US big banks Q2 earnings preview: Robust but not amazing

Although they lag the triple-digit growing businesses in the S&P 500 universe, the shares of US Banks marked a jubilant performance on Wall Street during the second quarter, with some of the biggest institutions chasing fresh record highs. Perhaps the quarterly earnings for Q2 could be relatively less amazing when the results come out next week on Tuesday and Wednesday before the market close but even if that is the case, buying confidence is expected to remain intact in the US banking sector. The consensus recommendation from Refinitiv analysts is buy.

Investment banking, optimism support banks

Excluding Wells Fargo, it’s been a long time since the four largest US banks last presented the kind of heavenly results they announced in the first quarter. Net income soared to record levels, doubling and tripling in yearly terms, while earnings per share accelerated to all-time highs. Returns on tangible common equity, which measures profits relative to shareholders’ equity spiked to the highest since prior to the 2008 global financial crisis.

The booming numbers, however, did not emerge because of rising loan activities but because of the escalating retail trading, the increased deal-making in mergers and acquisitions for vehicles known as SPACS, as well the massive stimulus unleashed by the government. The successful vaccine distribution and the continuous improvement in economic indicators played a key role too, elevating growth projections for the US economy, and therefore, reducing expectations of debt losses within the banks.

Stress test passed

The latest stress test from the Fed came as a relief to validate the fabulous performance of the banking sector, showing that the nation’s 23 banks are fortified enough to survive another sudden catastrophic blow, which involves a 10.75% jump in the unemployment rate and a 55% freefall in stock prices. The results gave the green light for dividend and buyback increases, with JPMorgan boosting its dividend by 11% to $1 for the third quarter, and hence its annual yield to 2.65%; the highest among the peer group.

Earnings forecasts

Rising dividends are considered a sign of good health but growing profits are also required for the banks to be steadfast payers. According to forecasts, the second quarter generated softer revenues for the four largest banks in quarterly and yearly terms, with JPMorgan likely facing the largest pullback of 11.68% y/y. Nevertheless, net income may have remained comfortably elevated in yearly terms for all banks. Earnings per share (EPS) are said to have marked a similar trajectory, showing a robust annual growth of over 100% for the big four and a moderate contraction compared to Q1.

