Seven fundamentals for the week: Two rate cuts, Nonfarm Payrolls to jolt markets in a packed week

- June kicks off with a packed economic calendar, promising high volatility in markets.

- The ECB and the BoC are widely expected to cut interest rates.

- A long buildup to Nonfarm Payrolls includes the JOLTs report, which could steal the show.

May's end-of-month flows were wild but directionless – and the first week of June is packed of top-tier events that may shape trends for weeks. Forward-looking surveys, guidance about the next moves from central banks and all-important US job figures are all on the docket.

Here are the main events to watch out for.

1) ISM Manufacturing PMI may show a retreat in inflation

Monday, 14:00 GMT. Despite massive manufacturing and construction spending, the industrial sector seems cautious. The Institute for Supply Management’s (ISM) Manufacturing Purchasing Managers Index (PMI) reached 49.2 in April, signaling a mild contraction. Economists expect a similar outcome now – but a key component could steal the show.

Update: ISM Manufacturing PMI came out at 48.7, worse than expected, and the Prices Paid component slipped to 57, also short of estimates. The US Dollar retreated across the board in the aftermath.

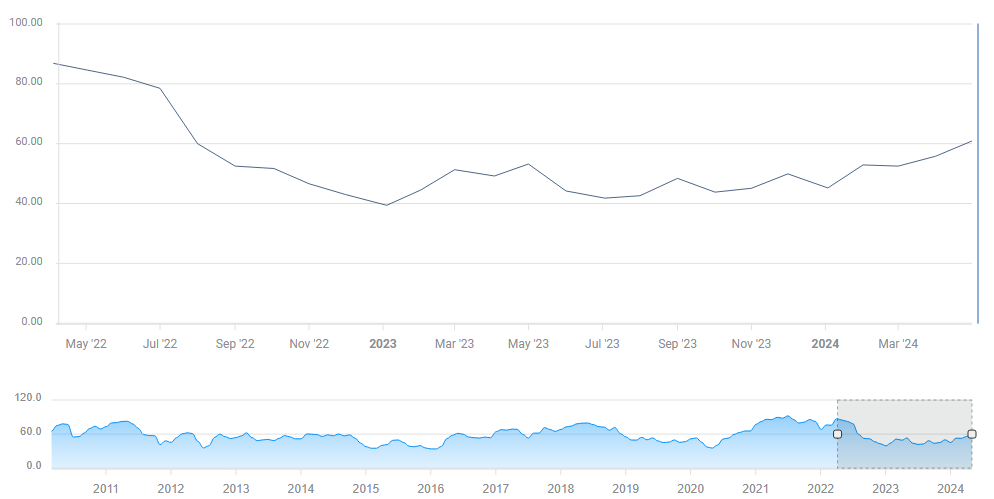

The Prices Paid component came out at 60.9, indicating elevated price pressures, and a minor retreat to 60 is on the cards in May. That would still be far above the 50-point threshold, which separates expansion from contraction.

Manufacturing inflation lifting its head:

ISM Manufacturing PMI Prices Paid. Source: FXStreet.

Given falling inflation pressures, as seen in core Personal Consumption Expenditures Price Index (PCE) and other data, I expect this figure to slide. That would boost stocks and Gold and weigh on the US Dollar (USD) ahead of next week's Federal Reserve’s (Fed) rate decision.

2) JOLTs to jolt markets, lower outcome on the cards

Tuesday, 14:00 GMT. This demand report in the labor market is for April – contrary to the Nonfarm Payrolls (NFP) figures, which are for May. Nevertheless, investors have learned not to fade this publication, as the Fed watches it closely.

