Rates spark: Putting disinflation to the test

The US disinflation narrative will have to pass a crucial test over the coming days, starting with today's University of Michigan inflation expectations release. However, key will be next Tuesday's CPI data. In the eurozone the European Central Bank balance sheet is featuring in officials' communication again of late, but for now with limited effect.

Key data points ahead to validate the disinflation narrative

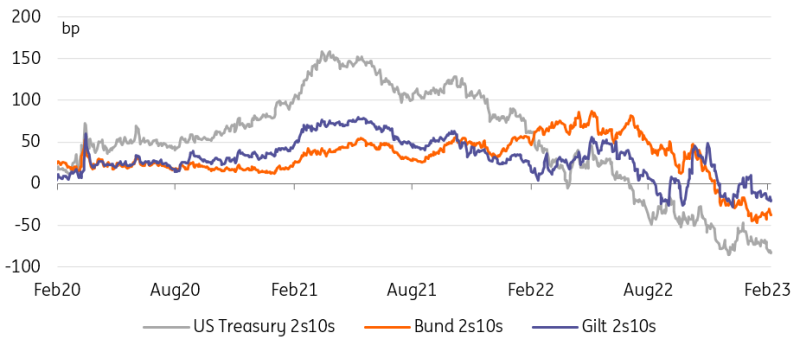

One striking market development over the course of yesterday’s session was the further inversion of the US Treasury curve, which hit another record low at -87bp.

We are inclined to read this as the Fed’s latest messaging working as intended in combination with the stronger data. This means that in the context of fine-tuning the policy stance, some more tightening may be possible near term, but for the longer-term outlook the market especially picked up on Powell signalling that disinflationary dynamics are already at play.

Starting today with the University of Michigan Consumer confidence survey and its survey inflation expectation and culminating in Tuesday’s CPI release, markets will be receiving key data points to corroborate their view of price dynamics having turned the corner for good.

Yet, today’s survey is actually anticipated to show a small uptick on the 1Y inflation expectations horizon. And next week, while the consensus is that headline inflation will further drop from 6.5% to 6.2% year-on-year and core to 5.5% from 5.7%, the month-on-month core reading is actually seen at a higher 0.4% – and keep in mind it is the month-on-month that usually gives a better picture of current price developments.

The most noticeable effect of more hawkish central banks and stronger data is deeper yield curve inversion

Source: Refinitiv, ING

Looking at the historically deep inversion of the US curve one should be forgiven to call out valuations as stretched as we have done for a while. But with so much of the benign outlook now riding on the disinflation narrative, it might just appear that the risk of a disappointment in the inflation data next week could have the larger market impact. Note that we will also be getting activity data, which will likely have benefitted from mild January weather.

In hindsight some market unease about what lies ahead in coming days combined with how far relative valuations had evolved can explain the soft 30Y auction result that triggered a correction in rates last night, lifting yields temporarily by 8bp from the lows of the day.

ECB officials take renewed stabs at the balance sheet

In the eurozone the German inflation data came as a delayed reminder that the ECB is facing a longer fight against inflation. We had highlighted the limited success so far of the latest ECB meeting and subsequent communication to get the hawkish message across to markets. Perhaps that is the reason why we have seen some of the hawkish ECB members of late resorting to communication on the balance sheet again after some pause on this topic. Klaas Knot had kicked this off on Wednesday stating that stopping the reinvestments of the asset purchase programme portfolio should be the ultimate goal. Yesterday, the Bundesbank’s Nagel stepped up the game and called for a more ambitious roll off of the portfolio, arguing that the reductions would need to pick up speed.

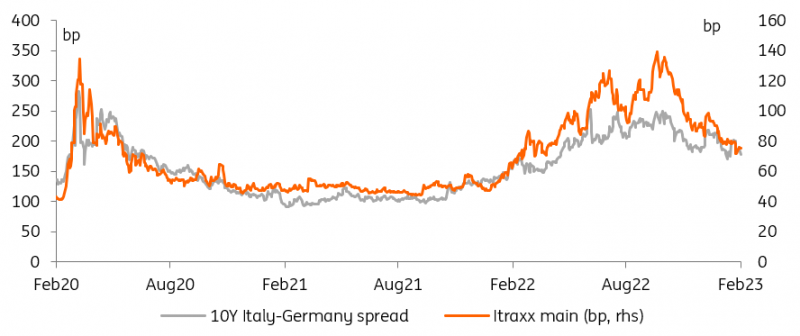

While on the face of it such comments are certainly hawkish, the market is already discounting the end of reinvestments starting in the second half of this year to a large extent. As much can be gleaned from the ECB’s own survey of analysts conducted ahead of each meeting. That, and also given it has been few voices only, should explain why government bond spreads are largely unfazed for now. But it also poses the question what is the next step up in hawkishness if the ECB want to “show its teeth” again as Austria’s Holzmann put it at the start of the week.

Credit and sovereign spreads tighten but ECB hawks want to accelerate QT

Source: Refinitiv, ING

Read the original analysis: Rates Spark: Putting disinflation to the test

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.