US ADP December Preview: Suddenly its inflation, not jobs

- Private payrolls expected to slip to 413,000 hires, lowest since August.

- Nonfarm Payrolls forecast to revive after a weak December.

- Dollar rises across the board on soaring US Treasury yields.

American firms closed out the year with moderate hiring despite rampant pandemic cases in parts of the country, an unsettled economy and a newly assertive Federal Reserve.

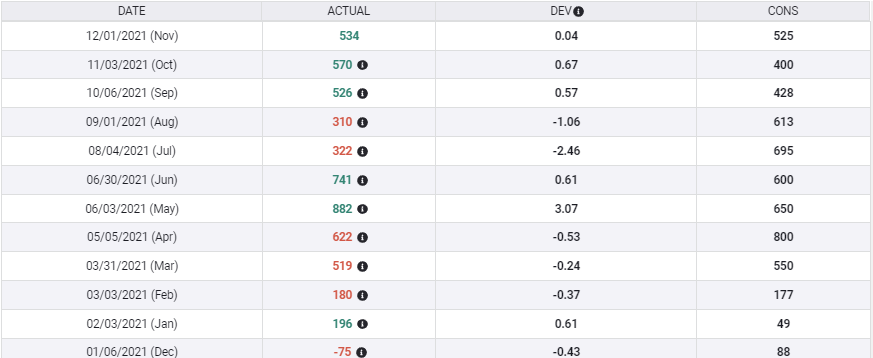

The clients of Automatic Data Processing (ADP) are forecast to have added 413,000 employees, the lowest since 310,000 in August, after averaging 543,000 in September, October and November.

ADP

FXStreet

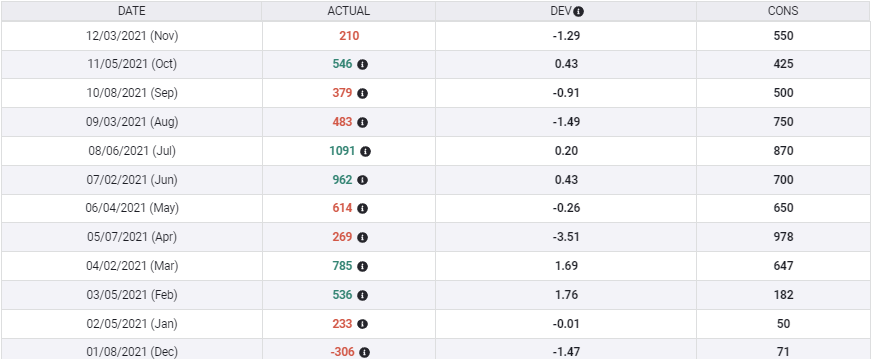

Nonfarm Payrolls are projected to nearly double to 400,000 in December following November’s disappointing 210,000, which was the weakest monthly total since the economy lost 306,000 jobs in December 2020.

NFP

FXStreet

Diagnosed cases of COVID in the last week of December reached a daily average of more than 265,000, an all-time record in the United States surpassing the prior high of 252,000 from January 11, 2021. Though hospitalizations and fatalities are rising, they are far below what they were last January. While some of the hardest hit states in the Northeast have reinstituted mask requirements and have attempted limited vaccination mandates, no government has tried or is contemplating economic closures.

ADP and NFP

Though the two reports draw their data from the US labor market, they are quite different in concept and their monthly results have been poorly correlated since the pandemic took hold in March 2020.

The ADP employment total is simpler and more accurate, but less encompassing. Its National Employment Report records the net employee additions or subtractions of the firm's 460,000 US clients covering about 26 million workers. Payroll services are exclusively in the private sector and do not cover government employment at the local, state or federal level.

The Employment Situation Report from the US Labor Department attempts to catalog the entire American employment market in one document. Known colloquially as the Nonfarm Payrolls (NFP) for its most quoted statistic, it tracks both hirings and firings as reported to the government and estimates the number of new jobs created each month but not on government books. The combination of actual job figures and these projections produce the monthly NFP number. The monthly estimates are compared to the tax rolls once a year and adjusted to reflect the correct number of jobs gained or lost.

