The fly in the ointment is falling yields

Outlook

We wrote yesterday Fed chief Powell was not likely to say anything different, and that was the right call. We have to wait for a tapering announcement for at least one more meeting and probably two, and then implementation of tapering at the second, third or fourth meeting after that. That takes us up to November or perhaps December. This is not a new narrative. Why was it not already priced into various markets? Well, it was–the dropping 10-year yield, the rising euro/dollar.

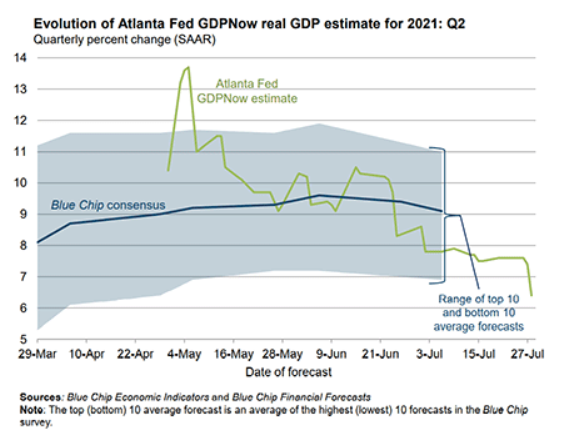

Today is another biggie, GDP. As we wrote before, estimates are all over the place. Today the WSJ offers its survey, 8.4% annualized, past pre-pandemic levels. Bloomberg has 8.5%, but we are dismayed to see the Atlanta Fed has a mere 6.4%, based on a drop in private investment. The Atlanta Fed almost always overshoots, so an undershoot is odd.

We also get the usual Thursday jobless claims, which is arguably more important because it’s the Fed’s main focus. Trading Economics has a succinct (if somewhat formal) report: “Initial jobless claims likely dropped last week to 380 thousand, not far from a 16-month low of 368 thousand reached at the end of June, underscoring a rapid recovery in the US economy. Still, the claims level is still more than double the pre-pandemic average, despite record job openings and stepped-up attempts by many businesses to add staff. The total number of claimants is likely to decline further in the coming weeks, due to the early phase-out of federal enhanced unemployment benefits across many states ahead of the official September expiration date, and as school reopen and demand over the summer picks up.”

What if GDP disappoints on the downside at the Atlanta Fed’s 6.4% (remember Morgan Stanley’s 11+%) but initial jobless claims crash well below the expected 350,00 or so? Logically, traders should price in an earlier tapering, which is dollar-favorable. Or how about the other way around, gigantic GDP at 10-12% but claims the same or higher? It’s hard to see this as not promising more jobs in the very near future, which we have been forecasting all along for Sept/Oct. Still dollar-favorable.

The fly in the ointment is falling yields, including the real yields, while inflation expectations are rising, deepening the negative real yield. We simply don’t understand how yields can be falling–meaning buyers abound–when GDP could be as high as 11%. Growth of that magnitude, even if a one-time bump, still suggests inflation from too much demand and too little supply. Even Powell said inflation can be bigger and more long-lasting than thought last time. So why are inflation expectations being dismissed in favor of a fear trade? Perhaps it’s fringe talk about a more lasting recession to come.

Then we have to consider it’s almost month-end and we need to expect position adjustments. That likely means paring long dollar positions, so may have contributed to the dollar’s decline. At a guess, the dollar is on a rough patch, but longer term (by which we mean Jackson Hole/September), sentiment will switch back to the US leading the world out of the pandemic-induced recession. Yields should recover, if not to any truly interesting real return. Yields falling so much is the single scary thing and not easily explained. Various efforts don’t really make a convincing argument. We note from time to time that yields and the dollar became mostly decoupled some years ago, but it appears the coupling is back. Perhaps China’s new soothing noises overnight will reduce anxiety.

Until anxiety (from whatever source) is cut back, we are stuck in a correction.

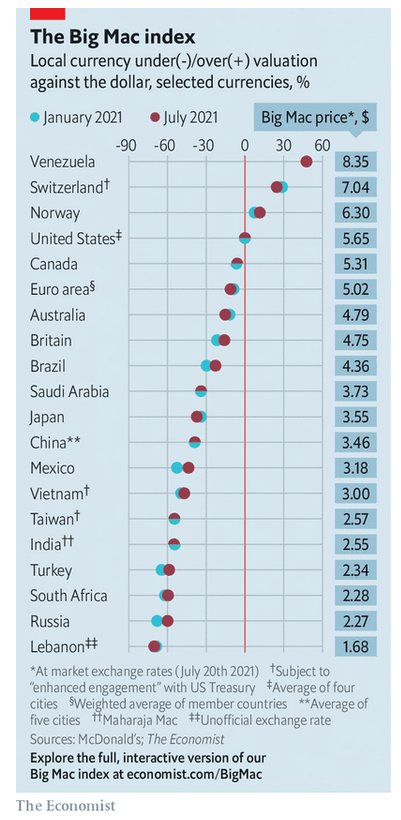

Fun Tidbit: Purchasing power parity theory holds that currencies should move to equilibrate prices across economies. It doesn’t work, of course, for about a dozen reasons, including selecting a representative basket of goods, difference in taste, and so on. But decades ago The Economist devised what it calls a “tongue-in-cheek” comparison of Big Mac prices around the world. It sometimes has some predictive value, too. The table this time shows the Swiss franc overvalued (it was ever so), the euro and pound somewhat undervalued, and the yen more undervalued. Just as the Treasury judged, the Vietnamese dong is undervalued, and the ruble even more so.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat