Three fundamentals for the week: US GDP, BoJ and the Fed's favorite inflation gauge stand out

- Economists expect the US to report a slower growth rate of 2.5% in Q1 2024.

- The Bank of Japan is set to leave rates unchanged after its historic hike in March, which failed to lift the Yen.

- The Fed´s preferred inflation gauge, core PCE has the final word of the week.

While it is hard to predict when geopolitical news erupts, the level of tension is lower – allowing for key data to have its say. This week's US figures are set to shape the Federal Reserve's (Fed) decision next week – and the Bank of Japan (BoJ) may struggle to halt the Yen's deterioration.

Here are this week's main events:

1) US GDP carries low expectations

Thursday, 12:30 GMT. The first release of Gross Domestic Product (GDP) tends to have a significant impact on markets. The initial read for the first quarter of 2024 is projected to show an annualized increase of 2.5%, down from 3.4% in the last three months of 2023.

The world's largest economy defied expectations for a recession in 2023. Such strong growth solved the dilemma for the Fed – it managed to keep interest rates high for longer, extending the fight against inflation.

Are elevated borrowing costs finally catching up with the economy? A 2.5% growth rate is still solid, better than in Europe, the UK and other developed economies. Moreover, there is room for an upside surprise.

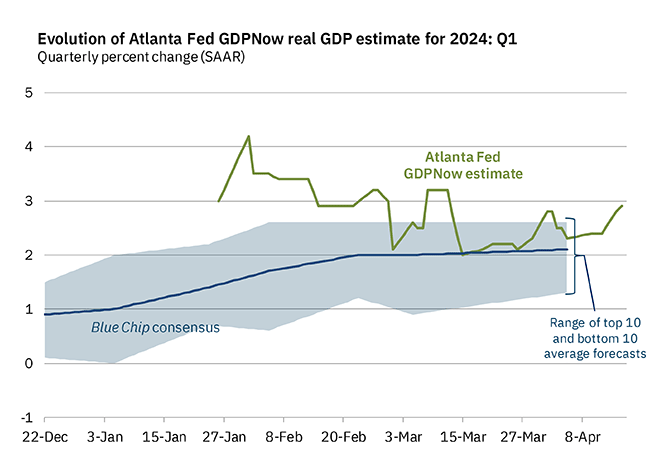

According to the Atlanta Fed's NowCast, the economy expanded by 2.9% in the first quarter. Better-than-expected data would boost the US Dollar (USD), weigh on Gold, and have a mixed impact on stocks. Companies need lower rates, but also more sales.

GDP Now. Source: Atlanta Fed

A disappointing figure would provide hopes for a rate cut coming sooner rather than later, sending the US Dollar down and Gold up..

Apart from the headline figure, the inflation indicator used to measure real GDP is also of interest. Investors want to see the "deflator", as it is often called, falling. A hot figure would weigh on markets.

Bank of Japan may warn about weak Yen

Friday, in the Asian morning. The Bank of Japan (BoJ) announced its first rate hike since 2007 last month – but that only brought borrowing costs to range between 0% and 0.10%. Moreover, that has not helped in buoying the struggling Yen.

Investors were unimpressed by Japanese officials' signal to intervene and boost the currency. A joint statement by the US, Japan and South Korea referring to the weakness of these Asian currencies also failed to move the needle.

Japan relies on energy imports, which are denominated in US Dollars. Higher gasoline prices are not the kind of inflation the BoJ aims for.

The one thing the BoJ could do is raise interest rates again – or at least indicate such a move. Will Governor Kazuo Ueda provide hawkish hints? That is the question for the upcoming BoJ gathering, as no rate hike is on the cards now.

A hawkish tone could also push other central banks to avoid immediate rate cuts, thus strengthening currencies such as the Euro and the Pound. If the BoJ avoids bold promises, the Yen would further weaken.

Core PCE is critical for the Fed decision

Friday, 12:30 GMT. Five days before the Federal Reserve announces its rate decision, officials will receive an updated inflation figure – the one they care about most. The Personal Consumption Expenditure Price Index (PCE) is more frequently updated than the Consumer Price Index (CPI). Despite being released after the CPI, the PCE is of high importance.

Core PCE has been falling, but got stuck in recent months:

Core PCE YoY. Source: FXStreet

The economic calendar points to a repeat of last month's 0.3% MoM increase in core PCE in March. More importantly, and despite the hotter CPI figures, core PCE YoY is expected to slide to 2.6% from 2.8%. The bank's goal is 2%.

Every tenth matters and a hot 2.7% or 2.8% read would weigh heavily on stocks and Gold while boosting the US Dollar. It would further push back estimates for a rate cut. A 2.6% figure or lower would be welcome news for markets.

Surprises are uncommon in PCE reads, as they are based on CPI, the Producer Price Index (PPI) and other figures that have already been released. Nevertheless, the Fed is focused on inflation and cares about its favorite gauge. Markets care as well.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.