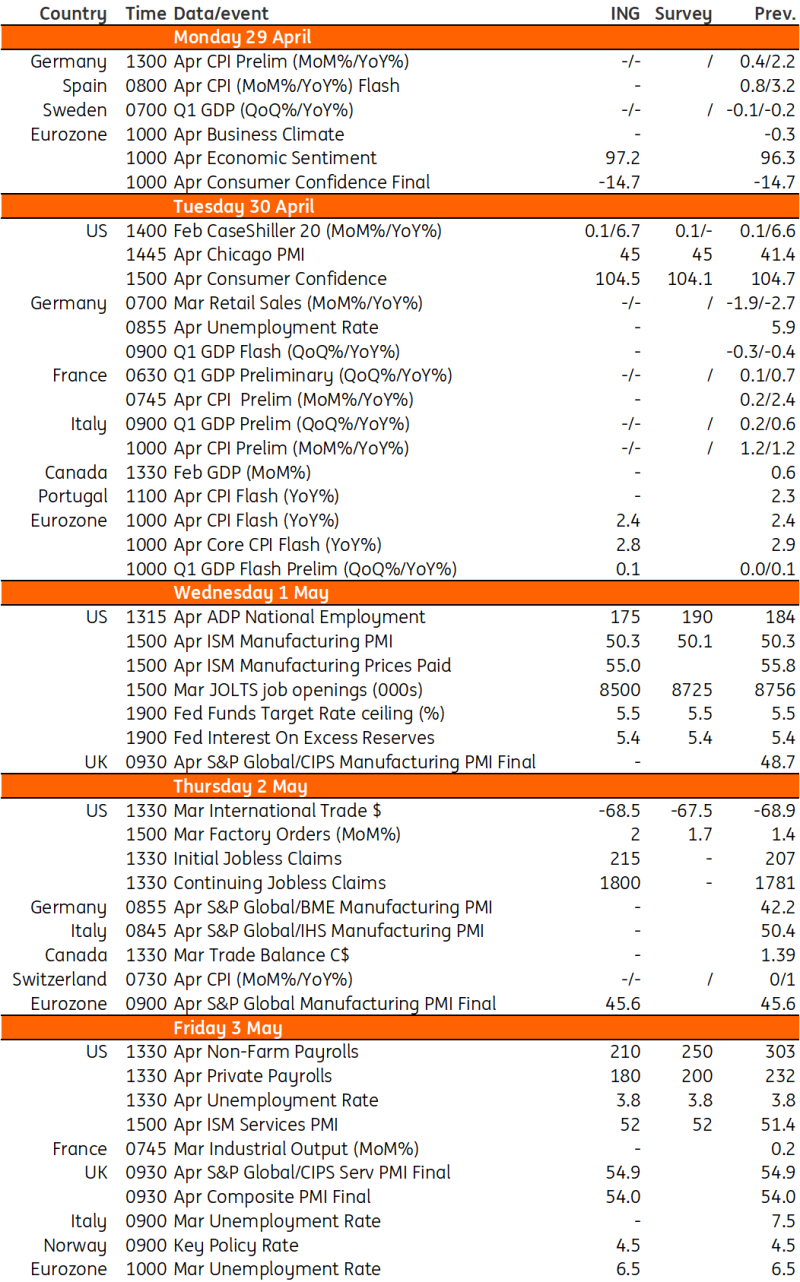

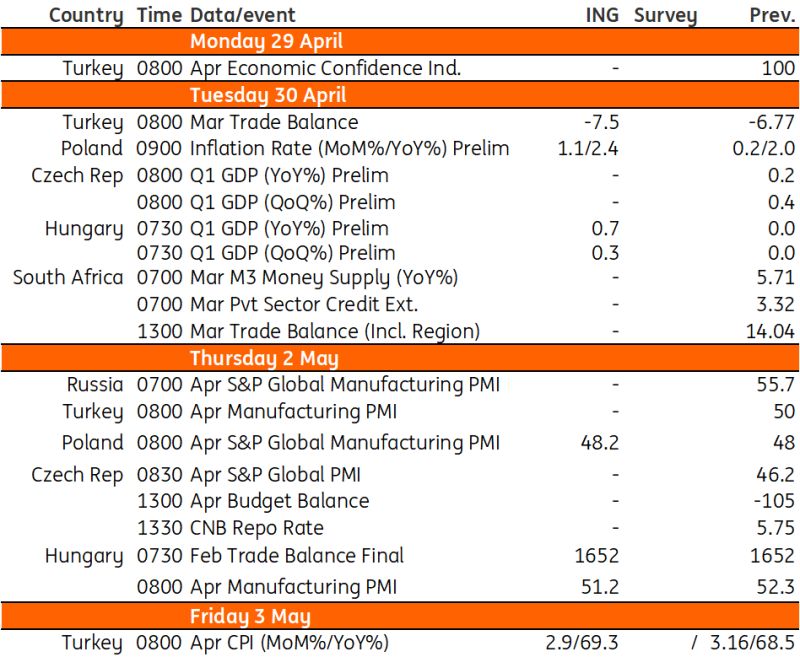

Key events in developed markets and EMEA next week

The highlight in markets next week will be the US jobs report. We expect a cooling to 210,00 jobs in April. Over in Poland, all eyes will be on CPI inflation where we expect a bounce back to 2.4%. Following a stagnant fourth quarter, we expect GDP growth to be positive in Hungary during the first quarter, while inflation in Turkey is forecast to rise to 69.3%.

US: Friday's jobs report the highlight

Markets have pushed the pricing for the first rate cut from the Federal Reserve back to December. This is a remarkable swing given it was only three months ago that the market was fully discounting 175bp of rate cuts this year starting at the March FOMC meeting. Nonetheless, with inflation running far too hot, the economy growing robustly and adding jobs in significant numbers there is no prospect of the Fed easing monetary policy in the near future with the upcoming 1 May FOMC meeting being a complete non-event. At the time of writing, the market is pricing just a 2.6% chance of a rate cut next week. The accompanying press conference will also see Fed Chair Jerome Powell sound less dovish with him set to reiterate his comments from 16 April that “if higher inflation does persist we can maintain the current level of restriction for as long as needed.”

In terms of the data, the highlight will be Friday’s jobs report. Having added 829,000 jobs in the first three months of the year the pace of hiring is expected to slow in the second quarter. Business surveys point to a substantial slowing, with the ISM employment components having sub-50 readings indicating a contraction and the NFIB small hiring survey suggesting something around the 50,000 mark. However, local government hiring is firm and there is a wariness that official data continues to be stronger than private sector surveys. Hence we look for non-farm payrolls to slow from 303,000 in March to 210,000 in April and for the unemployment rate to remain at 3.8%. Nonetheless, we will get ADP employment numbers and other survey updates that will help firm up expectations through the week.

Other numbers to look out for include the ISM manufacturing and service sector purchasing managers’ indices. They are currently at levels historically consistent with GDP growth closer to 0.5% year-on-year rather than the 3% YoY reported by 1Q GDP. We aren’t expecting any meaningful improvement next week. Also, watch out for the 1Q employment cost index for signs that inflation pressures emanating from the jobs markets continue to cool.

