US Initial Jobless Claims Preview: California returns to work

- Claims forecast to dip to 875,000 from 900,000.

- Continuing claims expected to be unchanged at 5.054 million.

- Payrolls predicted to rebound to 85,000 in January.

- California to reopen economy despite unchanged pandemic caseload.

- Dollar waits for improved American economy and statistics.

Unemployment filings are expected to continue at nearly a million per week even as California lifts its lockdown that has helped drive job losses.

New Initial Claims are forecast to drop to 875,000 in the January 22 week from 900,000 previous. Continuing Claims are projected to be unchanged at 5.054 million.

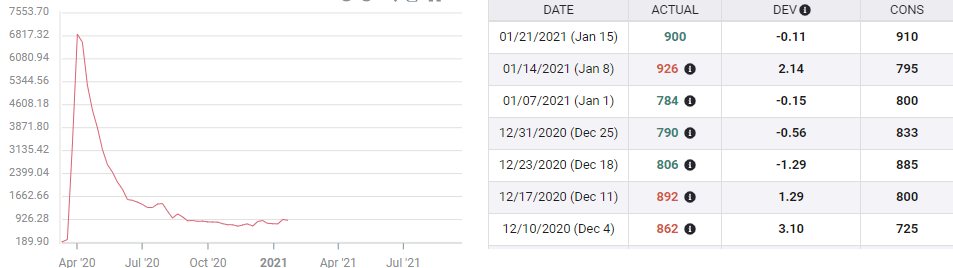

Initial Jobless Claims

Requests for jobless benefits had reached their pandemic low in November with the final four-week moving average at 740,500. In the following six weeks the average has climbed 107,500, 14.5% to 848,000 (January 15), and if the current forecast is correct the average will rise to 871,250 in the January 22 week.

Initial Claims, 4-week moving average

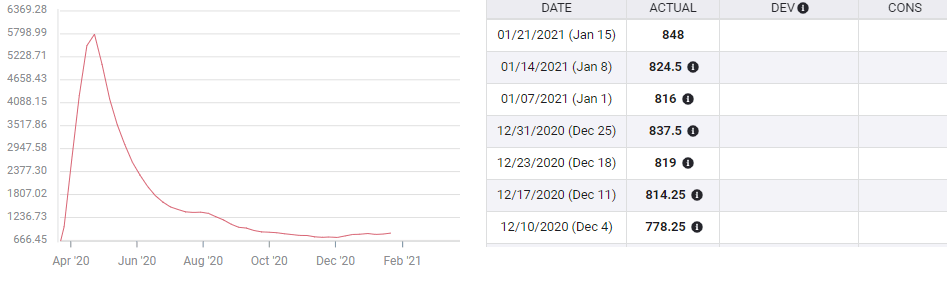

Continuing Claims have fallen to the lowest level of the pandemic as more recipients lose their benefits or return to work than are filing for new assistance.

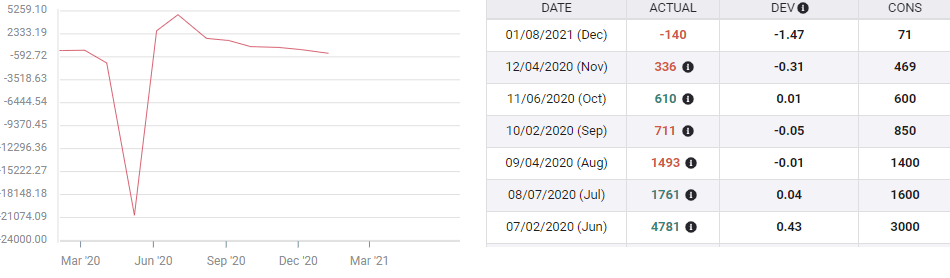

Initial Claims and Nonfarm Payrolls

Payrolls have mirrored the surge in claims, falling as filings rise, but the correlation is not specific month to month.

Nonfarm Payrolls were 610,000 in October and the four-week moving average for claims was 788,500. Payrolls dipped to 336,000 in November even though the claims average continued lower to 740,500. Here, the two middle weeks of the month averaging 767,500 were more predictive than the first and last weeks which averaged 713,500.

In December payrolls surprised by shedding 140,000 jobs, much worse than the forecast gain of 71,000 and the four-week claims average jumped 13% to 837,500.

Claims have remained at a much higher level in January with the four-week average at 848,000 on January 15 and, as above to 871,250 in the coming week. Nonetheless, the payrolls forecast for January, due February 5, is 85,000, better than the December prediction notwithstanding the claims average being considerably higher.

