Transport and logistics sector enters new phase of recovery – But there are headwinds

The global transport and logistics sector recovery is entering a new phase, and we're expecting substantial growth in 2022 – despite the war in Ukraine and continued supply chain disruption.

Second phase recovery from the pandemic for transport and logistics

The global transport and logistics sector will see another year of substantial growth in 2022, despite setbacks from the Ukraine war and ongoing lockdowns in Chinese port cities. The recovery is entering its second phase, but it is showing two faces. While dominant goods logistics is expected to enter a phase of moderation after a strong rebound driven by the shift to goods consumption, passenger transportation is expected to take over with a significantly stronger recovery from last year’s pandemic lows.

In 2021, passenger transportation suffered from ongoing Covid-restrictions leading to a disappointing year, but in most parts of the world, travel restrictions have been eased which will now trigger more traffic. For many office workers and commuters in developed countries, hybrid ways of working have been implemented, with people back in the office but also working from home more than before the pandemic. After a long period of limitations and postponed travelling, we expect that pent-up demand, especially in leisure airline travel, will be fulfilled over the course of 2022.

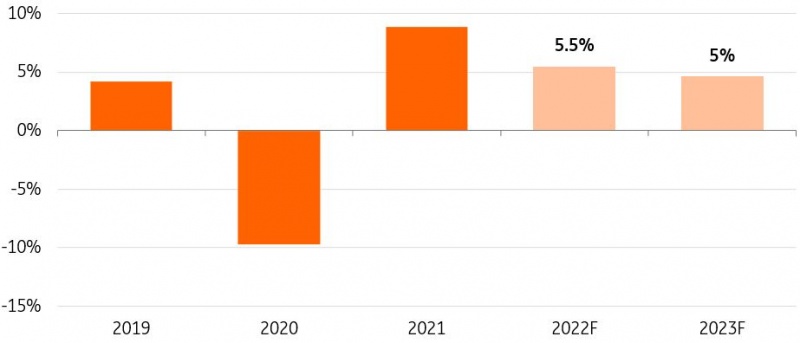

Recovery in global transport and logistics continues on the back of the return of travel

Value added transport, logistics and storage sector

Source: Oxford Economics, ING Research

Airlines and public transport are drivers of sector growth

After a second year of losses, airlines expect to see a natural rebound of leisure travel in 2022 from unprecedented pandemic lows, with travellers eager to resume their journeys after two years of limited leisure travelling. Many consumers saved money for holidays which has made higher ticket fares less offputting. In a consumer survey in the US last year, 22% of respondents said they held back spending in order to be able to travel once it was more accessible. Airline bookings – especially for continental trips – with Easyjet and Ryanair in Europe, for instance, and Jetblue and Southwest in the US, suggest a solid uptake in the run-up to the summer holiday season. An exceptionally strong return of cruise bookings with US-based liner Carnival is also a sign of returned holiday travel enthusiasm. However, recovery will be uneven across airlines and routes and business travel is expected to lag (+link to aviation).

In everyday passenger transport on road and rail (public transport), we also see a significant rebound over the first quarter of the year. Figures for travelling to transit stations reveal a rebound to levels between 70% to 95% in European countries, and some 75% in the US compared to the pre-pandemic baseline. Recovery is expected to continue this year, which drives general growth in transport in 2022.

Ukraine war limits the upside for sector growth, especially in Europe

The war in Ukraine has major implications for aviation and shipping. We expect world trade to flatten this year if the war carries on. Although recovery continues in transport and logistics, the conflict clearly slows volume growth, especially in Europe, with formal and voluntary sanctions on trade and a weakening general economic perspective due to rising prices and increased uncertainty around global growth perspectives. This is on top of the inefficiencies of disrupted supply chains and ongoing elevated transport prices (+link) pushing up costs of trade. Estimated average westbound container costs from Asia to Europe surged from 2-3% to 10-15% of product value by the end of the first quarter compared to two years ago. As the manufacturing sector still holds up quite well with order books fairly filled, the impact of slowing demand for goods may materialise more in 2023, but this also depends on how the Ukraine war evolves.

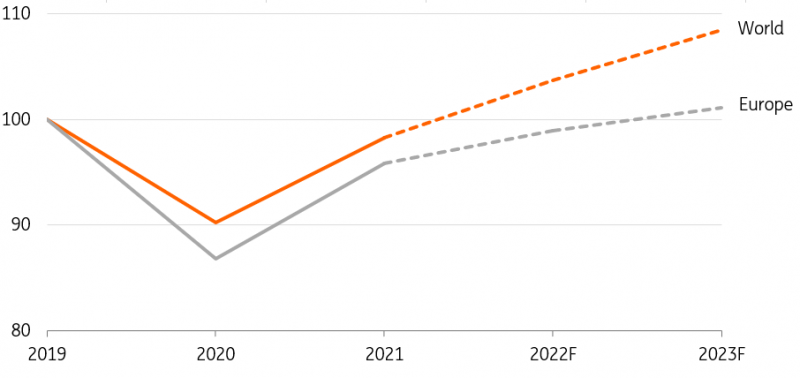

Still, the rebound in aviation and public transport will lead to solid average growth figures, but without the war in Ukraine the recovery would have been stronger. On a global scale, we expect the average total sector volume to exceed pre-pandemic levels by the end of 2022. As trade relations between European countries and Russia and Ukraine are more intensive than elsewhere in the world, the economic impact of the war and the imposed sanctions are more severe in Europe. Together with the mature character of the recovery in goods transport, this leads to lower expected growth perspectives.

Global transport and logistics sector to exceed pre-pandemic level in 2022

Value added transport, logistics & storage sector (index, 2019 = 100)

Source: Oxford Economics, ING Research

Three ways the Ukraine war impacts transport and logistics

The war in Ukraine significantly impacts shippers and transport and logistics companies, adding to ongoing supply chain challenges due to the pandemic. Among the most important implications for transport and logistics are:

- Demand: weakening economic and trade perspective flattens demand for goods.

The surge in inflation is weighing heavily on consumers but also producers. Consumers in Europe already revised buying expectations down, while for some producers it is too costly to produce at all at high gas prices.

- Costs: soaring fuel costs (and higher costs of transport equipment) means transport costs go up.

High fuel costs impact financial results the most for transport companies serving consumers directly, like airlines, but also cruise shipping and parcel transporters. European diesel prices have risen more sharply than gasoil prices because of dependency on Russian diesel supply. Higher raw prices for metals and other raw materials have led to price hikes in transport equipment as well.

- Supply disruption: new capacity constraints in the air and on land, re-routing in shipping.

Capacity pressure continues to drive the year for transport companies and the Ukraine war adds to frictions again. For airfreight, the closure of airspaces leads to new capacity reductions. Russian freighters are dropped out of global service, and routes between Europe and destinations in Korea and Japan are redirected to avoid Russian airspace taking hours longer and possibly requiring stopovers, leading to inefficiency and new capacity pressure, and higher prices/costs. On land, the Eurasian railway – which grew to handle around 1.5 million containers (TEU) over the last five years (representing more than 5% of total eastbound-westbound container traffic) – is now avoided by logistics services providers and several shippers. Some try to re-route south via the Trans-Caspian route, while some shift to sea, but both options mean longer lead times.

Russia and Ukraine are important suppliers of oil products, gas, coal, iron ore, metals and agricultural products like grains. The war and the imposed (self) sanctioning leads to major shifts in sourcing to other countries and the reshaping of trading routes. In our shipping piece, we take a closer look at this. On balance, this may lead to longer voyages in shipping. Attempts will also be made to shift part of the grain exports from Ukraine to Europe to rail.

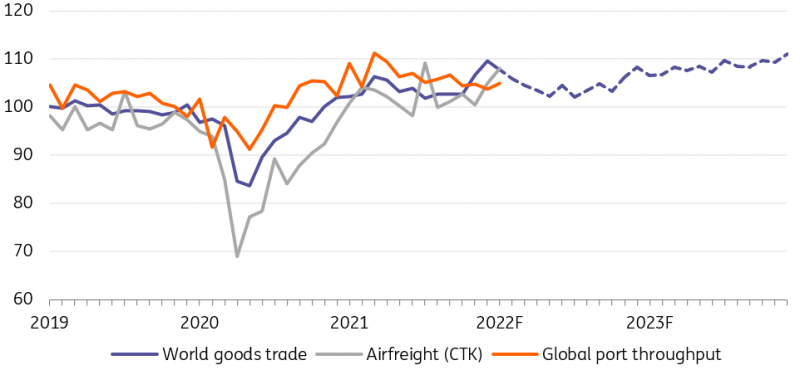

World trade slows above pre-pandemic levels in 2022

Indices global trade, airfreight traffic and global ports throughput (2019 = 100)

Source: CPB, IATA, RWI, ING Research

Global trade faces headwinds because of enduring supply chain frictions and sanctions

Trade is a strong indicator of global transport development, especially in shipping and logistics. After a double-digit rebound beyond the pre-pandemic level in 2021, we have already witnessed a slowing in 2022, and the implications of the war in Ukraine will weigh more heavily on trade than on the global economy. We expect global trade volume to flatten this year, but still remain on the positive side. Higher year-on-year demand for oil products and intra-regional trade growth (such as for building materials) especially support trade. Also, international e-commerce will persist as a driving force after a surge during the pandemic.

