United States: The economic consequences of political polarization

‘Economic voting’ -the possible influence of the economic environment on voting behavior- has been the subject of intense debate over the past three decades. A key question in this respect is whether individual economic perceptions are influenced by the political affiliation of voters and if so, whether this influences spending. On both questions, the results of empirical research in the US are not conclusive. With respect to company investments, the conclusion is unambiguous: polarization exerts a negative influence. This last point is enough a reason to argue that the significant increase in political polarization in the US in recent decades matters from an economic perspective. In addition, there is a concern about what it means for economic policy and the ability to act swiftly when circumstances require so.

In the run-up to this year’s US presidential election, many commentators will inevitably think of the phrase “It’s the economy, stupid”, coined by James Carville, the strategist of Bill Clinton’s campaign in 19921. Economic performance may again matter in the voting behaviour of the electorate on 5 November, but the question is how. Will voters look in the rear-view mirror at the huge increase in inflation in 2021 and early 2022 and its detrimental impact on purchasing power or will they focus on the big drop in inflation since the latter part of 2022? Will they pay attention to high mortgage rates, or will they find comfort in the ongoing strength in the labour market? This topic, known as ‘economic voting’, has been the subject of intense debate over the past three decades2. A key question is whether individual economic perceptions are influenced by the political affiliation. In such case, economic perceptions could influence voting behavior, but these perceptions would be ‘coloured’ by the political affiliation of the voters3. Lewis-Beck and Martini (2020) analyse whether the voters’ perception of the economy -is it improving or weakening- is correlated with developments in terms of inflation, the equity market and real GDP growth. They find that “voters’ retrospective evaluations of the national economy track real changes in the US economy.” Adding party identification as an explanatory variable does not significantly improve the regression results. This would mean that voters’ perceptions correspond to economic reality. However, other research shows a partisan bias. Households’ inflation expectations are lower when their preferred party controls the White House. “During the Barack Obama presidency, Republicans had higher inflation expectations than Democrats. This partisan gap reversed when Donald Trump was elected… When Joe Biden was elected, the partisan gap reversed again.4” Other researchers find, based on survey data, that people “who affiliate with the party that controls the White House have systematically more optimistic economic expectations than those who affiliate with the party not in control.5” However there is no evidence that this leads to increased spending. The authors conclude that “economic optimism driven by partisan bias reflects ‘cheerleading’ instead of actual expectations of income growth.” Other authors come to a different conclusion and find that following presidential elections, “consumption increases in areas allied with the winning presidential candidate and decreases in those areas where affiliations lie with the losing candidate.6”

People feeling different about the economy based on party affiliation is a manifestation of political polarization. Other examples are extreme differences in views, along partisan lines, amongst politicians as well as their voters on a broad range of topics, people having negative feelings or even disliking members of the other party, the so-called affective polarization7, etc.

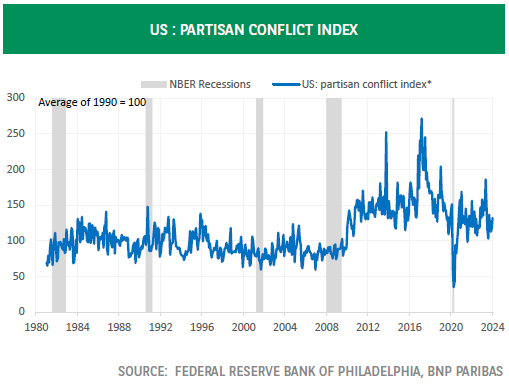

Based on the media coverage of political disagreement about government policy, polarization has seen a significant increase after the global financial crisis (chart)8. Other indicators show that polarization has been on the rise since the 1970s. In theory this could have negative economic consequences due to short-termism of economic policy (‘myopic policies’), political gridlock making it difficult to enact necessary policies and an increase in policy uncertainty. In case of affective political polarization, firms could also face risks in their product markets9. One would expect company investments to be particularly sensitive to these factors. Marina Azzimonti (2018) finds a persistent negative relationship between political polarization and aggregate investment. This result is confirmed even when controlling for the influence of economic policy uncertainty and the macroeconomic environment. She estimates “that about 27% of the decline in corporate investment between 2007 and 2009 can be attributed to a rise in partisan conflict.” Qiaoqiao Zhu analyses this topic at the level of US states and finds that “a one standard deviation increase in political polarization results in a 1% decline in investment or a 16% reduction relative to the mean investment rate.”10 Moreover, this effect is almost entirely driven by inland firms, which lack the mobility to invest across state borders. Unsurprisingly, there is also a negative impact on employment growth.

The empirical research can be summarized as follows. Firstly, certain authors find that households’ economic perceptions are not significantly influenced by partisan affiliation, whereas others report that voters who affiliate with the party that controls the White House are more optimistic about the future. Secondly, there is conflicting evidence whether this upbeat feeling influences spending. Thirdly, with respect to company investments, the conclusion is unambiguous: polarization exerts a negative influence. This last point is enough a reason to argue that the significant increase in political polarization in the US in recent decades matters from an economic perspective. In addition, there is a concern about what it means for economic policy and the ability to act swiftly when circumstances require so.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.