UK economy contracts as winter recession risks grow

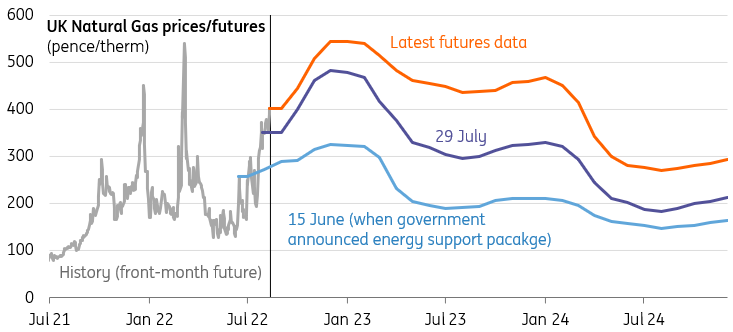

The fall in UK GDP during the second quarter was largely down to noise. But the risk of recession is rising quickly, with gas futures hitting new highs for next winter and our latest estimates suggesting the household energy price cap could come close to £5,000 in the second quarter of next year. Much now depends on fiscal policy announcements in the autumn.

UK GDP falls in the second quarter

It goes without saying that the latest UK GDP figures are very hard to read. Quarterly output fell by 0.1%, which is almost entirely down to the addition of an extra bank holiday for the Queen’s Jubilee in June, as well as the winding-down of Covid-19 testing/vaccine rollouts through the quarter. Admittedly the impact of the bank holiday was noticeably less than in previous years. The hit to manufacturing, wholesale/retail, transport and construction was generally more muted than during the 2002/2012 jubilee events, which probably reflects changes in the way the economy operates – not least the advent of online shopping.

Either way, an artificial rebound in July should see monthly GDP rise by roughly 0.7%, and overall third-quarter GDP by around half a percent. That means discerning the impact of the cost of living squeeze is going to be tricky for the next few months, at least in terms of the GDP figures. But by the fourth quarter, the signs of recession are likely to be more apparent.

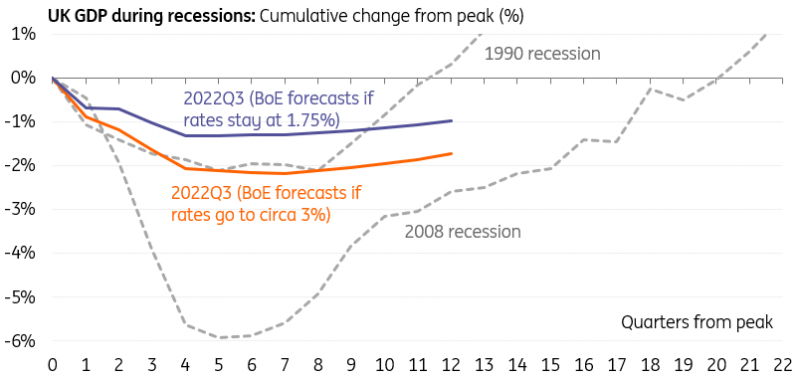

Bank of England is forecasting a 2% hit to GDP, though this assumes no further government support

Macrobond, Bank of England, ING

Household energy costs could hit £5,000 next year

At its latest meeting, the Bank of England forecasted approximately a 2% fall in GDP over the next couple of years, spread over five quarters of negative growth. Crucially though this prediction relies on a) an assumption that the Bank rate will need to go as far as 3% (which isn't our base case) and b) that fiscal policy will not respond. There’s little doubt now that the fiscal response of the new prime minister in September will be key to whether the Bank of England’s forecasts come to fruition.

Back in June, then-Chancellor Rishi Sunak announced just over £1,000 per household on means-tested benefits. At the time, we estimate that the household energy cap would have risen from roughly £2,000 to just over £3,000 by early 2023, based on futures prices back then and the new Ofgem formula. In other words, the support on offer would have roughly neutralised this increase for those in the lowest income deciles.

However, if we plug in the latest wholesale gas and electricity prices into the Ofgem spreadsheet, the cap is now likely to hit around £3,500 in October and could potentially get close to £5,000 by the second quarter of next year (though should fall back more noticeably later in the year). While such estimates are very volatile, it does mean that whichever candidate wins the leadership contest will be under huge pressure to significantly ramp up the size of those support payments.

We'll have to wait and see what the new prime minister offers in terms of support, but at the very least a fall in fourth-quarter GDP now looks highly likely.

Gas prices are hitting fresh highs ahead of this winter

Source: Macrobond, ING

Read the original analysis: UK economy contracts as winter recession risks grow

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.