US capital goods orders as expected, timing for Fed cuts remains uncertain, US GDP growth lower

Previous week's events (week 22.04 - 26.04.2024)

U.S. economy

U.S. manufactured capital goods demand increased moderately in March. The report suggests that weakness in manufacturing does not appear to be intensifying. March’s increase was in line with economists’ expectations. Core capital goods orders gained 0.6% year-on-year in March.

Business spending on equipment has struggled in the aftermath of 525 basis points worth of interest rate hikes from the Federal Reserve since March 2022 to tame inflation. Though the U.S. central bank is expected to start lowering rates this year, the timing of the first cut is uncertain.

U.S. economic growth (GDP change) slowed more than expected in the first quarter. GDP increased at a 1.6% annualised rate last quarter versus a forecast of GDP rising at a 2.4% rate. A slower pace should have a sticky inflation in the future some suggest.

Inflation

Australia

Consumer price inflation (CPI) slowed less than expected in the first quarter as service cost pressures stayed stubbornly high, a disappointing result for policymakers who were thinking of cuts this year. CPI rose 1% in the first quarter, above market forecasts of 0.8%. For March alone, the CPI rose 3.5% compared to the same month a year earlier, up from 3.4% in February.

The Reserve Bank of Australia (RBA) has left interest rates at 4.35% for three straight meetings as confidence had grown that inflation was on track to ease back to its target band of 2-3% in late 2025.

Interest rates

European Central Bank officials plan to cut interest rates multiple times this year, even with higher U.S. inflation delays and tensions in the Middle East keeping oil prices high. ECB President Christine Lagarde has strongly hinted that the euro zone’s central bank is still likely to begin reducing its deposit rate from a record-high 4% in June.

BoJ

The Bank of Japan (BOJ) kept interest rates steady on Friday and highlighted that inflation was on track to durably hit its target of 2% in coming years, signalling its readiness to hike borrowing costs later this year. BOJ Governor Kazuo Ueda said the central bank would raise interest rates if upcoming data back up its latest price forecasts.

BOJ maintained its short-term interest rate target at a range of 0-0.1% as expected.

The projections for "core core" inflation, which is closely watched by the BOJ as an indicator of the broader price trend, for 2024 and 2025 were unchanged from January.

Currency markets impact – Past releases (22 - 26.04.2024)

Server Time/Timezone EEST (UTC+02:00).

Currency markets impact

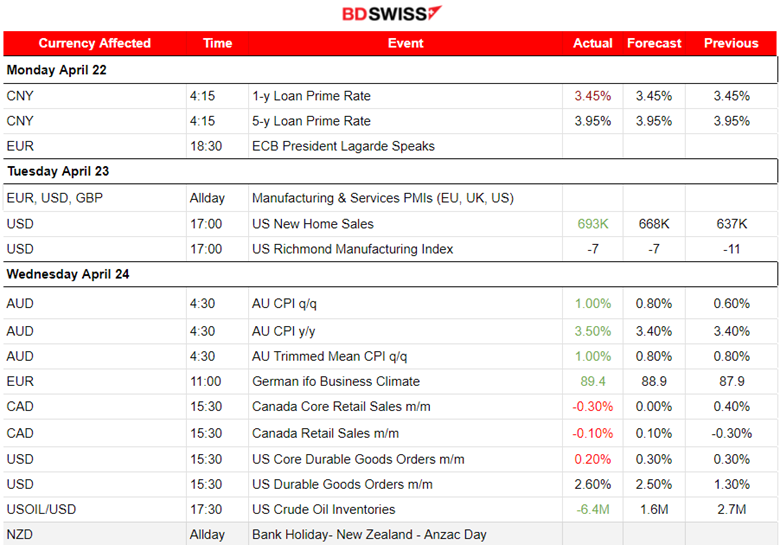

- On the 23rd of April, the Manufacturing and Services PMI figures were released:

Eurozone PMIs:

The French economy stabilised in April as renewed expansion in services activity offset the manufacturing sector contraction. The reported PMI in Manufacturing worsened to 44.9 but the services PMI turned to the expansion area with a reported PMI at 50.5 points. Private sector output levels remained unchanged from those seen in March. Services business activity increased for the first time since May 2023.

The German business sector returned to growth at the start of the second quarter driven by growth in services business activity. The manufacturing PMI remains in contraction while the services sector PMI reported a significant improvement to 53.3 points, turning in expansion. Although manufacturing remained in contraction, the rate of decline in factory production eased and confidence amongst goods producers towards the outlook reached the highest for a year.

The Eurozone PMI for services was reported improved. It shows that the economy is gearing up for an acceleration in activity after a year and a half of broad stagnation. It helps the EUR. However, that would be enough for a change in inflation expectations and a change in the ECB’s thinking about cuts? If we look at the U.S. the PMIs are not improving. This could be a signal of a downturn in U.S. growth and would suggest that the upcoming data will not be as great for the U.S. as before. Inflation obviously will be hard to bring down and the Fed will get even more puzzled on what to do in regards to future interest rate policy.

U.K. PMIs:

The U.K. experiences the fastest expansion of output since May 2023. The private sector activity expanded for the sixth consecutive month in April as a robust recovery in service sector output helped to offset a marginal decline in manufacturing production. Output growth from an upturn in new order volumes driven by the service economy. The services PMI reached, remarkably, to 54.9 points.

United States PMIs:

In the U.S. business activity expanded in April at the slowest pace this year on a pullback in demand that led to the first decline in employment since 2020. The services PMI was reported to worsen at 50.9 points. Orders showed contraction. The group’s measure of employment slid 3.2 points to 48.

-

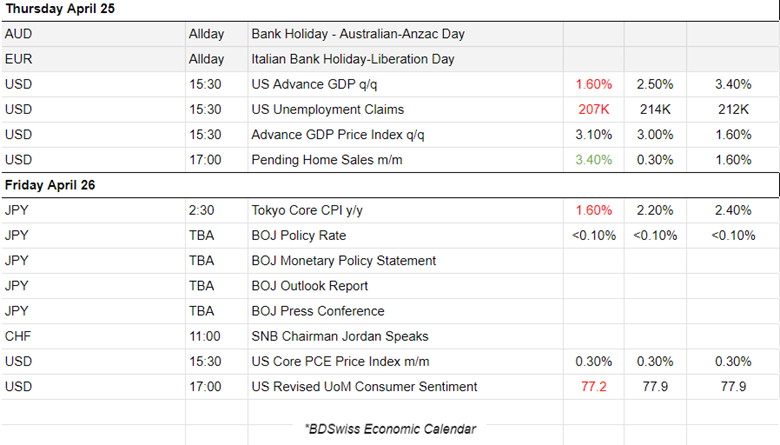

Australia’s inflation report on the 24th of April showed that the monthly CPI indicator rose 3.5% in the 12 months to March. The annual figure was reported higher at 3.5% from 3.4% which was steady for 3 readings in a row. The AUD appreciated at the time of the release. AUDUSD jumped near 30 pips before retracement took place back to the 30-period MA.

-

Canada retail sales figure releases showed that there are no signs of spending growth since the start of 2024. The latest figures show a decline in monthly core sales of -0.3% from the previously reported 0.4%. The retail sales figures showed a smaller decline of -0.1% versus the previous -0.3% decline. USDCAD jumped near 25 pips upon release due to CAD depreciation at that time.

-

The U.S. Durable goods figure released at 15:30 showed more growth, 2.6% versus the 2.5% expected. No major impact was recorded affecting the USD pairs.

-

At 15:30 the Advanced GDP figure (1st quarter 2024) for the U.S. was reported lower at 1.6% versus the expected 2.5%. The market reacted with sudden USD depreciation at first but it reversed soon to a strong appreciation and later another reversal confirmed the strong uncertainty that is governing the market currently.

-

Tokyo inflation slowed for the 2nd straight month according to the report released at 2:30. The actual figure was reported as 1.6% versus the expected 2.2%. The market did not react to the news as they were waiting for the BOJ news first. Core inflation fell below the central bank's 2% target, complicating its decision on how soon to raise interest rates.

-

Bank of Japan interest rate decision: Unchanged at 0%-0.10%. This follows the first rate hike since 2007, which was implemented in March. While the move was expected, this comes after Tokyo’s April inflation came in lower than expected. JPY depreciated heavily and the USDJPY jumped.

-

The U.S. Core PCE Price index figure was released steady at 0.3% reinforcing the Fed’s reluctance to cut interest rates anytime soon. At the time of the release, there was a sudden USD depreciation but the effect faded soon with the USD turning to steady and long intraday appreciation against other currencies.

Forex markets monitor

Dollar Index (US_DX)

The index is moving fairly sideways as the market eases activity due to the upcoming FOMC and Fed rate decision on Wednesday this week. The dollar is expected to be affected heavily, and probably to continue strengthening, if the Fed does not deny the fact that inflation is not going in the right direction. The Bank of Japan (BOJ) kept rates steady, keeping the interest rate differential between JPY and USD high and causing the pair to move to the upside aggressively. Today the pair dropped heavily, a sudden drop that hints at BOJ intervention, causing JPY to strengthen. The dollar was affected with depreciation against the other currencies during that time but the dollar index remains strong and over the support at near 105.5 points.

EUR/USD

This pair was experiencing an upward 30-period MA and the price was moving in an apparent channel formation. However, on the 26th of April, the price dropped and broke that channel to the downside. The price reached the support level near 1.06730 as the dollar appreciated heavily before reversing to the upside again. Recent developments and economic data releases suggest a delay in interest rate cuts from the Fed while the probability of an ECB cut instead soon grows. EURUSD is expected to drop if the fundamentals remain fixed. Further comments on the 1st of May during the FOMC and Fed Rate decision this week would cause high volatility and the pair to move in one direction. Comments for the delay in cuts would potentially cause high dollar appreciation and eventually downward movement for the EURUSD.

USD/JPY

The dollar has been relatively stable this week as seen above. However, the JPY experienced a remarkable weakness against other currencies. USDJPY started to move upwards from the 24th of April and gained momentum causing its rapid increase to the upside since the 26th of April. The Bank of Japan kept interest rates around zero on Friday the 26th of April. The lack of clear guidance on the future rate hike path triggered a broad-based decline in the yen. Traders were on high alert for signs of intervention by Japanese monetary authorities and that probably happened today on the 29th of April as the USDJPY dropped more than 50 pips after JPY's sudden and strong strengthening.

Crypto markets monitor

BTC/USD

Bitcoin halving took effect late on Friday 19th of April, cutting the issuance of new bitcoin in half. It happens roughly every four years, and in addition to helping to stave off inflation, it historically precedes a major run-up in the price of Bitcoin.

Currently, things are not looking good for the Crypto coin. A triangle formation has been breached today to the downside causing further Bitcoin price decline. 60K USD support so far away. However, considering its volatility, it is possible for the price to drop to that level, if other fundamental factors remain fixed.

This week's events (week 29.04 - 03.05.2024)

Coming up:

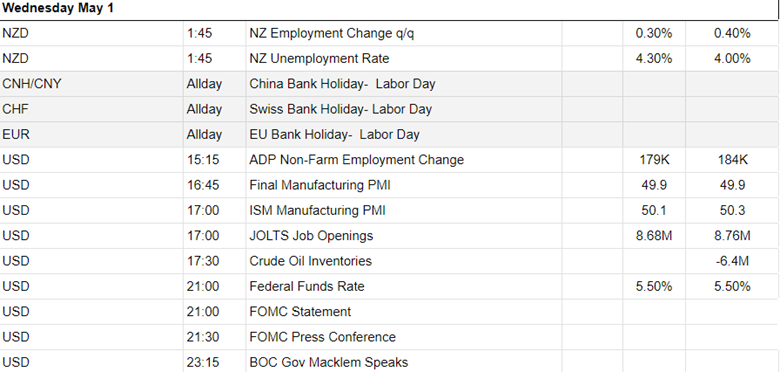

The latest figures confirm the pick-up in US inflation over the past few months. We have the FOMC statement and Fed Rate decision on the 1st of May that probably is going to shake the USD pairs and the markets in general.

Other important releases include the employment data for the U.S. on the same day, the 1st of May and the NFP report on Friday.

Currency markets impact

-

On the 30th of April, the Eurozone CPI flash estimate figures will be released giving important information that will determine if eventually the ECB will continue with the current narrative of potentially reducing borrowing costs soon. EUR is not expected to be affected greatly. The market will wait until the FOMC event takes place.

-

Canada’s monthly GDP figure release takes place at 15:30 and the CAD pairs are expected to be affected greatly. It is estimated that Canada’s GDP growth will be reported lower. That is likely the case, considering the decline in employment and retail sales decline for March. Unemployment has been rising as well.

-

CB Consumer Confidence at 17:00 will shed some light on what consumers are expecting for the near future now that inflation is showing an upward trend. Lately, it is declining as per the figures suggest. USD will probably be affected during that time as volatility levels could rise upon the release. Recent data suggest that U.S. consumers’ assessment of the present situation improved in March, but they became more pessimistic about the future.

-

Employment data for New Zealand will be released on May 1st at 1:45, and the NZD pairs could see an intraday shock upon release. Retarcement usually follows soon creating opportunities. We have negative expectations for the labour market. The RBNZ kept interest rates steady at 5.5% and that has not changed since April 2023. Cooling labour market data expectations are justifiable.