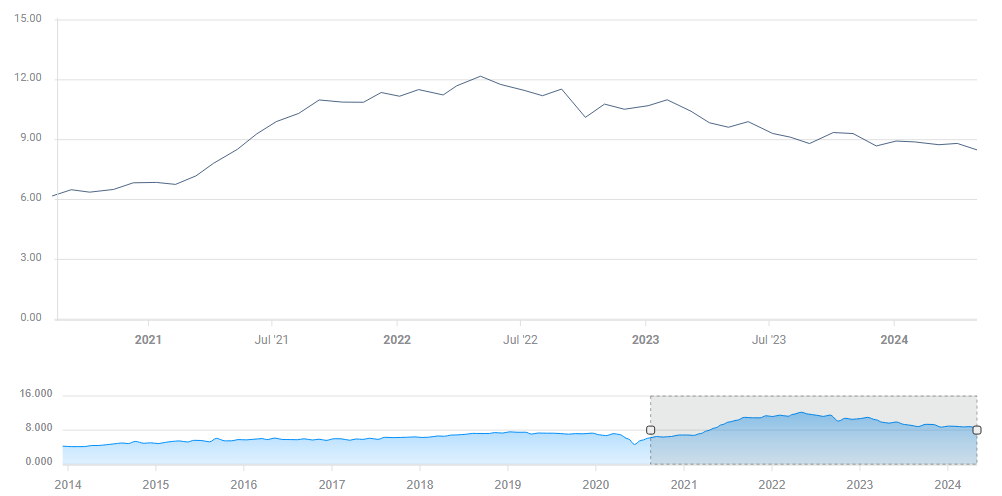

When JOLTs showed 8.488 million annualized openings in March, markets took it as a sign the labor market was cooling. Another drop to 8.34 million is on the cards.

Update: JOLTs hit 8.06 million annualized openings in April, below expectations and the lowest since 2021.

Fewer job openings, according to JOLTs

JOLTs. Source: FXStreet

Apart from the headline figure, the quits number is also of high importance. When people feel confident about their professional prospects, they tend to leave their jobs more frequently, while fear breeds sticking with the employer.

With a weak Nonfarm Payrolls report for April and minor rises in jobless claims, I think there is room for JOLTs to deteriorate even more than expected. At this point, bad news for the economy continues to be good news for markets, as they point to lower interest and slower growth – but not yet to a downturn. This will likely continue.

3) ADP jobs data could trigger the opportunity to go contrarian

Wednesday, 12:15 GMT. Roughly every sixth US payslip is processed by Automatic Data Processing (ADP), giving the software provider insights into the labor market. Its private-sector labor data serve as a leading indicator of the official Nonfarm Payrolls data, which is due out on Friday. That makes it a market mover.

Update: ADP jobs missed estimates with 152,000, below last month's downward-revised 188,000.

However, the correlation between ADP's and official figures is spotty. Moreover, the top-tier ISM Services PMI report is out less than two hours afterwards, giving investors something else to focus on.

Economists expect the ADP Employment Change to come out at 173,000 in May, a slight decrease from 192,000 reported in April. In case the data is wildly different, the impact would shape NFP expectations – rightly or wrongly – and the impact on markets would last for hours. That is an option to consider.

In most cases, a small miss or beat triggers a short-term impact, which is reversed shortly afterwards. That allows retail traders time to react and go contrarian.

ADP jobs. Source: FXStreet

4) Bank of Canada to cut rates, probably

Wednesday, 13:45 GMT. Between two key US events, its northern neighbour takes the spotlight. The Bank of Canada (BoC) is expected to cut its interest rates for the first time since March 2020, changing the Overnight Rate to 4.75% from 5%, which has been in place since July 2023.

Update: the Bank of Canada cut interest rates to 4.75% from 5.00%, as fully expected.

