The Case For Stagflation: US composite PMI shows wage pressures persist

With price pressures stabilizing and wages pressures still rising, let's discuss the stagflation case.

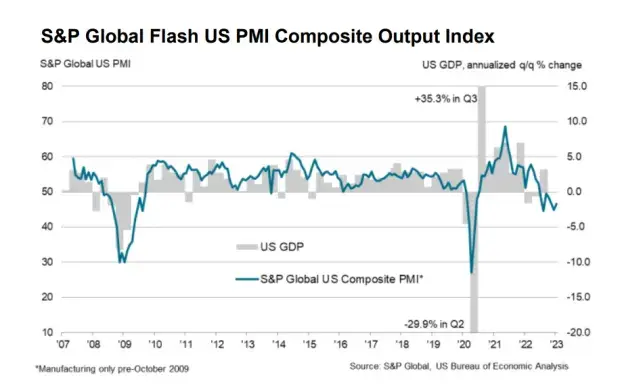

The S&P Global Flash US Composite PMI™ shows Private sector contraction in the US continues into the new year, with renewed pick up in cost pressures.

Key Findings

- Flash US PMI Composite Output Index at 46.6 (December: 45.0). 3-month high.

- Flash US Services Business Activity Index at 46.6 (December: 44.7). 3-month high.

- Flash US Manufacturing Output Index at 46.7 (December: 46.2). 2-month high.

- Flash US Manufacturing PMI at 46.8 (December: 46.2). 2-month high.

The headline Flash US PMI Composite Output Index registered 46.6 in January, up from 45.0 at the end of 2022. The contraction in activity was solid overall, but the slowest since last October.

Bringing to an end a seven-month sequence of moderating input price rises, January data indicated a faster increase in cost burdens at private sector firms. Although well below the average rise seen over the prior two years, the rate of cost inflation quickened from December and was historically elevated. Hikes in vendor prices, alongside higher wage bills, reportedly spurred the sharper rise in costs.

Despite subdued demand conditions and a further solid decrease in backlogs of work, US firms recorded a marginal rise in employment at the start of 2023. The rate of job creation was one of the softest in the current sequence of employment growth that began in July 2020.

Comments by Chris Williamson, S&P Chief Business Economist

- “The US economy has started 2023 on a disappointingly soft note, with business activity contracting sharply again in January. Although moderating compared to December, the rate of decline is among the steepest seen since the global financial crisis, reflecting falling activity across both manufacturing and services.”

- “Jobs growth has also cooled, with January seeing a far weaker increase in payroll numbers than evident throughout much of last year, reflecting a hesitancy to expand capacity in the face of uncertain trading conditions in the months ahead. Although the survey saw a moderation in the rate of order book losses and an encouraging upturn in business sentiment, the overall level of confidence remains subdued by historical standards. Companies cite concerns over the ongoing impact of high prices and rising interest rates, as well as lingering worries over supply and labor shortages.”

- “The worry is that, not only has the survey indicated a downturn in economic activity at the start of the year, but the rate of input cost inflation has accelerated into the new year, linked in part to upward wage pressures, which could encourage a further aggressive tightening of Fed policy despite rising recession risks.”

Case for Stagflation

The third bullet point above, emphasis mine, is the case for stagflation.

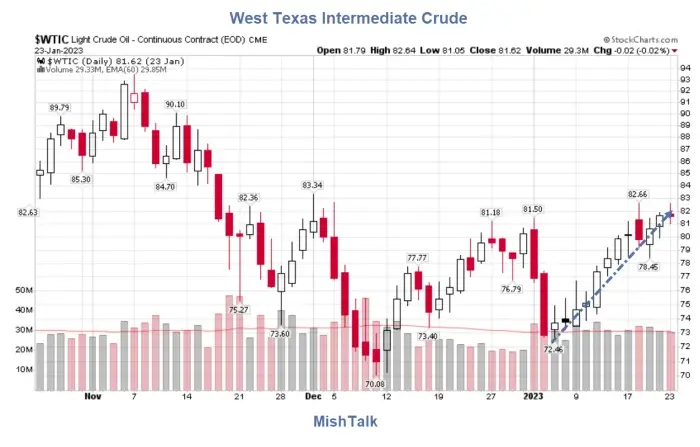

Oil isn't helping any.

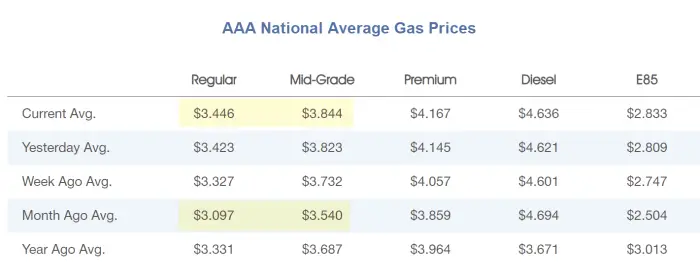

AAA National Average Gas Prices

CPI Declines Due to Gasoline But Food and Shelter Costs Jump Again

Key Details Month-Over-Month

- The Consumer Price Index for All Urban Consumers (CPI-U) declined 0.1 percent in December on a seasonally adjusted basis, after increasing 0.1 percent in November.

- The index for gasoline declined 9.5 percent and was by far the largest contributor to the monthly all items decrease.

- The energy index decreased 4.5 percent over the month.

- The the fuel oil index was down 16.5 percent but energy services including electricity and piped natural gas rose 1.0 percent and 3.0 percent respectively.

- The food index increased 0.3 percent over the month with the food at home index rising 0.2 percent.

- The shelter index rose 0.8 percent.

Gasoline is highly unlikely to save the day again.

However, it's possible the gasoline increase in January will be modest because December had some pretty wild swings in the price of crude.

For the CPI to decline again would take food and shelter prices falling with gasoline up no more than a bit.

Don't count on it. And if not, expect another barrage of Fed comments on hiking more for longer.

Not to worry, ultimately the Fed will crush demand enough that prices will stop rising. But think about what that will mean for stock market earnings.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc