US Consumer Price Index March Preview: Explosive but expected, can it be dangerous?

- March CPI is expected to jump to 2.5% from 1.7% in February and 1.4% in January.

- Fed has said price gains will be temporary and a reversal of last year’s base effect.

- In 2020 annual inflation plunged from 2.5% in January to 0.1% in May.

- Fed has limited the policy impact of price changes with inflation averaging.

- Markets will not react to the jump in CPI if as forecast.

Inflation’s long overdue bill for the pandemic lockdown is at hand.

From January to May last year, with stores closed and most of the US shuttered under mandatory stay at home orders, retail sales collapsed dragging annual consumer price gains from 2.5% in January to 0.1% five months later.

A year later the US economy is verging on explosive growth and the revival of consumption has returned demand and price levels to normal.

Inflation reporting, however, for the next six months or so, will be anything but normal.

The March Consumer Price Index (CPI) is expected to rise 0.5% after increasing 0.4% in February. Core CPI is forecast to add 0.2% following a 0.1% gain in February. There is nothing unusual in those numbers.

The core annual rate should climb to 1.6% in March from 1.3%, high for a single month but not shocking. It is the headline rate that promises to be exceptional. Overall CPI is projected to rocket to 2.5% in March from 1.7% in February, a gain of almost 50% in a single month, from January’s 1.4% it is almost 80% higher.

The explanation lies in the comparative nature of annual inflation.

Base effect of Consumer Price Index

Consumer prices are measured from a standard set of items that is tracked from month to month and compared as an index to a base year.

In normal economic circumstances the monthly changes are relatively uniform and the annual trend is gradual.

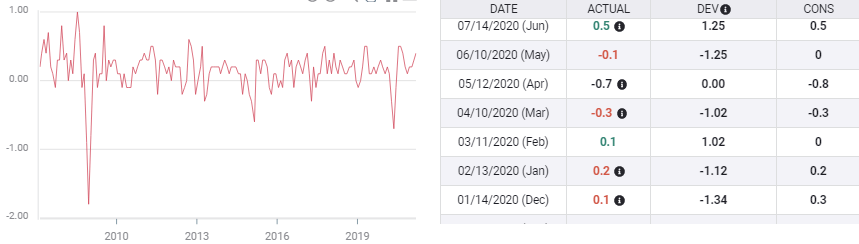

Last year the monthly variation went from 0.2% in January and 0.1% in February to -0.3% in March an astonishing -0.7% in April.

CPI

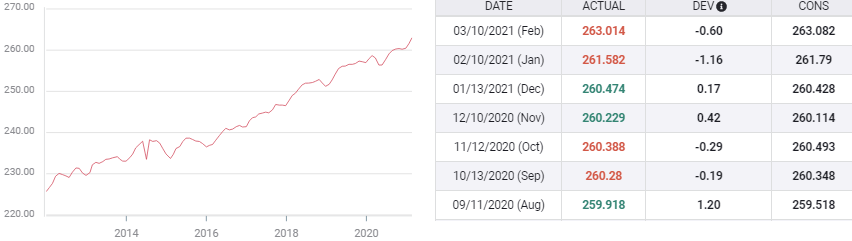

The index itself in 2020 went from 258.678 in February to 258.115 in March and 256.389 in April, the bottom of the pandemic lockdown.

Consumer Price Index (n.s.a.)

By February of this year the index had recovered to 263.014. The percentage comparison of those two February index reading gives the annual CPI measure, 1.7%.

Even if the March index this year were unchanged from February, the annual CPI would rise to 1.9% because the March 2020 index dropped as above.

If the April index was again unchanged the CPI would rise to 2.6% because the index for April 2020 fell again.

As it is, the index will rise in March by an expected 0.5%, the base will be higher and so the estimated CPI rate of 2.5% rather than 1.9% if the base had been stable. April will have an even higher annual rate because last year’s equivalent index was the lowest of the price reaction.

This unusual drop in the index in March, April and May last year is the base effect that many analysts and the Federal Reserve have been citing as the source of the rapidly rising inflation rate.

Federal Reserve response

Federal Reserve Chair Jerome Powell has said repeatedly that he and the governors view the coming inflation spike as temporary, a product of the calculation process.

In this judgement they are undoubtably correct. Prices changes have resumed a normal curve and as soon as the rate comparison moves past the aberrant months of the lockdown, the 12-month difference will reflect a much smaller price gap.

The Fed’s new inflation averaging policy, adopted last September was a fortuitous change unconnected to the pandemic but perfectly suited to the current circumstances. It will permit the governors to ignore the coming increases in prices without the markets speculating on a policy response.

The transitory nature of the price elevation is the main reason the Fed has been willing to maintain its $120 billion a month in bond purchases, repressing short-term rates.

Last year’s base effect, now becoming evident in the inflation numbers, has had an exaggerated impact on the markets, because it is compounded by the vast amount of deficit spending pouring out of Washington.

Interest rates at the medium and longer end of the yield curve have not moved sharply higher this year, because of the pending spike in inflation in the next few months.

US 10-year Treasury yield

CNBC

Credit markets are concerned that the many trillions in pandemic relief combined with an accelerating economy could produce actual inflation, liquidity compounded by demand.

Conclusion

By itself the base effect on inflation does not produce a long term change in inflation and inflation expectations. It expires with the extraordinary circumstance that produced it.

Credit markets are wary that the kick to inflation given by last year’s statistical fluke could merge with higher demand and liquidity driven prices changes.

Equities and currencies are watching how much higher US rates will go if inflation is stronger than forecast.

There is as yet no sign that prices have undergone a substantial development, but the next five or six months are going to be a nervous time for the markets and the Fed.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.