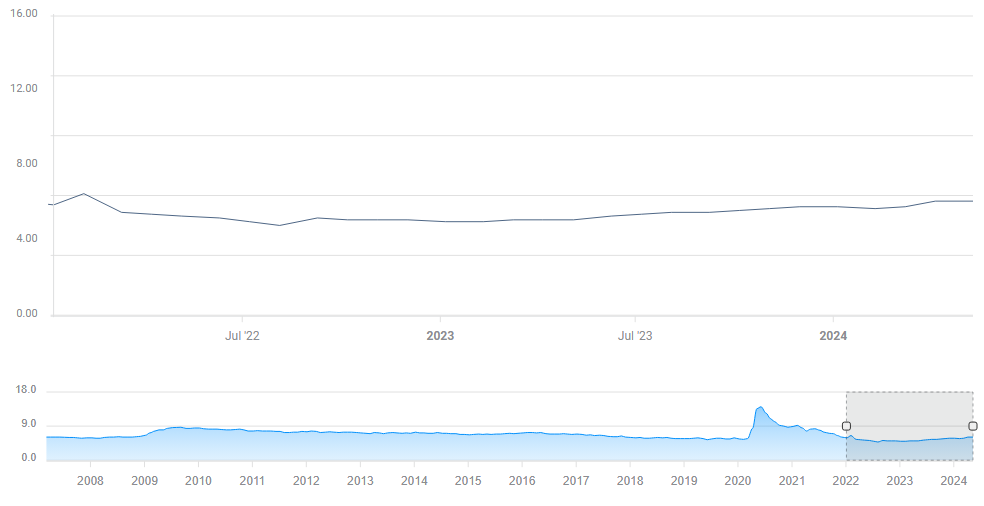

Weaker inflation pressures are behind the expected cut, but with the BoC, nothing is assured. Contrary to the Fed, the Ottawa-based institution does not shy away from surprising markets. While inflation is easing, the labor market seemed to have woken up, and the jobless rate unexpectedly stayed put in April.

Canadian unemployment holds at 6.1%. Source: FXStreet

The more likely scenario is an interest rate cut, but I expect the Canadian Dollar to weather the move, and even rise. Why? First, the decision is fully priced in. Second, BoC Governor Tiff Mackelm will likely reject expectations of a series of rate cuts, given the still-strong economy and the reluctance of the Fed to slash borrowing costs. Canada is highly dependent on the US.

The BoC's move will likely reverberate beyond the Loonie – it comes one day before the ECB decision and a week before the Fed. Markets are watching.

5) ISM Services PMI may cool markets and shape NFP expectations

Wednesday, 14:00 GMT. The worst of both worlds – that is how April's ISM Services PMI was described at the time. The forward-looking indicator for America's largest sector showed contraction, while its inflation component advanced.

Update: ISM Services PMI surprised by jumping to 53.8 in May, a big leap from 49.4 in April. It came alongside a small drop in the Prices Paid component.

Headline ISM Services PMI is set to rise to 50.5 from 49.4, crossing above the 50-point threshold and suggesting growth in the sector. While improved prospects would be good news for the economy, it would hurt stocks and push back expectations of rate cuts.

ISM Services PMI. Source: FXStreet

Investors may find solace if the Prices Paid component retreats from 59.2 seen last month. In the scenario I describe, the report would point to growth with lower inflation.

The employment component is also important. When it hit a four-month low of 45.9 in April, it signaled a weak Nonfarm Payrolls report. Most Americans work in the services sector, making this component another leading indicator – and the last one – ahead of the NFP.

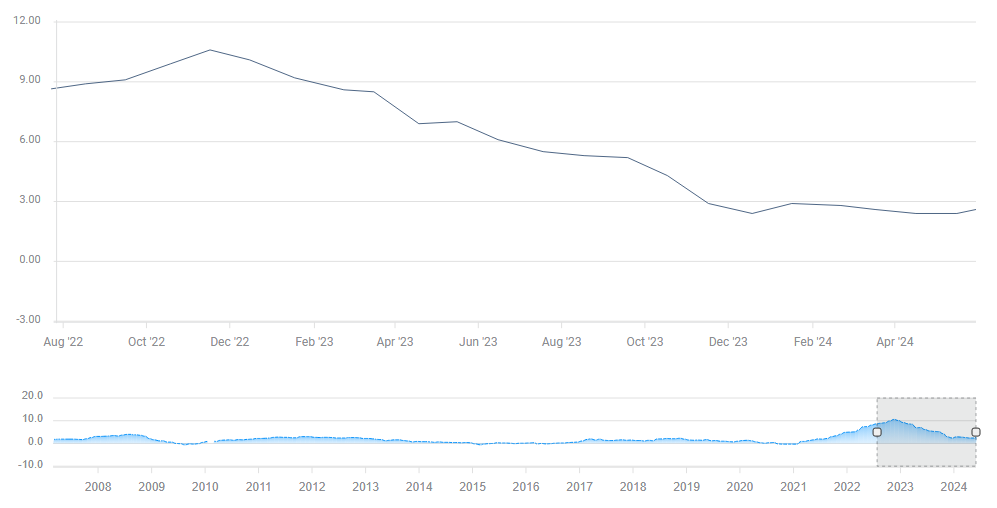

6) ECB to cut now, push back against more moves

Thursday, the rate decision will be at 12:15 GMT, and the press conference will be at 14:45 GMT. Are they declaring victory against inflation? That is how markets will see the first rate cut from the European Central Bank (ECB). Both headline and underlying inflation are below 3%, close to the bank's 2% target. That justifies slashing the Main Refinancing Operations interest rate to 4.25% from 4.50%.