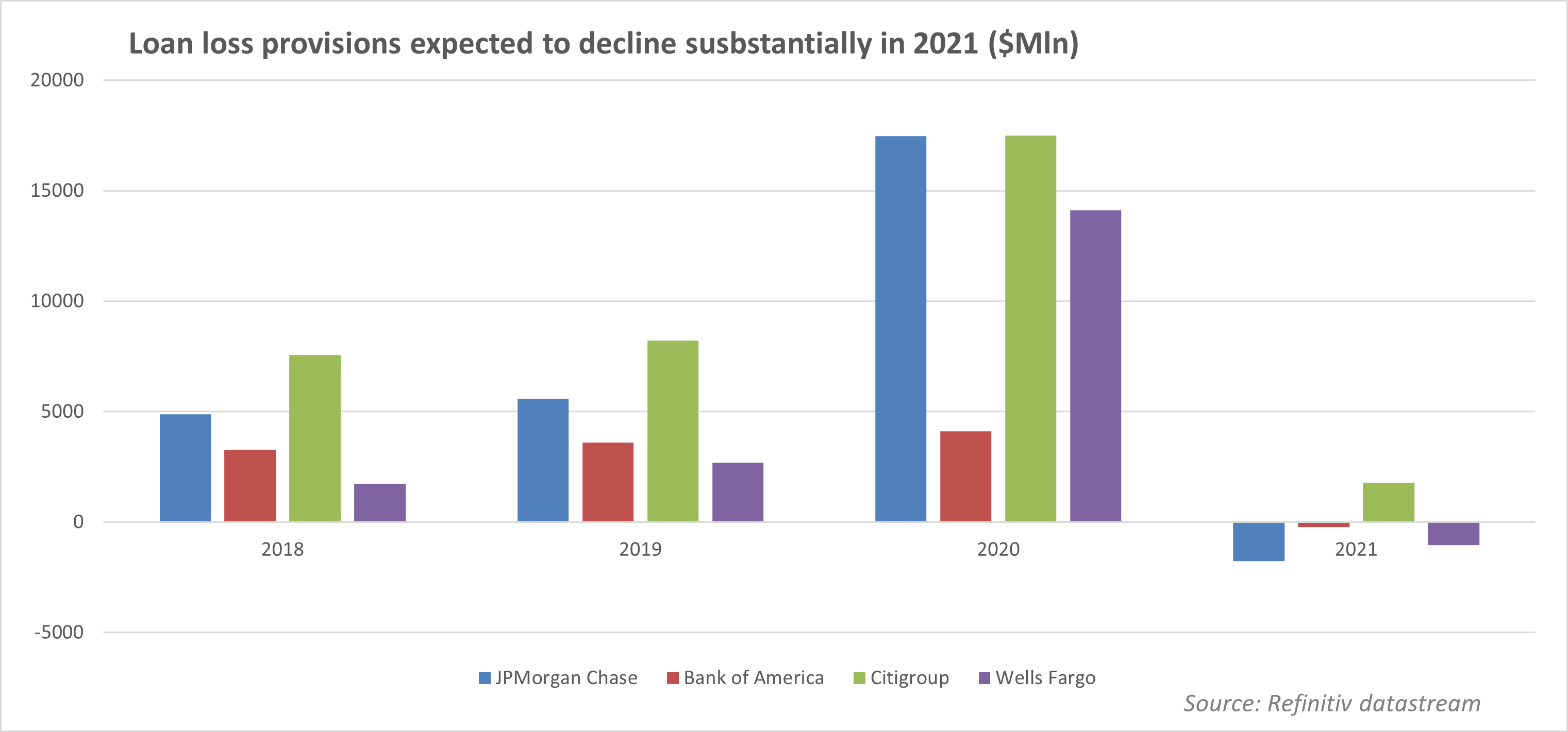

Perhaps a potential increase in loan loss provisions in Bank of America and Citigroup may raise some eyebrows about fears of uncollected loans but the additional amount could be relatively minimal to create any headlines.

Fed policy positive for banks

Apparently, consumers and businesses may retain a careful approach as regards their debt exposure as long as the Covid-19 battle continues, but the banking sector could still extract some benefits from wider net interest margins in the case hot inflation readings become more permanent and the Fed brings forward the timeframe of rate hikes. Particularly, Wells Fargo, which is heavily reliant on mortgage and car loan rates, could experience a tremendous expansion in margins. Biden’s infrastructure bill may also create new business contracts for banks.

Valuation metrics

Valuation metrics favour banking stocks as well. Although being overvalued is not a clear-cut sign to cash out at the moment as the Fed’s stimulus measures are keeping a strong footing under stock prices, traders remain sensitive to bubbly stocks such as the ones in the US tech sector. The same, however, cannot be told for the US banks. The forward price to earnings ratios for the next year for JPMorgan (11.66x), Bank of America (13.80x), Citigroup (7.47x)and Wells Fargo (11.38x) are well below the one for the S&P 500 of 21.3x. Hence, banking stocks can still be considered relatively cheap to buy.

Market reaction

Turning to the market reaction, optimism for flourishing earnings in Q2 has been partially responsible for the ongoing rally in stock prices. Therefore, should the earnings results echo that confidence, stock prices may not move dramatically.

However, how banks will perform in the second half of the year is still a puzzle given the unpredictable spectrum of Covid-19 and the still uncertain Fed tightening plans. Hence, any answers to this question could generate volatility in banking stocks next week.

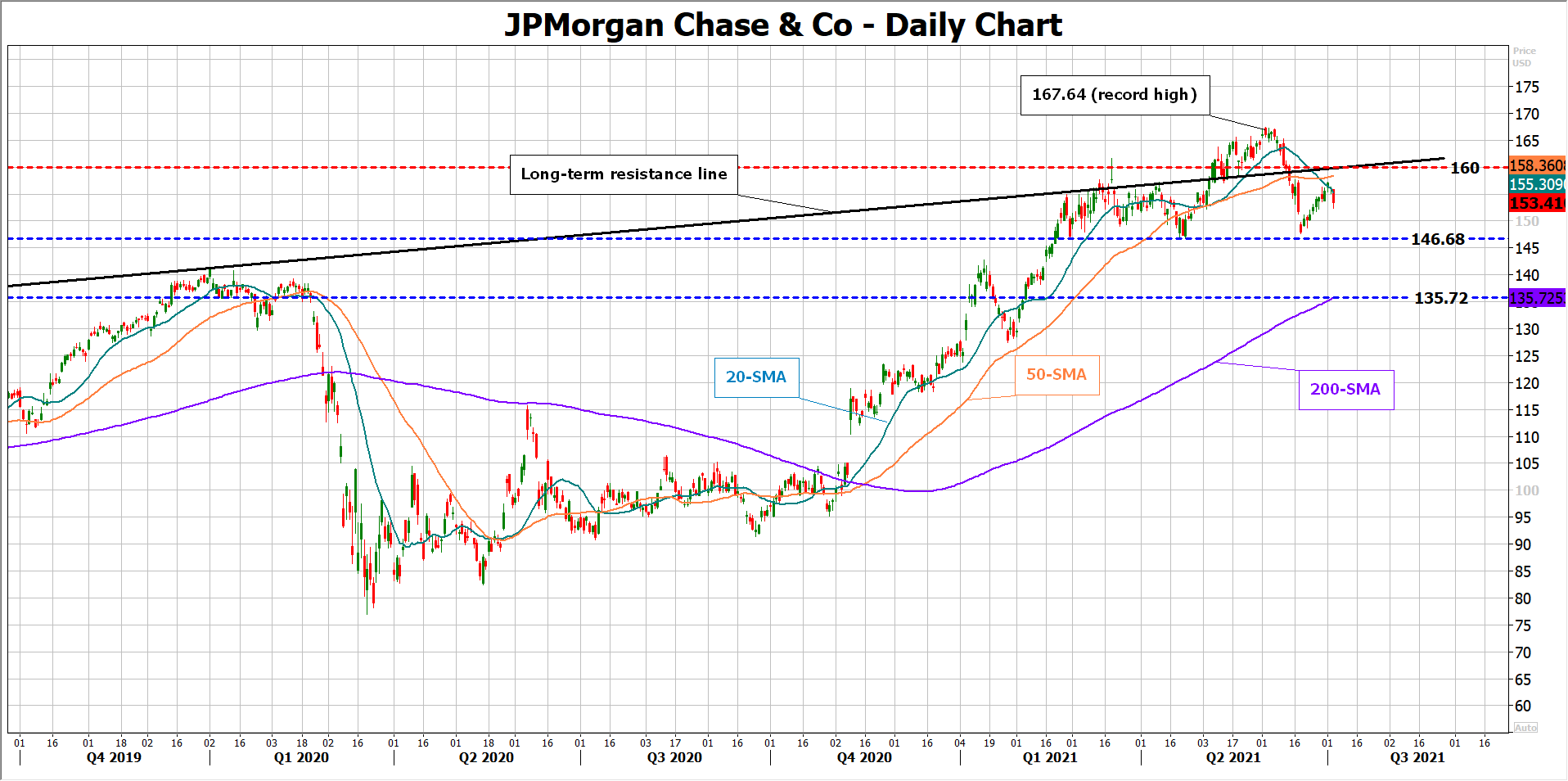

JPMorgan stock

Looking at JPMorgan’s stock, the price has fully reversed May’s rally but managed to stabilize the sell-off near its previous low of 146.68.

From a technical perspective, the decline has pushed the stock below the Ichimoku cloud, which has become a key resistance territory following this week’s pullback. The bearish cross between the 20- and 50-day simple moving averages is another negative sign, though this needs a confirmation as the lines have not diverged significantly yet.

Nevertheless, only a drop below 146.68 could raise selling interest, with the spotlight falling immediately on the 200-day SMA at 135.72 in this case.

Alternatively, the stock may need to gear back above the cloud and the broken long-term resistance line at 160.00 to shift attention back to the record high of 167.64.

Author

Christina joined the XM investment research department in May 2017. She holds a master degree in Economics and Business from the Erasmus University Rotterdam with a specialization in International economics.