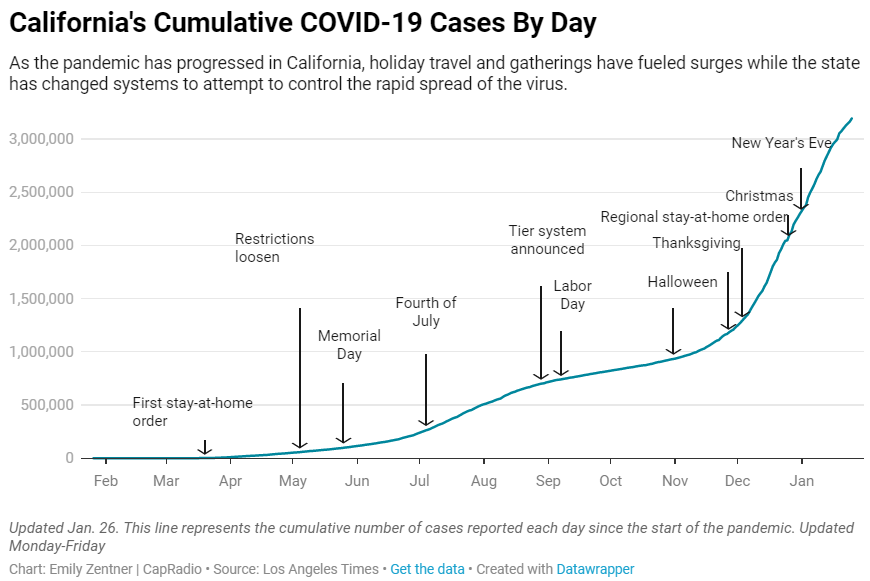

California lockdown

Despite no significant improvement in the hospitalization or ICU usage rates, Governor Gavin Newsom on Monday rescinded stay-at-home orders across the state, allowing restaurants to reopen outdoor dining and removing restrictions on travel.

The original criteria imposed in December specified that in order to reopen a region must have 15% availability in its ICU capacity. At least two of the state's five regions were below that threshold on Monday.

California had been under the strictest lockdown in the US since December which had does little or nothing to halt the spread the of the virus. The government's efforts to administer the vaccine have met with a supply shortage that has delayed roll out plans.

Governor Newsom is being challenged by a recall petition that had gathered about 75% of the necessary signatures to qualify for the ballot. In 2004 California voters successfully removed Democrat Gray Davis and replaced him with Republican Arnold Schwarzenegger.

Because California's economy is the largest in the US, 14.5% of total GDP, it has an out-sized effect on national numbers. If California returns to work the noatinal number will reflect the improvement.

Conclusion

The dollar's New Year recovery has been modest and based on three factors.

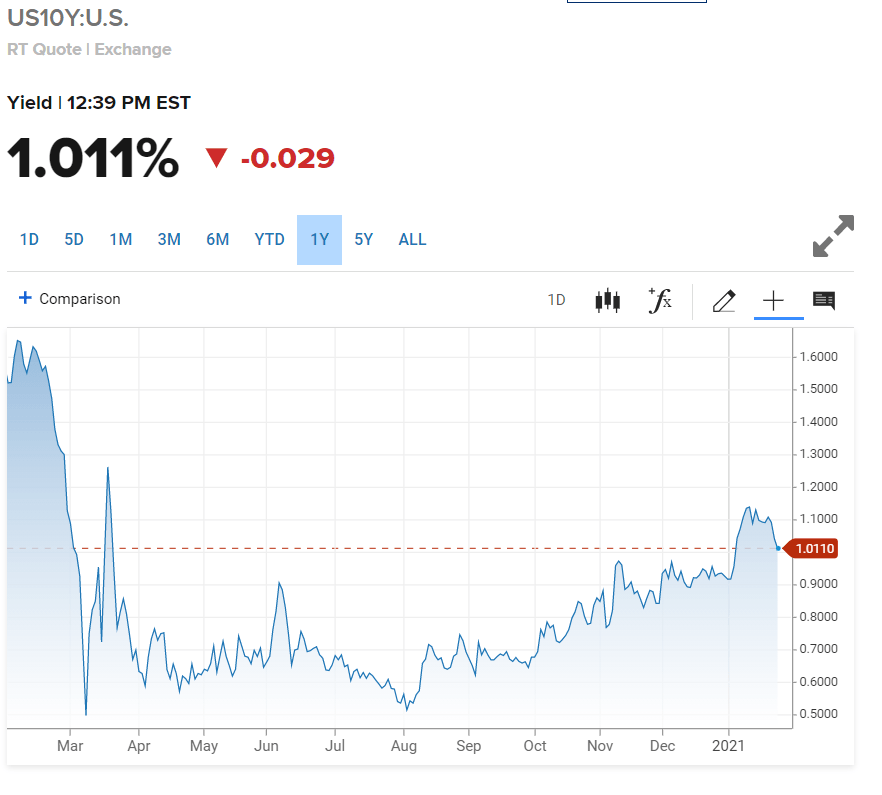

First Treasury rates have have increased. The 10-year bond has gained the 1% level for the first time since March. It is not the size of the increase, just 10 basis points from late December, but that for the first time credit markets are beginning to price an economic rebound in the quarters ahead.

CNBC

Second, the Biden administration is expected to complete a $1.9 trillion stimulus package in the weeks ahead, providing an extra $1400 in individual and family stipends.

Third, the COVID-19 vaccine roll-out is still projected to permit the return of normal economic life sometime in the second or third quarters.

These assumption have not been changed by the rise in unemployment claims and the loss of payroll jobs in December. Markets will remain keyed on the recovery until it is confirmed or not by the data.

When and if these expectations are reflected in the data, the dollar will rise.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.

![Hyperliquid representatives, Trade[XYZ] meet SEC Crypto Task Force to discuss digital asset regulation](https://editorial.fxsstatic.com/images/i/Hyperliquid_Bull.png)