Rates spark: Some two-way risk in rates

Recession fears have injected much needed two-way risks in rates markets. Inflation swaps suggest expectations are anchored, but swaptions betray a record low degree of conviction. Together, they suggest limited risk appetite and the market remaining in a wait-and-see mode.

Interestingly, recession fears boiling over have brought much needed two-way risk in rates price action. This isn’t to say that the past few months were a smooth transition towards a world in higher interest rates, but it feels like last week’s rally has really woken up investors to the rates downside scenario. Central bankers are fond of splitting nominal interest rates between a real rate and an inflation expectations component, or between a short-term interest rate expectation and a risk premium. What do these approaches indicate?

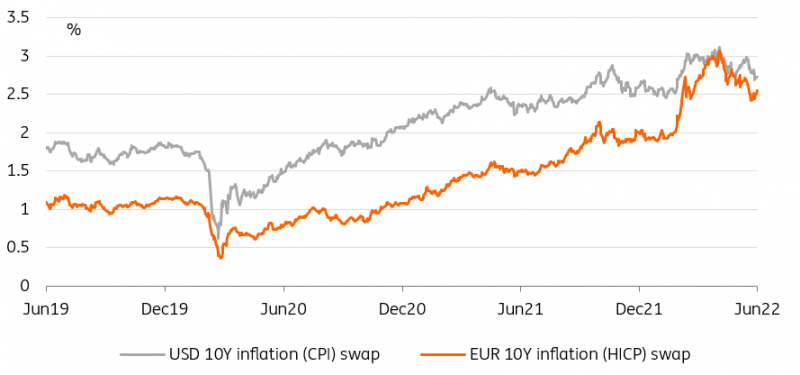

Inflation expectations may be under control…

In the first approach, long-term inflation swaps both in USD and EUR remain well below their peak in the spring. Clearly swaps do not equate inflation expectation for the broader economy, but they are a reliable indication of where large investors see the fair compensation for inflation risk over the longer-term. In that sense, they seem to suggest that central banks have regained control of the narrative and are expected to get on top of the current inflation surge, however long and painful the process may be. We fully expect European Central Bank speakers to repeat that they are alert to recession risks at today’s Sintra forum.

Inflation swaps show central banks have regained control of the narrative

Source: Refinitiv, ING

While it is premature to sound the all clear on the inflation crisis, this development is remarkable. No doubt that growing recession fears have contributed to calm long-term inflation swaps but this was far from a given. Increasingly, the debate on inflation has shifted to long-term dynamics, where a mild slowdown in growth would not guarantee a return to target. On that basis, we’re tempted to say that the upside in long-term yields is more limited than a few months ago, and that a bond market sell-off would likely be felt more acutely in the front-end. Eurozone inflation numbers, expected to show another acceleration later this week, will be a good test of this theory.

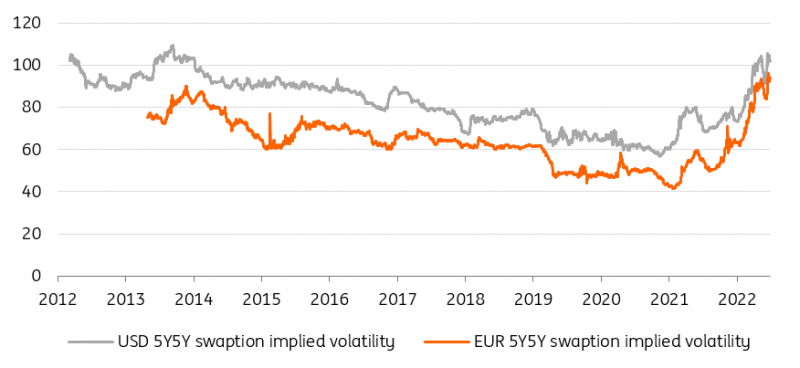

… but investor conviction is at a record low Risk premia are perhaps more difficult to measure, but there are proxies. We like to rely on the future interest rates volatility implied by the swaption market. If yields have so far remained under their recent peak, volatility has already printed new record highs. This is notable on two counts. Firstly, last week’s bond rally is the sort of event that would normally coincide with a drop in implied volatility, as market gyrations slow when rates approach their lower bound. Secondly, it shows that even with recession risks growing, investors aren’t necessarily pricing a return to the low rates environment of the past decade.

Implied volatility is already above its earlier peak

Source: Refinitiv, ING

With central banks no longer systematically supressing risk premia, we would refrain from calling the top in implied volatility. In the past decade, these levels of carry would have attracted investors in droves, but it seems not this time. What short volatility strategies have in common with bonds is that they offer carry but are exposed to sudden moves. It is a sign of the low degree of conviction in either of the competing narratives (durably higher inflation or severe recession) that implied volatility continues to rise, and probably points at durably depressed investor demand for bonds.

Read the original analysis: Rates spark: Some two-way risk in rates

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.