Labor market

Labor market data suggests that job availability remains high and employers are keeping current workers as best they can.

The four-week average of Initial Jobless Claims dropped to 199,250 on December 24, its lowest count in 52 years, since October 25, 1969.

Initial Jobless Claims, 4-week moving average

FXStreet

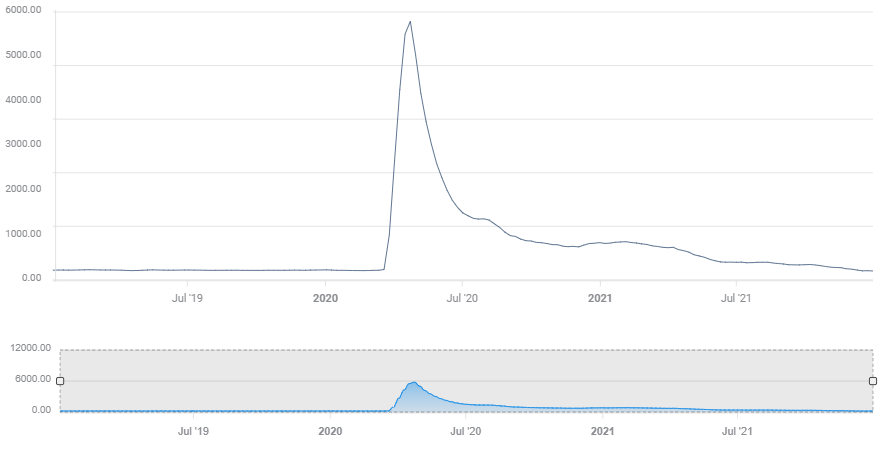

Unfilled positions in the Job Openings and Labor Turnover Survey (JOLTS) averaged 10.695 million from June through November, with an all-time record of 11.098 million in July. In comparison, the highest one-month total prior to this year had been 7.574 million in November 2019.

JOLTS

FXStreet

Purchasing Managers’ Employment Indexes (PMI) from the Institute for Supply Management (ISM) indicate that hiring has been restrained by worker shortages rather than lack of opportunities. The services Employment PMI was 56.5 in November with December's version due on Thursday, January 6. The manufacturing Employment PMI for December came in at 54.2, better than the 53.5 forecast and November's 53.3, for the highest score since April 2020.

Nonfarm Payrolls have averaged 612,000 for six months to November, the best record since the initial recovery from the 2020 lockdowns. The half-year has been unusually volatile ranging from 1.091 million in July to 210,000 in November.

Conclusion

Credit markets have taken the Federal Reserve’s December rate prognosis to heart. Soaring consumer inflation evoked a doubling of the bond purchase taper to $30 billion a month at the December Federal Open Market Committee (FOMC), ending the program in March and clearing the path for a fed fund increase at that month’s meeting.

The Fed’s own rate projections envision three rate increases by the end of 2022 with a 0.9% estimate for the fed funds. Futures traders agree. The Chicago Board Options Exchange (CBOE) fed funds futures rated the odds for three hikes by year end at 68.8% at the close on Monday.

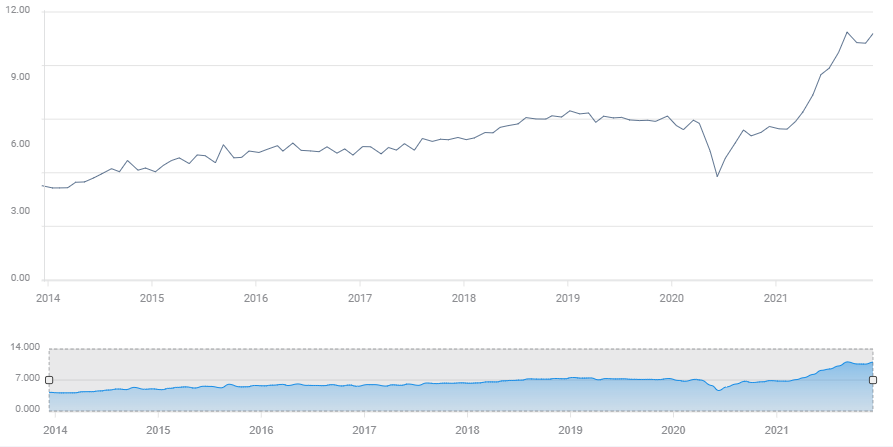

Despite the Fed’s clear signal at the December meeting, Treasury rates barely responded in the final two weeks of the year. The 10-year yield gained just 5 basis points from the close of the December 15 FOMC at 1.462% to the final quote of the year at 1.512% on December 31.

