The danger of debt becoming more expensive as GDP drops for emerging markets

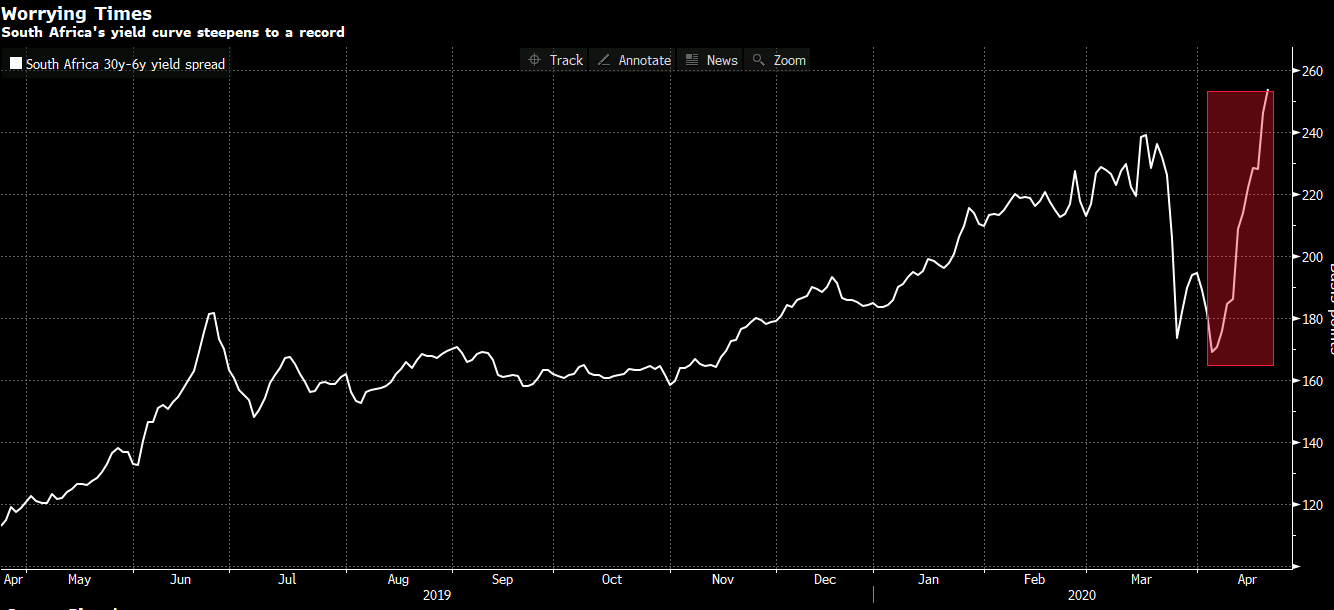

South Africa's debt financing is becoming more expensive

It is an obvious problem. When income is high enough we can finance debt. However, when times are hard not only does income drop, but debt also becomes more expensive. Repayments go up because you are now a riskier borrower. It is the double edged sword of debt that can get you in big trouble.

The book 'And the money kept rolling in (and out)' really outlines so clearly the problem that emerging markets have in trying to break free of this debt/bust cycle. If you want to see how the World Bank, IMF and Wall Street work together to 'support' emerging markets then read this book. It will also really underscore how bonds can work to really create an uphill struggle for emerging markets when bond yields rise and make borrowing more riskier as well as attracting predatory investors keen to capitalise on a country's weakness.

South Africa is potentially facing a similar problem to Argentina. The yield curve is steepening as South Africa embarks on a $26 billion plan to support the economy.

The funding for that plan is due to come from reallocations within the budget, loan guarantees to banks, the World Bank, the IMF as well as other domestic and international lenders. All well and good to take the loans when times are good. However, the forecast is for a -6.1% contraction this year which will leave a large tax revenue shortfall. This will mean that Government debt could climb to 80% of GDP from around 62%. The problem comes that a vicious spiral can quickly emerge: Falling income, leads to greater borrowing, leads to higher bond yields, leads to steeper repayments. Eventually the bubble bursts and the cards come falling down. Sadly, a number of emerging markets are going to be experiencing this problem going forward. This is one area to watch for SA and hopefully the selective default that Argentina implemented won't be repeated.

Author

Giles Coghlan LLB, Lth, MA

Financial Source

Giles is the chief market analyst for Financial Source. His goal is to help you find simple, high-conviction fundamental trade opportunities. He has regular media presentations being featured in National and International Press.