UK Inflation Preview: Sterling needs Goldilocks CPI to rise ahead of the BOE

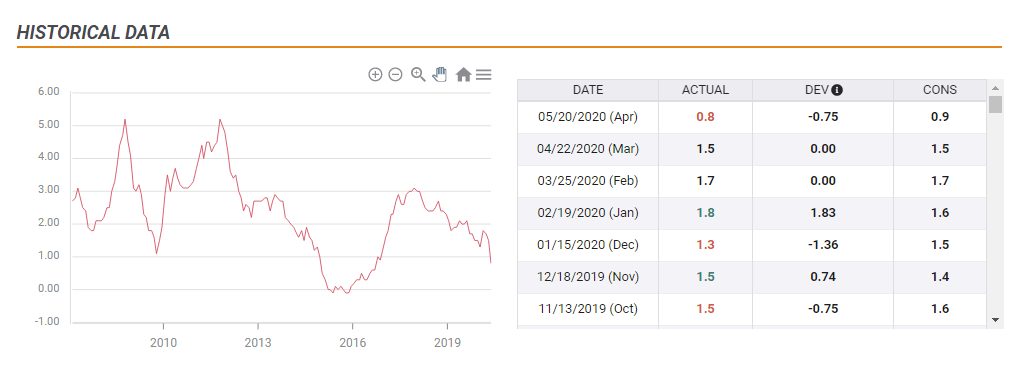

- UK inflation has likely extended its fall to 0.5% yearly in May.

- Coming 24 hours ahead of the BOE, the size of QE and tone on negative rates may move.

- GBP/USD is sensitive to any developments amid ongoing Brexit and coronavirus uncertainty.

The rush to buy toilet paper is over – and even the bounce in oil prices is unlikely to have lifted inflation. Consumer Price Index figures for May are set to show another fall, and the Bank of England is watching it ahead of its decision on Thursday.

The economic calendar is showing a potential drop from 0.8% in April to 0.5% in May. CPI floated well above 1% in the pre-pandemic era. The crash in demand due to the efforts to cub coronavirus have been outweighing localized supply issues.

A drop to 0.5% would send inflation to the lowest since 2016 before sterling's post-referendum slump sent it back up. The BOE's target is 1-3% and it will likely miss it not only in April and May this year but for many months to come.

Potential reaction – it all depends on the BOE

CPI is published on Wednesday, ahead of the BOE's decision on Thursday. The "Old Lady" is on course to expand its Quantitative Easing program by between £100 to £150 billion on top of the current £645 billion.

Contrary to the days preceding coronavirus, investors cheer money-printing as it allows governments to stimulate the economy – worries about devaluation seem to belong to history.

Following this logic means lower inflation would trigger more BOE action – turning bad news into good news for sterling.

However, the London-based institution is also considering setting negative interest rates – and that would already depress the pound. Andrew Bailey, Governor of the Bank of England, said in May that the topic is "under active consideration." Other officials also publically toyed with the idea. While most of them hinted the move is not imminent, setting sub-zero borrowing costs remains an option.

If inflation falls too fast, real interest rates would cease to become accommodative – with borrowing costs exceeding price rises. That could lead the BOE to move in that direction.

For the pound to rise, CPI would need to hit the sweet spot of between around 0.3% and 1% – showing that inflation is low and that more QE would help.

If inflation surprises with over 1%, it could result in less stimulus from the BOE – perhaps under £100 billion in new funds, thus sending sterling down.

On the other extreme, CPI that is close to 0% – and especially negative CPI, deflation – would already raise the specter of negative rates, potentially punishing the pound.

Apart from the BOE, GBP/USD has been moving on fresh Brexit hopes following a video-call between Prime Minister Boris Johnson and several EU officials. However, the lack of details causes doubts among investors.

Other concerns are coronavirus, with cases remaining stubbornly high in both the US and the UK. Volatility remains high and cable is sensitive to any developments.

Conclusion

CPI is set to move sterling, yet an increase depends on meeting expectations – not too hot nor too cold. Investors will have the BOE in mind.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.