US Non-Farm Payrolls June Preview: The delicate art of prediction

- Payrolls expected to increase by 3 million jobs.

- ADP June private payrolls rose 2.369 million, May revision adds 5.825 million.

- Manufacturing PMI unexpectedly jumps into expansion at 52.6.

- New orders in manufacturing soars to 56.4 from 31.8 with the largest gain on record.

- US dollar has retreated from its two-week rally.

Perhaps a bit of sympathy is due, the economists trying to predict the course of the labor market over the past three months.

The novelty and excess of the employment collapse took econometric models far beyond historical precedent, leaving their operators with little but guesswork and assumption. It took a month for analysts to bring their forecasts for initial jobless claims in line with reality.

By the April Non-Farm Payrolls report on May 8 it seemed forecasters had grasped the situation. The consensus estimate was 22 million and the actual was 20.5 million.

But then in May, it was off to the estimated races again. The consensus forecast for NFP was for a loss of 8 million jobs. In fact, US employers hired 2.5 million workers, an astonishing miscalculation of 10.5 million.

The close cousin of NFP, the private payrolls of Automatic Data Processing had similar results. April’s predicted loss of 20.05 million forecast was near the -19.557 million result. However, the May prediction of -9 million missed the initial -2.76 million figure by 6.24 million, not quite as bad as NFP but a record for the series.

But one month later the revision to May added 5.825 million jobs, giving the month a gain of 3.065 million not a loss of over 2 million and a world record payroll prediction miss of 12.065 million.

Since ADP tracks actual payrolls and includes no estimates for created jobs like the Bureau of Labor Statistics (BLS) ‘birth-death model’, how ADP managed such an astronomical miss is an open question.

Is recovery even more bedeviling than catastrophe?

The answer is probably no.

Analysts had more than a month to integrate the weekly unemployment claims numbers into their models for April’s NFP and ADP estimates which clearly aided the accuracy of their forecasts.

When the economy switched to hiring in May the models were again directionless. The linear projection for NFP and ADP for May, -8 million and -9 million respectively could not account for the abrupt change from firing to hiring. The initial claims numbers in May had continued to mount, averaging 2.3 million new claims each week so the analysts can be forgiven for imputing more payroll losses. Nor could the models factor in the overwhelming desire of employers to reopen business and employees to return to work as soon as permitted.

The June ADP estimate returned to reasonable accuracy predicting 3 million in the Reuters survey and 2.5 million in the Dow Jones survey for a 2.369 million number.

ADP payrolls

Non-Farm Payrolls

National payrolls are forecast to rise 3 million in June after May’s 2.509 million gain and April’s 20.687 loss. The spread in the predictions from 405,000 to 9,000,000, is unusually wide.

The unemployment rate is expected to drop to 12.3% from 13.3% in May and 14.7% in April. Annual average hourly earnings should fall to 5.3% from 6.7% in May and 8% in April as lower-paid workers return to their jobs. On the monthly wages, expectations are that it will drop 0.7% after the 1% decline in May. Average weekly hours will slip to 34.5 in June from 34.7.

Consumption in May

Retail sales, durable goods and personal spending confirmed the April bottom and subsequent reversal. Retail sales dropped 14.7% in April, by far the largest one month decline on record and then roared back 17.7% in May, more than double its 8% estimate.

Retail sales

Durable goods, a subset of sales fell 18.1% in April and rebounded 15.8% in May, beating the 10.9% prediction. Non-defense capital goods, the business investment proxy, dropped 6.5% in April then rose 2.5% in May, much more than the 1% projection. Personal spending climbed 8.2% in May following the 12.6% April tumble and was the only consumption gauge to miss its forecast at 9%.

