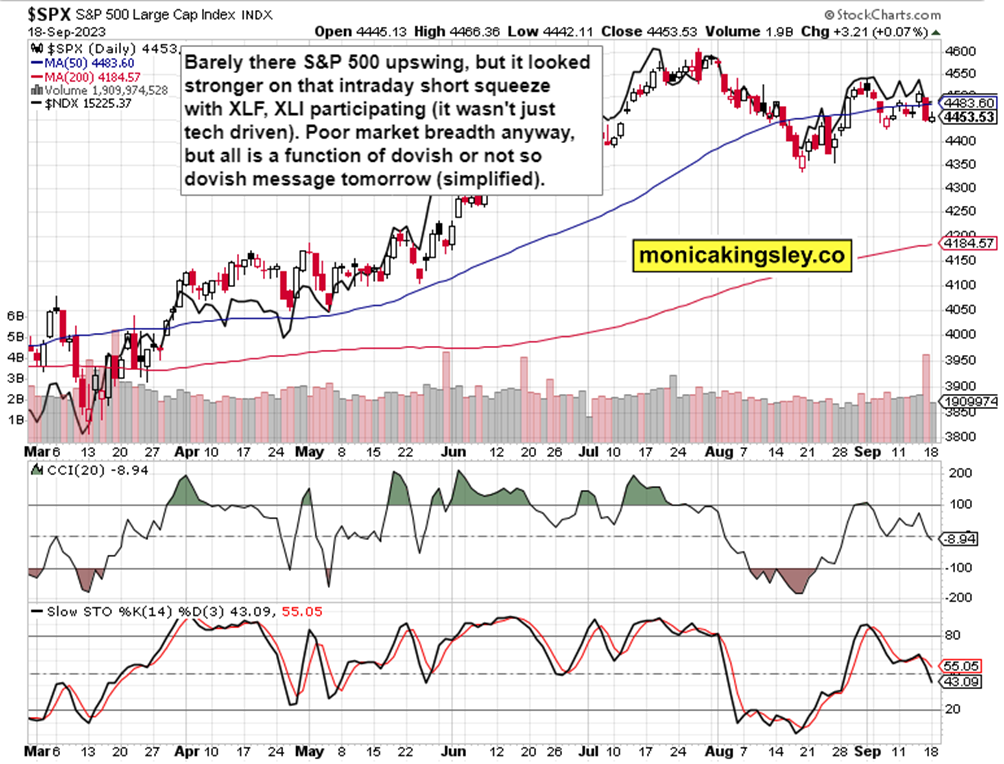

Smelling FOMC outcome

S&P 500 made a dead cat bounce mixed with an intraday short squeeze, and given likely rise in yields (10y back above 4.33%) and muted HYG, I favor a slow decline to prevail today. Not that FOMC positioning would need to be overly bearish, but odds are yesterday‘s advance-decline line or volume status is likely to catch up with stocks some more today, especially given my immediate take on housing preceded by an Intraday Signals ES call. If it weren‘t to, we would have seen a much better European session showing, which isn‘t clearly the case with DAX slightly negative, and more.

Hence, it‘s up to the early Friday confirmed turn in gold, and continued consolidation with a bullish medium-term bias in oil, that remain the easiest trades, together with a patient ES, NDX short waiting for more downside later in Sep and beginning Oct (seasonal tendencies supported e.g. by the turn in global liquidity, however modest).

Let‘s move right into the charts – today‘s full scale article contains 3 of them.

S&P 500 and Nasdaq outlook

4,515 stopped the advance yesterday (my first resistance support given in premium analysis yesterday) while I didn‘t take the possibility of a run to 4,532 second level resistance seriously. Reconsidering following yesterday‘s rejection at 4,489 (probably this is the level on the way down, and not 4,492 or 4,485 anymore), this area will be more than nibbed at during today‘s session, which of course requires HYG below $74.62 and 10y yield above 4.34%. The journey to the next support – 4,465 – is still long, and the Fed‘s not really hawkish stance tomorrow is likely to result in a reflexive stock market upswing first (without changing bearish rationale down the road).

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.