Poland: CPI inflation to bounce back to 2.4% in April

Flash CPI (Apr): 2.4 % YoY

We forecast that CPI inflation bounced back slightly in April (2.4% YoY vs. 2.0% YoY in March) and was close to the National Bank of Poland's target of 2.5% (+/- 1pp). Core inflation excluding food and energy prices moderated to 4.0% YoY from 4.6% YoY. House energy and fuel prices were still slightly cheaper than in April 2023. The main driver of higher CPI inflation is an upswing in food prices. Although wholesale prices did not increase markedly, the VAT on food was restored in April. In an environment of price wars among large retail chains, the higher tax was not fully passed onto the consumer, but still, food prices increased markedly in monthly terms, after two months of declines.

Hungary: Positive growth expected in the first quarter

Next week's key data point will be the (preliminary) first quarter GDP print in Hungary. There is a high degree of uncertainty surrounding the performance of the agriculture and services sectors, as there is (usually) a lack of high-frequency data on these sectors. On the other hand, based on last year's performance, we expect agriculture to make a negative contribution to GDP growth, while we expect some recovery in services due to rising household purchasing power. Otherwise, we see industry more or less stagnating, coupled with a surprisingly strong first quarter in construction due to technical factors. All in all, we see the Hungarian economy moving from stagnation to positive growth in 1Q, both on a quarterly and annual basis. As for the second quarter, the first indicator will be the fresh manufacturing PMI print, where we forecast an expansionary reading, albeit lower than in March

Turkey: Annual inflation to rise to 69.3%

Given the worsening in price dynamics, as evidenced by the elevated trend inflation and high exchange rate pass-through in addition to the sensitivity of forward-looking expectations to past inflation, we expect the annual figure to rise to 69.3% in April (with a 2.9% MoM reading) vs 68.5% a month ago. Going forward, whether the central bank's unexpected and strong rate hike, large set of macro-prudential measures, and liquidity tightening will be enough to return inflation to its forecast range will be closely followed by the market.

Key events in developed markets next week

Source: Refinitiv, ING

Key events in EMEA next week

Source: Refinitiv, ING

Read the original analysis: Key events in developed markets and EMEA next week

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.