Supply chain disruption and higher costs are not expected to improve trade conditions

The purchasing manager indices in the manufacturing sector still provide positive signs for trade and transport in the short run. Filled order portfolios in the US and Europe seem to secure growth. But at the same time, important manufacturing industries like automotive continue to struggle with shortages (see box: rethinking sourcing). The supply constraints limit production levels and consequently trade and transport demand.

How will supply chain frictions evolve further into 2022?

Port congestion and backlogs started to ease in the first months of the year, leading to a substantial improvement in the US LA-Longbeach port bottleneck. However, the war in Ukraine and related avoidance of ports and vessels combined with a new lockdown at the world’s largest global container port region, Shanghai, put the global supply chain network to the test again. Estimated Far East-Westbound timeliness (cargo ready ex-works to port of destination departure) reached a new high in April which adds to existing delays in supply chains. It’s uncertain how these events will evolve, but the impact will at least be felt for several months ahead. Consequently, imbalances are expected to drag on through the year.

Rethinking supply chains may revise logistics patterns, but not immediately

Among transport and logistics clients, supply chain resilience is top of mind. Logistics players such as Dachser and UPS note that clients are looking at ways to reduce supply risks and increase reliability. Efficiency and lowering cost are no longer the leading focus, with damages following production interruptions and workarounds and this could impact transport. What are the options?

-

More buffer stocks (just in case inventory).

-

Longer contracts with suppliers and transport partners.

-

Investment in own containers and transport capacity.

-

Multi-sourcing.

-

Reshoring or nearshoring (regionalisation).

Trade and transport are under reconsideration, but at the same time fundamentals of trade still hold. Research so far shows the pandemic hasn’t marked the end of globalisation yet and labour shortages and high energy prices make reshoring more expensive. Consequently, despite higher trade costs, we don’t expect a rush in reshoring, and perhaps rather nearshoring, with a focus on diversification.

Cross sectoral and global cost pressure for transport companies – pricing power helps

For many companies, this year is marked by rising costs of fuel, wages, and transport equipment. The aviation and shipping sectors are the most energy-intensive. In aviation, specifically, this complicates the return to profitability, while the highly-fragmented trucking sector is also affected. For the latter, the positive thing is that shortages of drivers and transport equipment have lifted pricing power in the US, UK and EU, but wages and sub-contractor rates have gone up as well. With the market volumes and pressure on capacity easing further into 2022, it will most likely be less profitable for most road haulage companies.

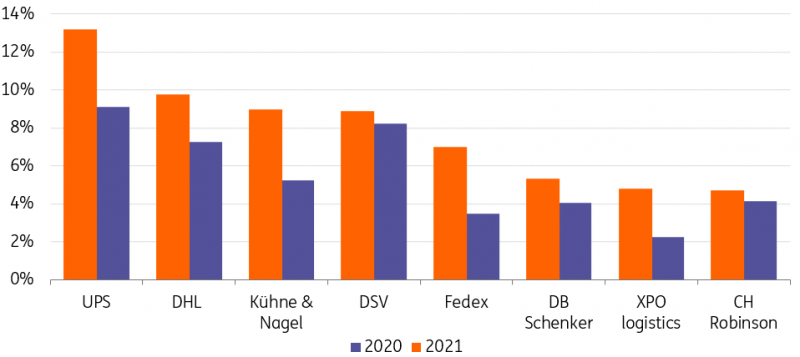

Logistics services providers boosted margins amid rebound and disruption

Operational margins of large global logistics sercvices providers (EBIT) in % per year

Source: Annual reports, ING Research

Logistics services providers entered a more challenging year

The profitability of large global logistics services providers active in sea and airfreight soared amid increasing volumes and spiking tariffs in 2021 (chart). The year ahead, however, will be more challenging because of the market, but also because of competition. Last year, logistics companies benefited strongly from earlier fixed-term contracts with container liners, that offered a high margin on the spot market. But as container liners shift more into term contracts with clients, they will try to deal with large shippers themselves more often. Consequently, margins are likely to have peaked and will erode in 2022.

A positive note for logistics services providers active in parcel is that at least higher e-commerce volumes over the pandemic are here to stay. UNCTAD figures show that the online share of total sales of goods is close to 25% in the UK, China, and Korea in 2020. Other parts of the world are lagging, indicating that there’s generally ample room for bolstering growth.

Read the original content: Transport and logistics sector enters new phase of recovery – But there are headwinds

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.