The Dollar as a global reserve currency, is it the end?

The Dollar is in a weird place. On the one hand, the US is arguably the strongest economy in the world with its currency being used as the global reserve (essentially guaranteeing a bailout in case of an economic disaster). On the other, the US has legitimate competition for the first time since the Second World War in the form of China, and the trade war, combined with excessive debt burden may finally be beginning to take its toll.

Keeping everything in mind, we will take a long-term view of the dollar. We will analyze every single major aspect of the currency and attempt to determine whether it will rise or fall in the next few years.

Why the Dollar’s Strength Matters

Before we take a look at the future of the dollar, it is important to understand why the power of the Dollar is important. A stronger currency means imports are cheaper and exports are expensive. It is for this very reason that China devalued the yuan in 2019.

Furthermore, investors investing in the US Dollar would decrease their real returns if the dollar has weakened in between when they invested and when they cashed out (this also applies the other way around). As such, foreign investments may be a better idea if you are bearish on the dollar.

Overall, there are both positives as well as negatives whenever there is a change in the power of a currency. It is up to you to determine which one of these moves is better from your portfolio’s point of view.

The Dollar as a Global Reserve Currency

At the beginning of the last century, Britain was considered the center of world commerce. The US, while it had the largest economy roughly by 1910, it did not have an official currency. In 1913, the Federal Reserve Bank came into existence (FED). Just a few decades later, it was the world’s reserve currency.

The dollar went from strength to strength as the vast majority of the global powerhouses recovered from the first World War. At that time, the Gold Standard was in use. The Gold Standard had both positives as well as negatives. While there were many proponents for it, there were also several problems with the system.

During the second world war, the US lent a lot of money to Allied nations. In 1944, 44 nations met at Bretton Woods in New Hampshire, and decided that their currencies will be linked to the US Dollar, and the Dollar will be linked to gold.

The dollar is no longer pegged to gold, but it is still the world’s reserve currency. Over 60% of the foreign bank reserves are currently held in US Dollars. However, that number is on the decline, with Russia and China looking towards a system that serves their interests in a better way. Before we explore that, let’s look at what the US Dollar has going for it!

Reasons Behind the Strength of The Dollar

Here is why the Dollar could still be strong in the years to come.

The Aftermath of the Stock Market Crash

It is possible for the stock market to affect the exchange rate of a currency in a significant way. To put it simply, a falling market encourages money out of the country, while a rising one invites it in. It seems that the worst of the 2020 COVID-19 crash is beyond us, and markets are gradually recovering.

Keeping this in mind, it is likely that foreign investors entering the US market will pressure the currency upwards.

A Recovering Economy

The bi-partisan stimulus package that provides over $2 trillion to US citizens and Businesses will have both positive as well as negative effects. One of the positive effects is the fact that normal business activity will resume much quicker. Considering the fact that the US has a stimulus package that is larger than any nation on Earth, it is probable that the US will recover in a much quicker fashion.

This will automatically give the US an edge. With competitors reeling from the crisis, this might be the best time for manufacturers to export goods to countries with poorer infrastructure, thus increasing the demand for the dollar on the exchange.

Debt and the Emerging Markets

On a related note, once the US economy begins to gain traction, it is probable that the interest rates will rise. The Fed had already planned to stop its bond purchasing program in 2019. However, we saw the FED once again purchase treasury securities during the COVID-19 crisis.

While this will continue for some time, the FED will eventually return to its policy of ending the balance sheet runoff. When that happens, the volatility in interest rates could have an astoundingly positive effect on the US Dollar due to debt in the emerging markets.

Right now, a large number of US citizens and businesses are invested in numerous emerging markets such as Brazil, India, and Turkey. These markets depend on a low-interest rate as they run a Current/Fiscal deficit and they need foreign inflows to fund it.

Conditions in emerging markets were already worsening towards the end of the last decade. The havoc that COVID-19 has wreaked definitely won’t be of much help.

If the interest rates in the US become more favorable, they will affect the debt in two ways. First, it will further hamper investor confidence in emerging markets as their debt payments will be much larger. Secondly, we might see large capital inflows back into the country from such markets as the returns in the US become more favorable. This will definitely have a big hand in pressuring the dollar upwards.

Reasons Why the Dollar May Fall

All is not well when it comes to the dollar. Just like there are a lot of reasons due to which it could rise, there are also many that could cause it to fall. Let’s take a look at some of the major ones.

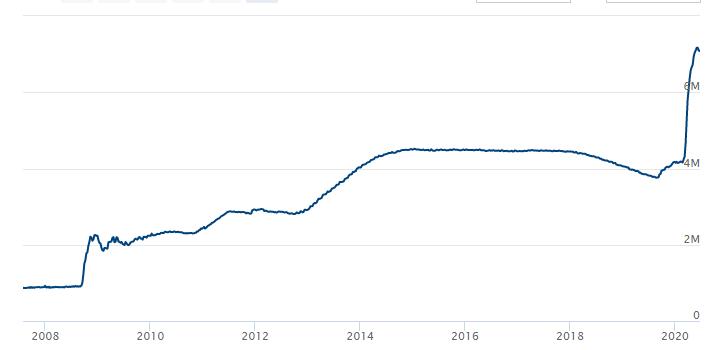

Excessive Money Printing from the FED

We mentioned the stimulus package earlier. While it may help boost the recovery, the money also had to come from somewhere. The US has long been under heavy debt. In fact, the US is the most indebted country in the world.

The debt has been used to fund wars, provide stimulus after the 2008 financial crisis, and fund other initiatives that the government has undertaken.

It is quite obvious that when the government prints more money than usual, then the value of the currency falls. This is because there is more money going after the same things, virtually increasing its demand.

Printing money also leads to inflation. Inflation is almost always bad for any currency since it decreases its purchasing power. Inflation has been low in the US in the past few years, but it is possible for it to rise quickly due to the amount of printing that is currently occurring.

Here's the FED balance sheet - pay attention to the change in the last 3 months:

The Trade War

The trade war has already cost the US in a massive way, and it doesn’t seem like it will stop any time soon. According to estimates, the trade war impacted more than $460 Billion of goods in 2019, and it increased consumer costs by $57 Billion.

A trade war may help reduce imports into the US, but it will similarly reduce US exports to China. Overall, a trade war decreases economic activity in all countries involved. In the case of the US and China, the ramifications could extend to the rest of the world due to the size and superiority of them both. A perfect example of this is the trade war that took place in the Great Depression, which decreased world trade by 25%.

To add to that, a trade war can also cause a lot of speculation in the markets. This has been evident with both the stock as well as the forex markets swaying wildly with every single piece of news or announcement from both camps. This can cause markets to be volatile in the short-term, causing investors to move to safer assets.

Efforts to Change the Global Reserve Currency

There have been efforts by numerous countries (led by China and Russia) to dethrone the US Dollar as the world’s reserve currency. China has been reducing its exposure to the Dollar for a long time, and both China, as well as Russia, have been stocking up on gold in recent times.

Other countries are beginning to join the fray. Turkey, India, and Iran have begun to do a small amount of trading in other currencies. In early 2020, Pakistan joined China and Russia and decided to trade in local currencies as well.

Pakistan and China have an ironclad trading agreement between themselves in the form of CPEC. This trade agreement is quite fitting for the current economic situation, as Pakistan is a country that has heavily relied on US aid in the past, but it seems to gravitate more and more towards China with each passing day.

Conclusion

Overall, it seems as if the tide is finally starting to turn against the US Dollar. Not only does the US face immense challenges in the short-term in regards to potential inflation and the trade war, but it is also possible for its currency to lose its status as the global reserve.

If that happens, the confidence in the US Dollar would shrink by such a gargantuan amount due to their debt and their economic policy that it is quite possible for the Dollar to plunge to unprecedented amounts.

Do remember that the chances of the latter happening are incredibly slim. The vast majority of the world still has no plans to switch from the US Dollar, and the government has persevered through far worse times (e.g. the Great Depression and the 2008 crisis). Still, it is hard to recommend being bullish on the Dollar in its current state. The enormity of the challenges should cause conservative investors to prioritize other currencies, and that is what we recommend as well!

Author

Baruch Silvermann

The Smart Investor

Baruch Silvermann is a personal finance expert, investor for more than 15 years, digital marketer and founder of The Smart Investor.