survey of the past two years has been the highest and most stable in over two decades.

Reuters

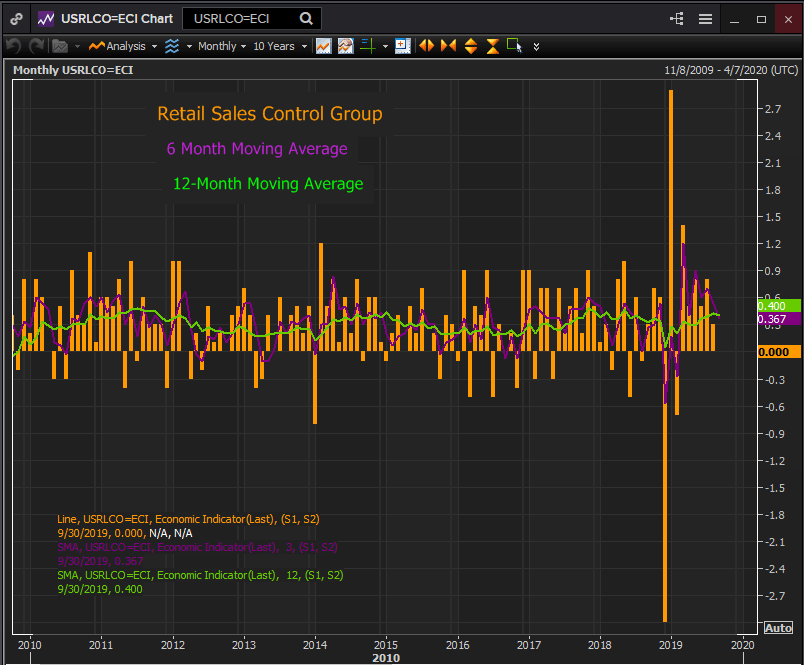

Retail sales kept pace with wages increases and the rise in disposable income. The control group component of GDP shows a steady if unspectacular record of gains for the last two years.

Reuters

Although the consumer economy continued to operate with vigor a combination of business, political and economic factors combined in late summer to produce the most serious recession scare since the financial crisis.

Business spending had been decreasing for most of the last two years. In July the 12-month moving average for the durable goods category of non-defense capital goods, an oft used proxy for business investment, turned negative for the first time in almost three years.

Reuters

That same month the 3-month moving average in payrolls fell to 135,000 its weakest in seven years.

Reuters

When the decrease in payrolls and the cessation of business spending were placed against the background of slowing domestic activity, GDP had fallen from 3.1% in the first quarter to 2.0% in the second and the global slippage in growth it seemed as if the longest post-war expansion might be reaching its limit.

If job growth continued to fall then the last support of US GDP, consumer spending, might disappear with employment. With business investment already moribund, the risk of recession could rise sharply.

Behind the eclipse in business spending was the enervating US China trade war. In mid-to late summer it seemed as intractable as ever with a new round of US tariffs set to take effect in the fall and no negotiations scheduled. In Europe the Brexit puzzle remained unsolved and an October 31st no-deal exit a live option.

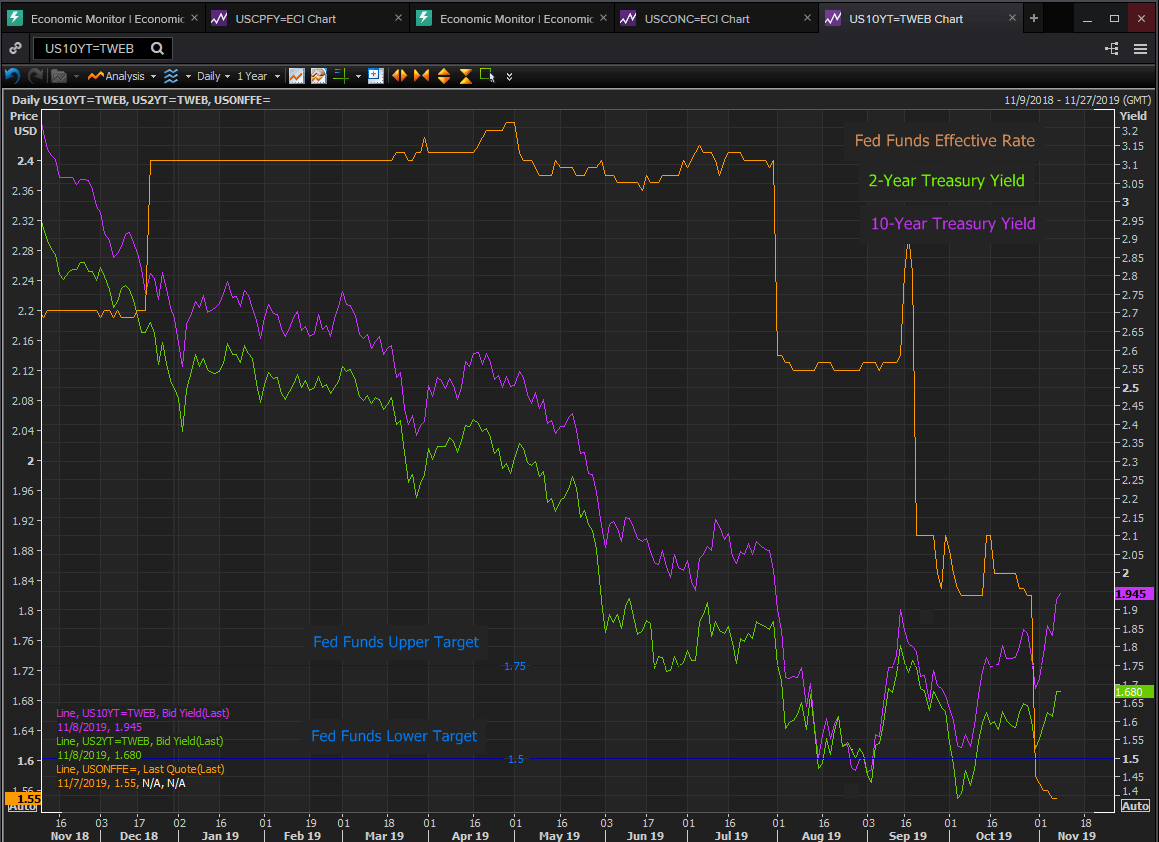

Mirroring the concerns for the US economy was the collapse and for a few days in late August, the inversion, of the 2-10 Treasury spread. Long considered one of the most reliable recession indicators it touched a peak reversal of 5 basis points on August 28th.

Reuters

Answering these concerns the Federal Reserve cut its base rate by 0.25% for the first time in a decade on July 31st and then again on September 18th and indicated that more reductions lay ahead.

But just weeks later, by mid-October the economic and political directions had changed remarkably.

Payrolls did not falter. August’s figures released on September 6th and then revised ended at 219,000, September’s were 180,000. Unemployment dropped to 3.5% in October and third quarter GDP proved to be stable at 1.9%.

Most importantly on October 11th President Trump announced a deal in principle with China for what he called a phase one agreement on trade, thus removing the threat of an ever escalating trade and tariff war.

Credit spreads responded immediately. Within three weeks, by the close on November 8th, the 2-10 Treasury spread was out to 27 points, normal for the conditions of the past two years.

By the first week of November all three major US equity averages had reached new records.

The US China trade deal, which will not be signed until sometime in December, is not a guarantor for US, Chinese and global growth. It is, however, an effective recession preventative.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.