US Consumer Sentiment Preview: Expectations look rich, dollar could receive a (second) blow

- Economists expect a marginal decline in US consumer confidence in January.

- Covid's ongoing rage, the slow vaccine rollout, and stimulus hiccups could result in a disappointment.

- The data is due just 90 minutes after retail sales statistics for December could paint a gloomy picture.

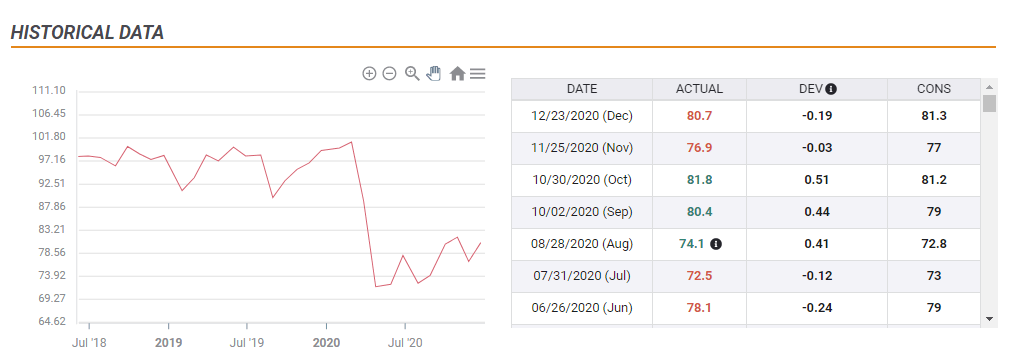

If the approval of vaccines cannot cheer consumers, what can? After the University of Michigan's Consumer Sentiment Index for December was revised down to 80.7, it is hard to see a recovery – and even a minor retreat seems too optimistic.

The economic calendar is pointing to a small retreat to 80 points, but economists missed the mark in the past two publications and may be overestimating the figure once again.

Source: FXStreet

Why consumers could be even more depressed

There are three additional factors to consider ahead of the release on January 15:

1) Dire covid situation: Since the latest update to UoM's measure, coronavirus has been spreading rapidly across the US. Hospitalizations have topped the 130,000 milestone, a daily death toll above 4,000 is not uncommon, and cases also continue their ascent. In this environment, it is hard to see improvement.

2) Slow vaccine rollout: As mentioned earlier, medical staff have been administering immunization since mid-December – but the pace remains sluggish. If optimism about the launch of the campaign failed to cheer consumers, the frustrating pace could push it lower.

3) Issues with the stimulus package: Outgoing President Donald Trump delayed signing the $900 billion relief package and postponed sending stimulus checks – which would have boosted sentiment. President-elect Joe Biden promised to raise it to $2,000, but that came only after Democrats won control of the Senate – probably too late for surveyors to incorporate into the preliminary report.

Potential dollar reaction

The greenback is highly sensitive to moves in US Treasury yields. The recent rise in returns has been driving the dollar higher. Will that change if economic figures continue deteriorating? The Federal Reserve has the keys to pushing yields lower by expanding its bond-buying scheme.

The Fed seemed reluctant to signal any change after Nonfarm Payrolls data showed a loss of jobs. That sent the dollar higher after only a short downside correction.

Consumer sentiment is released only 90 minutes after Retail Sales figures for December are due out. Without government support and with a raging virus, expenditure dropped in November – the months of Black Friday – and has likely continued declining in December.

Therefore, Friday's dual publications could deal two blows to the dollar, with consumer confidence having the final word.

In case UoM's data meet estimates or surprise with a bounce, the dollar could find some buying in the last hours of the week. However, chances are low.

Conclusion

The first read of consumer sentiment in 2021 may disappoint investors looking for an uptick, potentially resulting in a weaker dollar. The timing, just after retail sales data, may result in a higher impact than usual for these forward-looking figures.

More Five factors moving the US dollar in 2021 and not necessarily to the downside

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.