Tail risks emerging

S&P 500 continued higher Friday as consumer confidence data didn‘t disappoint – adding to soft landing hopes. Soft landing would though only happen should the unemployment claims don‘t rise too much – on the flip side, that would mean that service inflation would remain high, which is exactly what we have seen so far. It‘s a double edged sword, this tight job market – and it will remain tight. Just have a look at unemployment ratio to job openings – it‘s not really declining, and the Fed wants to see it decline, just like latest job creation is more than double the Fed‘s preferred less that 100K monthly.

So when would the troubles strike, based on what the Fed is doing? I look for continued balance sheet shrinking, and while the hikes favor 25bp for Jan FOMC, it‘s far from a done deal. 50bp is still very much an option (underappreciated by the markets), but I acknowledge it‘s slightly less probable than 25bp. Anyway, it takes up to 12 months for rate hike effects to play out in the economy, and we have seen one of the steepest hiking paths last year – one that can be compared to mid 1990s (the last time of a soft landing, by the way).

Followed by 25bp more in Mar, we would have Fed funds rate at 5%, but Kashkari wants to go higher, almost to 5.50% - and should headline and especially core inflation remain sticky (these won‘t please the Fed in the months ahead), the central bank would seek to redefine its level of restrictive FFR regardless of the 2y yield telling the Fed for weeks it‘s done tightening, otherwise things in the real economy start to break.

Forget for a moment about Japanese yields rising, third day in a row above the 0.50% threshold the BoJ deems permissible. Appreciating JPY as the yen carry trade is unwound, which is resulting in rising Treasury yields (parking the money in risk-free U.S. government bonds was the go-to proposition of those borrowing in yen). Brings in mind the Swiss frank peg, and we know how that ended.

And indeed thing are all on a solid track of breaking – let‘s isolate earnings and the pace of recent surprises. If these continue as before, we are looking at a neutral or negative earnings growth quarter, but greater troubles would strike in Q2 earnings season, because the Fed in my view wouldn‘t be able to avoid doing no more rate hikes, and I am not even bringing up the market hopes of two rate cuts late 2023 that the Fed is adamantly ruling out, and I agree as it in my view wouldn‘t cut.

It‘s aware that inflation has to be defeated, and inflation expectation must return lower – including household ones, and by extension nominal wage growth. After having cut the temps and overtime hours, things will get serious in the job market, with quickening pace of layoffs once the unemployment rate increases over 4%. Not even poor manufacturing, services or real estate data would convince the Fed.

As for the recent bank earnings (more to come this week, together with $PG and $AA), see rising loan loss reserves. Couples nicely with tightened bank lending standards. Add the soon to be 10 months in a row of negative LEIs, and the two yield curve inversions (levels unseen in decades)– and you can bet your bottom dollar on recession arriving around mid year, which is when the going would get considerably rougher.

We ain‘t seen nothing yet. If in doubt, check shipping rates - $BDI below Aug lows while U.S. domestic transport remains more resilient – the troubles haven‘t yet hit the shores, but are amply seen in leading indicators.

Keep enjoying the lively Twitter feed serving you all already in, which comes on top of getting the key daily analytics right into your mailbox. Plenty gets addressed there (or on Telegram if you prefer), but the analyses (whether short or long format, depending on market action) over email are the bedrock. So, make sure you‘re signed up for the free newsletter and that you have my Twitter profile open with notifications on so as not to miss a thing, and to benefit from extra intraday calls.

Let‘s move right into the charts.

S&P 500 and Nasdaq outlook

S&P 500 is likely to spend more time around the 200-d moving average. 3,980 is first support, followed by 3,955. Conversely 4,010 and 4,040 await on the upside as the tug of war is going on. The timing of USD relief rally will though tip the scales one way...

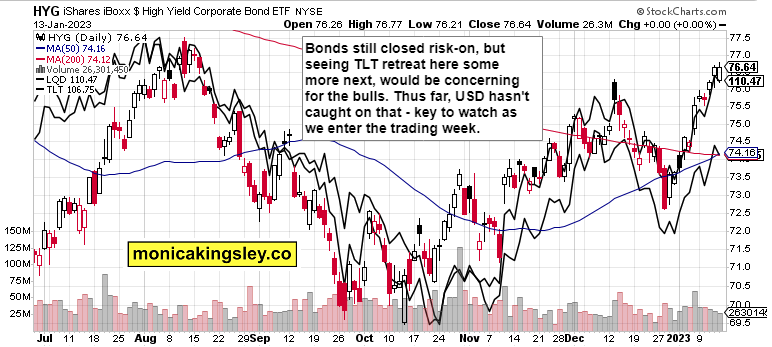

Credit markets

Bonds look to be in need of a breather, but aren‘t done retreating. The jitters are understandable given the BoJ uncertainty – won‘t it disappoint in setting the new 10-y permissible rate? The risks are skewed towards risk-off, broadly speaking.

Copper

Copper is worth watching here for general risk-on sentiment – the red metal would (and should) stumble without recovering into $4.15 on troubles hitting and spreading to other assets in the very short run.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.