Euro area: Looming energy crisis creates a perfect storm

Energy prices have risen globally, and while the base case remains for prices to reverse lower in 2022, risks of more persistent effects on euro area growth and inflation remain.

The gas price surge has been a result of recovering industrial demand, high demand for heating and cooling, and limited supply of gas and renewable energy.

Elevated energy prices combined with cost-push inflation from ongoing global supply issues pose challenges for manufacturing and real disposable income, which European governments have already tried to soften. Nevertheless, timing is unfortunate as the post-pandemic recovery is still vulnerable to setbacks.

Severe gas shock expected to last through winter

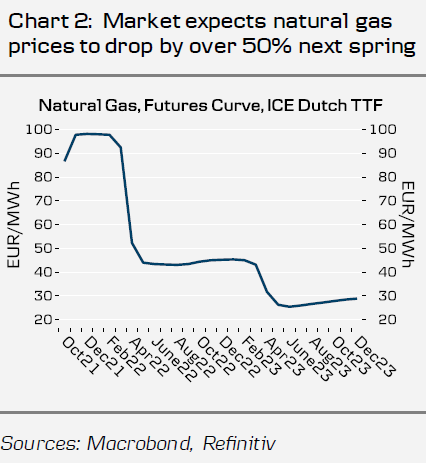

As European gas futures hit 100EUR/MWH, market concerns of a looming energy crisis in Europe have risen. The rapid rise in European natural gas prices has been a result of a combination of factors. Demand has been driven up by both the very cold winter and the subsequent hot summer, which boosted households’ heating and cooling needs. The reduced production of nuclear power has increased the relative importance of fossil fuels and renewable energy. The hot summer, however, also reduced electricity supply from both Northern European hydropower plants (Chart 1), as well as wind power.

The lack of alternative energy sources has increased demand for fossil fuels, and especially natural gas, and inventory levels have fallen below normal levels ahead of the high-demand heating season. The development can also be seen as a part of the more long-term European green transition challenge, where rising CO2 prices encourage a shift towards renewables, yet the limited capacity leaves gas as a ‘go-to’ solution for more polluting fossil fuels.

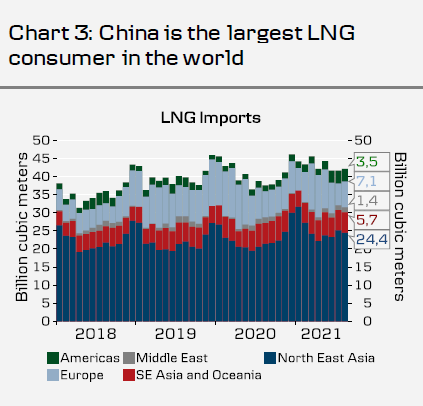

The rise in energy demand is not Europe-specific, however. Cold weather and the postpandemic recovery in industrial activity have increased demand also in Asia, which has already led to energy rationing in many Chinese provinces. From European perspective, this limits the global LNG supply, which could theoretically be shipped to Europe, as large share of the supply has already been tied to Asia with long contracts (Chart 3).

Market expects prices to moderate towards spring

Gas futures markets expect prices to remain high through the winter, before falling next spring (Chart 2). This largely reflects the cyclical nature of energy demand, and also highlights the uncertainty over the winter, as the upcoming weather is both important for prices yet highly unpredictable. We are now past the peak in the global recovery pace and approaching both fiscal and monetary tightening over the coming year. Moderating industrial growth should also limit upside in energy demand.

Yet, the rise in prices hits at an inopportune time, as the post-pandemic recovery is still vulnerable to setbacks. The higher prices come on top of the still ongoing global supply shortages, which continue to increase prices of inputs and raw material, and the power rationing in China could further delay easing of the situation. Labor shortages continue to put upward pressure on wages especially in the US, but also in other parts of the world as we highlighted in Research Global - Stagflation' risks on the rise, 15 September.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.