The need-to-knows ahead of four July

-

After 14 years of Conservative rule, polls and prediction markets indicate a Labour majority government led by Keir Starmer as the most likely outcome in the next general election due on 4 July.

-

Despite the challenges of overturning more than 100 constituencies, the struggles faced by the Tories and the SNP make a Labour victory most likely.

-

We expect the market impact to be limited given the limited fiscal headroom and the ghost of the 2022 “mini”-Budget still enforcing fiscal responsibility.

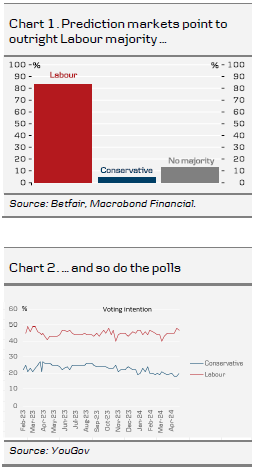

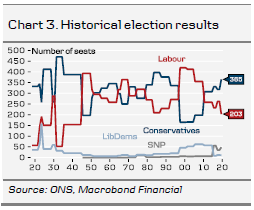

After 14 years of Conservative party rule, a Labour majority government led by Keir Starmer is at present the most likely outcome after the general election according to both polls and prediction markets (chart 1 and 2). To secure the outright majority, Labour will need to overturn 123 constituencies. This follows the worst post-war defeat for the Labour party in 2019. By comparison, only 59 seats were required in the 1997 election, which secured a landslide Labour win (chart 3). However, with the headwinds that have faced both the Tories and the Scottish National Party (SNP) the past years, a Labour victory is in the cards.

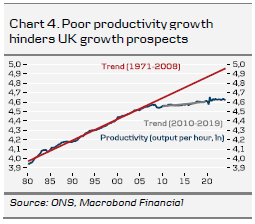

Regardless of the election outcome, fiscal policy is likely to remain constrained in light of the large public debt and in the absence of a noteworthy improvement in the structural outlook (e.g. productivity growth, see chart 4). In March, the UK fiscal watchdog the OBR, estimated that the fiscal headroom is historically slender at GBP 8.9bn against the objective of lowering the debt-to-GDP ratio over the rolling five-year forecast horizon. This has led both parties to campaign on the notion of fiscal responsibility. Likewise, Labour has watered down policies such as the GBP 28bn a year green investment pledge following questions on funding. While the respective election manifestos have not been presented yet, we aim to outline key policies and respective differences below.

Key policies: Spending, taxes, EU, Brexit and the BoE

Spending and taxes. With the tax-burden set to rise to the highest level post-war according to the OBR, neither party has unsurprisingly been eager to outline plans to increase taxes. On balance, we expect Labour to prove more inclined to fund increased spending via tax raises (e.g. removing the tax break for private schools and targeting taxes on wealth). Additionally, Labour is set to have more focus on industrial policy, labour market reforms and decentralisation aimed at boosting supply as highlighted by Starmer. As outlined by chancellor Hunt, a Conservative government would likely prioritise continued cuts to National Insurance contributions (NIC) with an eventual ambition to scrap it altogether. Conversely, Labour party is likely not to deliver further cuts to NIC with its ties to pension funding. More details on Labour policy is presented in Box A below.

EU and Brexit. While a Brexit reversal is highly unlikely under the rule of either party, we expect a more cooperative stance toward the EU under a Labour government. A smoother implementation of post-Brexit regulation would initially be positive for the UK economy and UK assets, boosting growth and improve the supply side. However, we highlight the risk of the political process falling short of expectations leaving the lasting impact more muted, which has also been the case previously.

BoE.We expect neither government to interfere with either the inflation target nor the BoE’s independence. Last month, former Labour PM Gordon Brown proposed reverse tiering on BoE reserves, which has sparked concern as to whether a Labour government would use this to fund spending. Reverse tiering would reduce the interest paid on deposits placed at the central bank. Conversely, chancellor Hunt has noted that he is “not considering” the proposal, since it could impact the competitiveness of British banks.

We expect limited market impact

Overall, we expect the market impact of the UK general election on 4 July to be fairly muted with both parties firmly campaigning on the notion of delivering economic stability and the fiscal policy likely to remain constrained. In the regard, we deem the likelihood of another fiscal event akin to the “mini”-budget as unlikely. With the “mini”-budget still fresh in mind, this will also limit the possibility of the Labour party turning to unfunded spending, which historically has worried markets and trigged a subsequent rise in Gilt yields. However, closer ties to the EU, policies aimed at boosting growth and the supply side of the economy, less policy uncertainty are on balance GBP positive although we do not want to overstate the impact. For UK assets, we believe the cyclical backdrop, the global investment environment alongside the policy action from the BoE to prove more important for UK assets.

Given the UK's large current account deficit the GBP has historically been very sensitive to political uncertainty. However, this time around a Labour victory remains a clear base case for both markets and political pundits, which limits the potential for an uncertainty induced setback to GBP.

We do not believe the timing of the election will interfere with the BoE delivering the first 25bp cut in August. Alongside the recent topside surprise to inflation, the timing of the election further reduces the chance of an earlier move in June given the pre-election blackout period, limiting the BoE’s communication on policy action.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.