The final leg of the USD rally

At Thursday's meeting, the ECB kept all policy rates unchanged, maintained its monthly QE purchases of EUR 80bn and did not change its intention to end purchases in March 2017. At the press conference, Mario Draghi initially said that the Governing Council had not discussed an extension of QE but also said that they had not discussed a tapering of QE either. We still believe that the ECB at its December meeting will announce an extension of its current QE programme to September 2017.

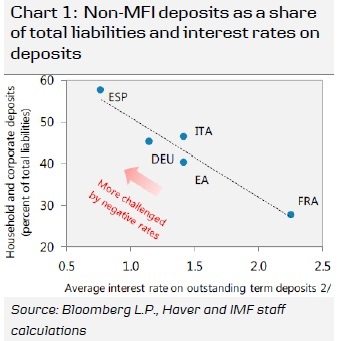

Recent research has shown that banking systems with a) a high share of variables rate loans, b) a large deposit base compared to total funding; and c) a small share of fee income will suffer under a negative rate environment. Italy, Portugal and Spain all have a high share of variable loans while Spain in particular has a large share of deposits compared to total liabilities (see Chart 1). In addition, the direct costs of negative deposit rates are likely to be greater for banks in large surplus countries such as the Netherlands and Germany where the Target 2 settlement of capital flows generates large amounts of excess liquidity in their banking systems. It is likely that the ECB in particular will be concerned about the relatively short end of the yield curve, which has the largest transmission to banks' deposit and lending rates. This rules out further ECB interest rate cuts whereas an extension of the QE programme should be less damaging for banks.

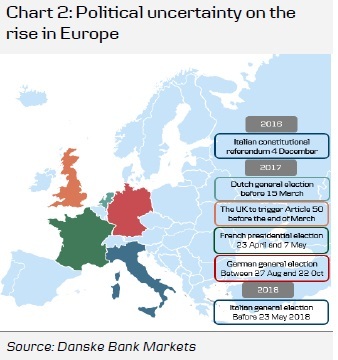

From our discussions with clients, it is clear that everyone is very concerned about politics in Europe. In our view, Brexit negotiations will set the tone for EU politics. Based on recent comments it is likely that both the EU and the UK will begin Brexit negotiations from a ‘hard Brexit' starting point. The EU will have to signal a tough stance to ensure that other countries are not tempted to follow the UK. Meanwhile, it appears that the UK government wants to have a say in controlling immigration. However, it will be a ‘game of chicken' where the UK may blink first as it is not obvious from polls that the UK population wants to controlimmigration rather than having full access to the single market. The EU's stance during the negotiations will of course be highly dependent on the outcomes of upcoming referendums and elections (see Chart 2).

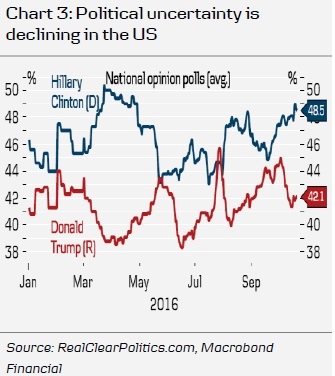

The political risks and relative monetary policy will weigh on EUR/USD where yesterday's downside break of 1.0950 opens the door for further losses towards 1.0700-1.0850. Positioning is not yet stretched short EUR/USD, which supports a greater role for relative rates. We see political risks in Europe as more EUR negative than USD negative as Clinton appears to be the likely winner of the US election. (Chart 3). We expect it to be sell-therumour, buy-the-fact with the EUR/USD bottoming in December and heading convincingly higher in 2017 on the large Eurozone-US current account differential and valuation. We also note the continuing rise in USD/CNY (and USD/CNH). This is in line with our view and we expect it to continue to head higher into year-end on broad USD strength and China's need for a weaker exchange rate.

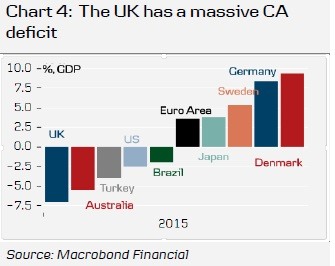

Finally, on FX the British pound (GBP) has plunged. The UK runs one of the largest current account (CA) deficits and the funding of that will be pressured if the UK opts out of the single market (see Chart 4). Still, markets may to a significant extent already be priced for a hard Brexit. We believe the British pound will weaken further against both the USD and the EUR, but that will play out over the coming 3-6 months. It will be ‘sell the rumour, buy the fact' with respect to the UK's triggering of article 50 and the GBP is likely to strengthen later in 2017.

As we argued a couple of weeks ago, we believe that there is a macro-case for higher longend bund yields given higher inflation and inflation expectations in Europe and that the market is likely to price in ECB tapering long before it occurs. However, timing is difficult and our view is more of a 6-12 months view rather than a short-term view. Short term, we see equities as a ‘buy-on-dips' after a reasonable start to the earnings season in the US, while we remain underweight on equities versus cash on a 3-6 month view as earnings expectations in 2017 look unrealistic.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.