Surging commodity prices adds to emerging market vulnerabilities

-

Rising fuel and metal prices leave importers exposed at a time when slow progress in COVID-19 vaccinations threatens to derail economic recovery and looming US rate hikes highlight external vulnerabilities.

-

Most EM countries in Europe, Asia and Latin America are hurt by higher fuel prices. Turkey, India and Egypt are particularly vulnerable as their external positions are weak to begin with.

-

In longer term, the global transition to clean energy technologies will benefit net metal exporters, also further boosting China’s prominence in the global economy.

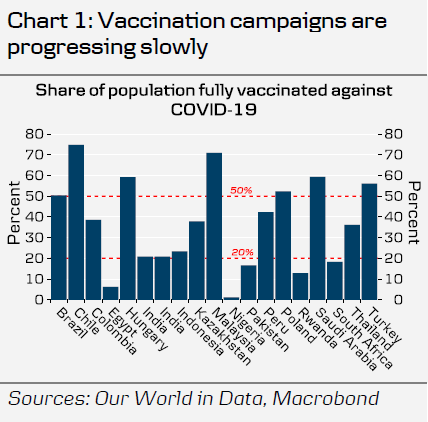

High fuel and metal prices pose another risk to EM outlook

Rising energy and metal prices are a double-edged sword for emerging markets. While net exporters welcome the booming prices, net importers face a rising imports bill. For many economies, rising import costs will further undermine their already weak external position. Acute energy shortages could also lead to electricity rationing and power cuts locally, derailing fragile economic recovery. The energy crisis hits the EM at a time when slow progress in COVID-19 vaccinations is leaving many countries exposed to further negative impacts from the pandemic (See Chart 1). In the context of rate hikes approaching in the US next year and anticipated USD strength, there is a risk of abrupt reversals in net capital flows, adding pressure on EM currencies and debt.

Prices expected to level off, but risks are tilted to the upside

In our baseline, we see oil prices in the range of USD 75-80 for the next two years. OPEC has shown little signs of easing the current tight supply, but if prices continue materially higher from here, a combination of both a response from OPEC and our view of stronger USD should limit the rise over medium term. On the other hand, downside is limited due to low investments into production over the past years. For natural gas, the combination of low supply from Russia, limited availability of LNG globally and low renewables production in Europe is likely to keep the prices elevated through winter’s heating season, as we wrote in Research Euro Area - Looming energy crisis creates a perfect storm, 4 October.

For metals, the fading growth in China combined with high costs of energy-intensive steel production have already weighed on iron ore producers’ terms-of-trade, including Brazil and South Africa. High energy costs continue to contribute to tight refined metals supply for now, but ultimately the Chinese construction sector downturn, increased focus on environmental challenges and deleveraging imply at least moderately lower metal prices over medium term, read more in Research Global - Power crunch supports metal prices despite fading demand, 18 October.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.