10-year Treasury yield

CNBC

Monday was a different story. The first trading day of 2022 saw the 10-year return jump 12 basis points to 1.63%, as yields rose across all terms.

Inflation has become the Fed’s chief concern. As long as hiring continues at a moderate or better pace, economic assumptions about the US will remain unchanged and monetary policy will stay fixed on consumer prices. Hiring would have to drop to near zero for the governors to rescind their latest policy twist.

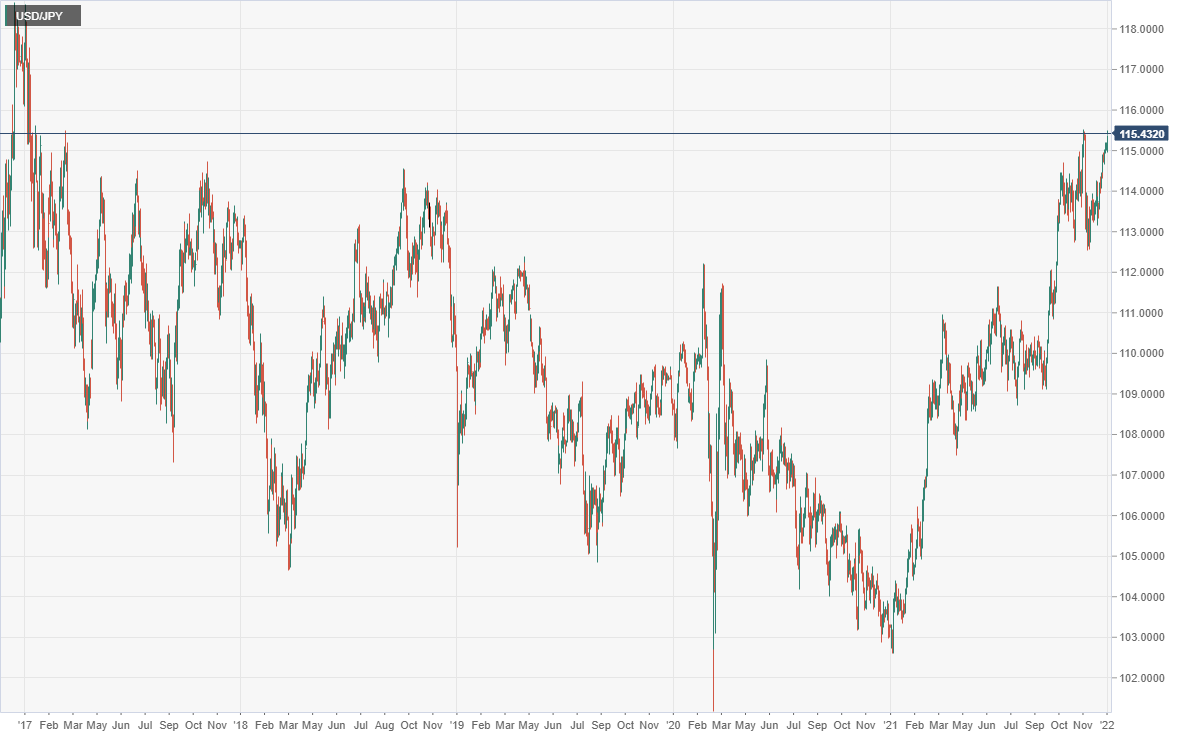

The US dollar answered the yield charge forcefully, rising in all major pairs. The USD/JPY closed at 115.35 on Monday, just two points below its five-year high.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.