Revised BoE call – Hot service inflation spells trouble

-

On the back of continued strong inflationary pressures in the service sector, as evident in the April inflation print, we revise our BoE call. We now expect the first 25bp cut in August (prev. June).

-

We expect quarterly cuts from August and through 2025, leaving the Bank Rate at 3.75% by the end of 2025.

Inflation in April surprised significantly to the topside across the board, relative to both the consensus expectation and the BoE’s forecast from the May monetary policy report. Headline came in at 2.3% y/y (cons: 2.1%, BoE: 2.1%, prior: 3.2%,), core at 3.9% (cons: 3.6%, prior: 4.2%) and services a 5.9% y/y (cons: 5.4%, BoE: 5.5%, prior: 6.0%).

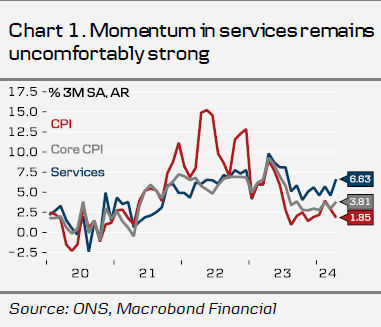

Although the year-on-year measures dropped notably due to base effects from energy prices and April-specific annual price adjustments (e.g rents, telephone contracts and tv licence fees), the underlying momentum remains strong. The big driver was services with a broad range of services such as hotels, restaurants and recreation and culture services delivering upward contributions. Service inflation remains key for the BoE as it uses it as a measure of inflation persistence alongside tightness of the labour market and wage growth. Worryingly, alongside the big BoE forecast miss, the momentum in service inflation picked up in April (see chart 1). Likewise, wage growth remains elevated with the labour market still tight by historical standards.

Following today’s topside surprise and the May print unlikely to deliver an equally large downside surprise to sway the majority of the MPC to vote for a cut, we now expect the first 25bp cut in August.

Our call. We now expect the BoE to deliver the first cut of 25bp in August (June previously). Given the later start to the cutting cycle, we subsequently now only expect one 25bp cut in the following quarter, totalling 50bp of cuts for 2024 (previously 75bp). Markets are pricing 40bp for the remainder of the year with the first 25bp cut fully priced by November.

Author

Danske Research Team

Danske Bank A/S

Research is part of Danske Bank Markets and operate as Danske Bank's research department. The department monitors financial markets and economic trends of relevance to Danske Bank Markets and its clients.