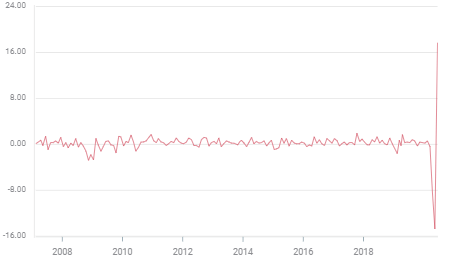

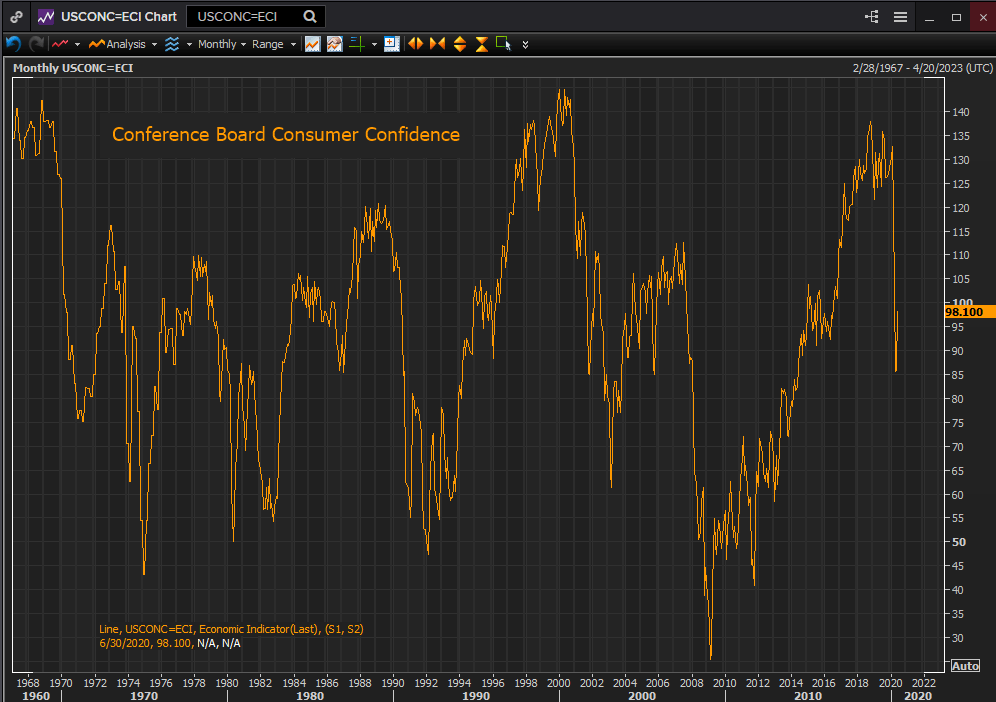

Consumer confidence

The Michigan survey of consumer sentiment has rebounded from its April low into June. The two-month drop from February to April in each of the three indexes, – sentiment, current conditions and expectations – was the steepest in the 68-year series.

The current conditions index has recovered the most, April 74.3-June 87.1, followed by overall sentiment, April 71.8-June 78.1, and then expectations, April 70.1-June 72.3.

Conference Board figures have a sharper recovery. The consumer confidence index jumped to 98.1 in June from 85.9 in May, well ahead of the 91.6 forecast. The present situation index climbed to 86.2 from 68.4 and the expectations index rose to 106.0 from 97.6.

Purchasing managers’ indexes

The June purchasing managers indexes (PMI) from the Institute for Supply Management were also better than expected. The overall index rose into expansion at 52.6 from 43.1 in May beating the 49.5 forecast. New Orders soared to 56.4 from 31.8 in May and, more than doubling the April low of 27.1. It was the largest one month and two month gain in the 72-year history of the series.

Employment lagged the improvement rising to 42.1 from 32.1 in May and missing the 43 forecast.

Conclusion and markets

Businesses have taken heart from the strong retail recovery in May, which, along with the rising June consumer sentiment figures produced the surprise jump into expansion of the June manufacturing PMI figures. Services PMI which will be released on Monday July 6 is forecast to rise to 48.9 in June from 45.4 but that should be now considered a low estimate in the 44.9 to 53.3 range.

The China trade deal remains intact and in the best interests of both nations despite the US displeasure over the Hong Kong security law.

The unexpected May addition to NFP payrolls, the revision to the ADP number bringing it into line with the national figures, and the June 2.4 million gain in private payrolls places the risk for June non-farm payrolls firmly on the positive side.

While no states have ordered widespread business closures or sheltering instructions, Texas Governor Abbot shuttered bars on Monday a month after permitting them to open saying that they were one of the sources of the increase in new cases. California has issued a list of businesses to close and 12 states have paused or rolled back parts of their opening schedules.

While Americans appear disposed to return to their normal spending habits abetted by clearing purchases deferred by two months of closed stores, the wildcard is the progress of the second wave of the pandemic. If it again forces widespread closures the economy will close all of its improvement of the last two months.

Equities just closed their best quarter in decades anticipating the recovery and reversing the panic decline of March. The Dow rose 17.8% it best since 1987, the S&P 500 gained nearly 20%, its best since 1998 and the Nasdaq jumped 30.6%, its strongest since 1999.

The rise in US virus cases had brought on a mild degree of risk-aversion in currencies which has dissipated. It is unclear how much the new closures will impact the economy or where the pandemic is headed. On those two questions, more than on economic statistics will turn the immediate direction of the stocks and the dollar.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.