-

The U.S. ADP Non-Farm Employment Change figure (for April) will be released at 15:15 and the expectation is obviously a lower figure considering that the Fed has kept interest rates high. The JOLTS Job Openings report will be released at 17:00, another figure that will add to the labour market picture even though it is more of a lagging indicator since the Job openings reported is for the month before, March. It is also expected to be reported lower. This figure was actually declining since the start of the year and coincides with the recent GDP growth data for the U.S. that showed slower growth for the 1st quarter. The ISM Manufacturing PMI for the U.S. will be released at the same time and it is quite important for the Fed who want to see the progress of that sector. The services PMI showed that is currently strong and leading the economy. An improved figure could give a hint that interest rates are more likely to remain high. At 17:00 the USD pairs could see an intraday shock because of these data releases.

-

At 21:00 the FOMC statement and decision on the Fed rate will take place causing a shock in the markets. The USD pairs and related assets will probably be affected by an intraday shock. The Fed is expected to keep interest rates unchanged and proceed with updates on how the central bank will counter the recent inflation progress which is quite against their expectations.

-

On the 2nd of May, we have the release of the Swiss monthly inflation-related figure that is expected to be reported higher. The SNB was the first to proceed with cuts this year in March. CHF pairs could be affected greatly if we have surprises with this CPI figure since an expected rise in prices is logical after a cut.

-

Unemployment claims figure release for the U.S. takes place at 15:30 and the USD pairs could see more volatility during that time. A higher figure is expected but still remains near the usual average of 210K.

-

On the 3rd of May, the NFP report along with the Unemployment rate and Average Hourly Earnings figure will be reported at 15:30. The USD pairs and related assets will probably be affected by an intraday shock. Surprisingly employment is expected to be reported weaker but the unemployment rate figure is expected to remain steady and the same applies to the feared wage growth that could keep inflation high.

-

At 16:45 and at 17:00 the services PMI-related data will be released but not expected to have a great impact on the USD pairs.

Commodities markets monitor

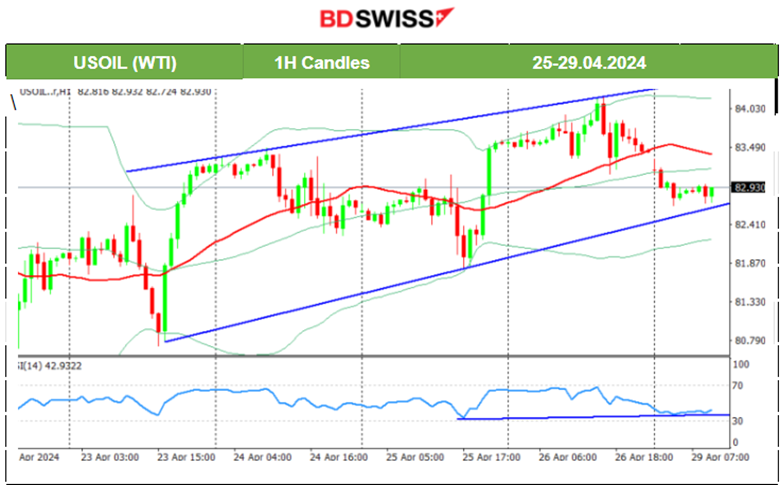

US Crude Oil

On the 25th of April, the resistance of 83.5 USD was broken and the price reached higher. On the 26th of April, this breakout even helped the price reach near 84 USD/b. Now an upward channel is apparent indicating the highly volatile market conditions that Crude oil is facing at the moment. The price is moving around the 30-period MA with deviations from the MA up to near 1 dollar. Will the price continue to move to the upside thus following the channel? A breakout below the channel could cause a rapid drop back to 82 USD/b.

Gold (XAU/USD)

On the 24th of April, the price remained stable. An apparent upward channel was formed with 15-20 dollar deviations from the 30-period MA taking place. The proposed range is 2,300-2,340 USD/oz. It would be unlikely to see a jump to 2,400 USD/oz. For that to take place we should see an unusual increase in demand for metals. The fact that the price currently is below the MA indicates a rather sideways path for now. Breakout of the channel to the downside might spark a dive in Gold’s price to 2,300 USD/oz. Alternatively, the next important resistance is near 2,350 USD/oz which matches the upper band of the 50-period BB indicator.

Equity markets monitor

S&P500 (SPX500)

Price Movement

On the 25th of April, the market experienced a sudden plunge causing the index to drop to the support near 4,990 USD before eventually reversing heavily to the upside. It crossed the 30-period MA on its way up and reached remarkably back to the 5,100 USD level. On the 26th of April, stocks moved higher but the rapid movement to the upside seems to slow down. The RSI is actually pointing at a potential bearish divergence. The downside breakout of the upward wedge/triangle formation is however not clear.

Author

BDSwiss Research Team

BDSwiss

BDSwiss is a leading financial institution, offering bespoke CFD trading and investment products to more than 1.7 million registered clients, in over 180 countries.