Rates Spark: Lost in translation

Fed Chair Powell has a clear ambition to hike by 50bp in December, and likely the same in February 2023, and maybe more. Given that, and a likely terminal funds rate of at least 5%, the drift lower in the US 10yr yield looks anomalous. Then again, year end can be like that. A move back above 4% still looks probable – it just might take a bit longer to achieve.

A hawkish hike (even if smaller) now needed to help re-tighten conditions

If Chair Powell wanted to use yesterday’s speech to help re-tighten financial conditions, then he won’t be very happy with the impact market reaction. Market rates have fallen, credit spreads are tighter and effectively we’ve gone “risk on”. Financial conditions started out at about 0.6 of a standard deviation tight versus normal pre-Powell. They are now at closer to 0.5 of a standard deviation tight. We think it needs to be a full standard deviation tight, to be at least somewhat statistically meaningful.

The reason we are not tighter is (mostly) lower market rates and tighter credit spreads. The US 10yr is now down to 3.7%, more than 50bp below the peak seen at end-October / early-November. Some 8bp of that has come in the wake of Chair Powell’s speech today. At 3.7%, the 10yr yield is some 130bp below the discounted terminal rate of 5%. That’s quite a spread. We think it’s far too wide. It’s telling us one of two things: (1) If the Fed hits 5%, then it’s not sustainable and a cut is coming really soon after that, or (2) The Fed will in fact not hit 5% at all, and they are done in December.

Our view? We think the Fed does hit 5% (in February), and that the 10yr should be comfortably back above 4% in anticipation of that. This can happen soon, but could also morph into a turn of the year call, as we're now in this weird end of year swing where anything can happen. There can be some net buying going on as investors square books into year end, often buying back duration that had been shorted during the year. The first quarter of 2023 will bring the realization that the flip from 22 to 23 does not magically rid us of inflation risks that the Fed will feel emboldened to continue to address. Market rates are not fully reflecting this; but they will.

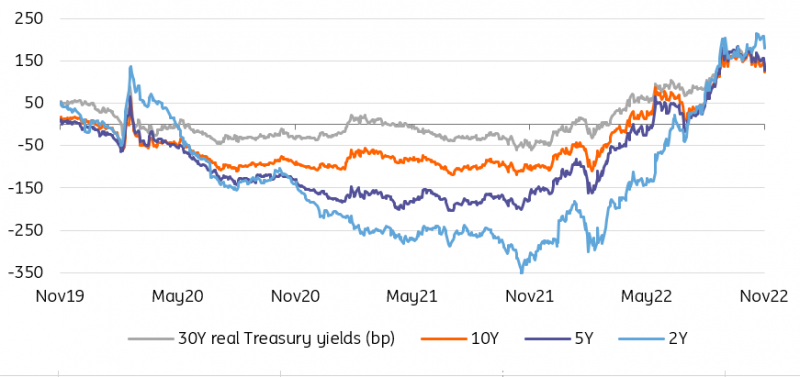

Real Treasury yields are positive across the curve, the Fed will want to avoid an early drop

Source: Refinitiv, ING

EUR inflation solidifies expectations for a 50bp hike

The eurozone flash CPI sees inflation having decelerated to 10% in November versus expectations of only a moderate slowing to 10.4% had surprisingly little effect on the market. Our economists also see this report having strengthened the case for a 50bp hike in December after the series of 75bp over the past meetings, but the market has been leaning to a slowed pace already in the wake of the first country readings at the start of the week, reducing the discount to only slightly more than 20% for still another larger 75bp hike after around 50% previously.

Yet away from the energy price-induced, headline-grabbing drop to 10%, the more relevant core measure of inflation has not budged and remains at a painfully elevated 5% year over year, in line with the consensus. The European Central Bank has rightly shifted the focus of the policy debate to underlying inflation and its persistence, being well aware that drops in the volatile headline can lead to false dawns.

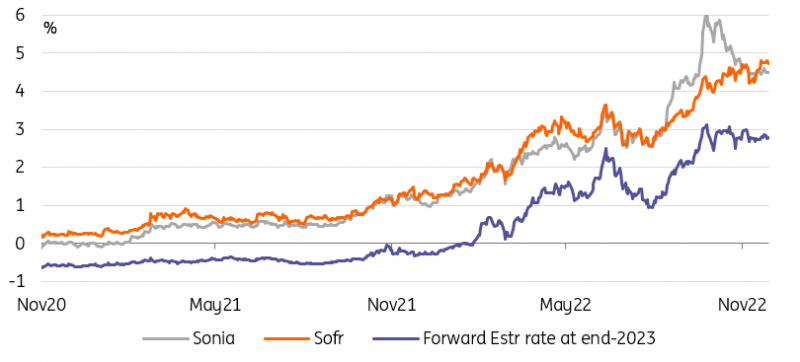

The bond rally has limited - but not reversed - ECB and Fed hike expectations

Source: Refinitiv, ING

The ECB’s Isabel Schnabel has been the most vocal about still worrying underlying trends in her latest speech last week. Chief Economist Lane has employed a more measured tone in his latest expansive blog, though, warning not to read too much into current measures of underlying inflation. In particular he cautioned that the staggered adjustment of wages to the increase in the cost of living can play out over several years, but shouldn’t automatically signal a change in overall wage dynamics, i.e. the onset of a much feared wage-price spiral.

That the ECB isn’t done raising rates is clear. While it is widely accepted that the ECB will have to move into restrictive territory is also widely accepted, the latest inflation data has taken the edge off calls for more larger pre-emptive hiking. This also means that the tailwind for a further curve flattening dynamic is fading, but it should not distract from the prospect of rates possibly staying higher for longer. Similar to the Fed, the ECB should still have qualms about letting financial conditions ease too much, too early in its battle with inflation.

Read the original analysis: Rates Spark: Lost in translation

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.