Officials in Frankfurt and across the continent have signaled a cut is coming, and it is fully priced in. Investors will focus on the July decision. Is the expected move the first of many? Or just an initial one?

I expect ECB President Christine Lagarde to push back against another move – she is unlikely to commit to another move now. Apart from the usual comments about being data-dependent, Lagarde will likely point to the fact that inflation came out slightly above preliminary estimates in May.

Eurozone inflation down but not out. Source: FXStreet

Moreover, the old continent seems to be finding its feet and growing more satisfactorily. Using such arguments would help convince markets another cut is far from being certain, adding to the Euro's strength.

The ECB also publishes new forecasts alongside the statement, but markets will likely reserve judgment until Lagarde conveys her messages.

7) Nonfarm Payrolls may rock markets on a second consecutive miss

Friday, 12:30 GMT. Is unemployment making a comeback? Investors have been laser-focused on inflation in the past few years as it has risen – and as the Fed put all its efforts into crushing rising prices. However, there are initial signs that unemployment is creeping up – and full employment is the bank´s second mandate.

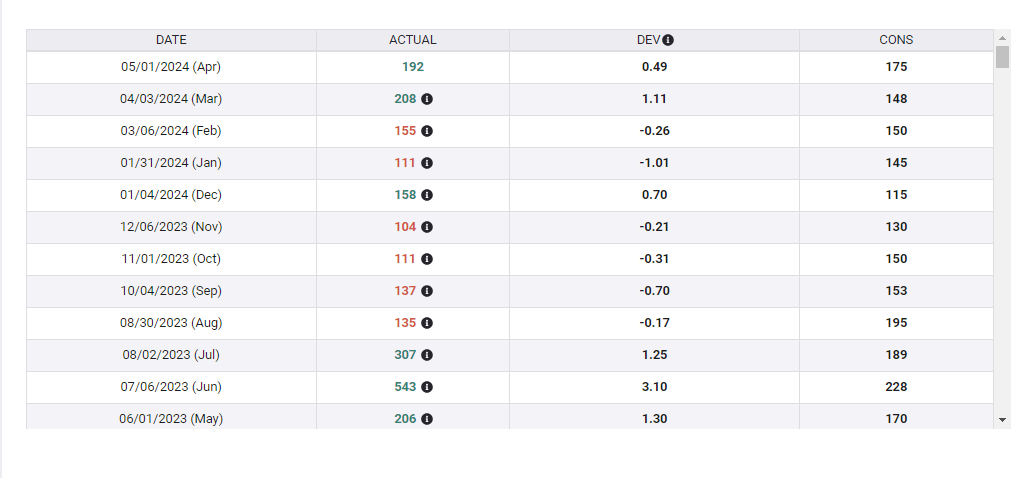

Headline Nonfarm Payrolls missed estimates in April, coming out at 175,000 vs. 243,000 expected. A similar increase of 180,000 is on the cards for May. A figure above 200,000 would be good news for the economy and the US Dollar but bad news for stocks and Gold. Anything under 150,000 would have the opposite effect.

Nonfarm Payrolls. Source: FXStreet

What about other figures? Average Hourly Earnings slipped to 3.9% year-over-year in April, showing that wage inflation is falling. A repeat of that figure is on the cards now, while monthly earnings are expected to rise by 0.3% vs 0.2% beforehand.

The wildcard is the Unemployment Rate. Markets usually dismiss this data point, as it is impacted by the participation rate, and they focus on changes in jobs and wages. However, if the jobless rate rises and hits 4%, a round number, it will get more attention.

Fed Chair Jerome Powell said a rate cut could come earlier in response to "unexpected weakness" in the labor market. A 4% handle on the unemployment rate might trigger hopes of an early cut from the Fed.

I expect weakness in the Nonfarm Payrolls report, leading markets to cheer at the prospects of lower borrowing costs – and ignoring the meaning for the economy.

Final Thoughts

Markets will get jittery around every news release in this busy week. I recommend trading with lower leverage and more care than usual.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.