Potentially dovish ECB could accelerate EUR/USD’s breakdown

This week was all about the pound; next week could be all about the euro. The pound’s rally came to an abrupt halt as economic data from the UK disappointed expectations and after the Bank of England Governor Mark Carney warned that a rate rise in May was not a forgone conclusion. The resulting rally in the EUR/GBP initially kept the EUR/USD supported. But as the dollar started to push higher due to the rising short-term government bond yields, the EUR/USD also fell in the greenback’s slipstream. Although the world’s most heavily-traded pair is still stuck inside its existing consolidation range, this week’s price action points to a potential breakdown next week.

ECB in focus

That being said, though, there isn’t much in the way of economic data from the US for much of next week to keep the dollar supported. But the dollar index could nonetheless find direction from the EUR/USD. The European Central Bank rate statement and press conference on Thursday has the potential to move the euro sharply and we think Mario Draghi and co will give a more dovish assessment of the Eurozone economy given the recent soft patch in German data. This could undermine the euro and underpin the dollar. In addition to the ECB, the Bank of Japan will also be making its own policy decision next week, too. And if the BOJ also turns out to be more dovish than hawkish then this could further boost the Dollar Index.

Eurozone PMIs and US GDP among next week’s key data

In terms of macro data, we will have plenty of Eurozone manufacturing and services sector PMIs on Monday, while on Tuesday the German Ifo Business Climate will be published. The German GfK Consumer Climate index will come out on Thursday, a few hours prior to the ECB policy decision. On Friday, we will have French and Spanish GDP estimates, as well as Spanish CPI and German unemployment data. As far as US data is concerned, existing home sales (Monday), CB consumer confidence (Tuesday), durable goods orders (Thursday) and the first estimate of Q1 GDP (Friday) will all be published next week. So, there’s plenty of macro data to keep everyone busy.

EUR/USD’s path of least resistance is to the downside

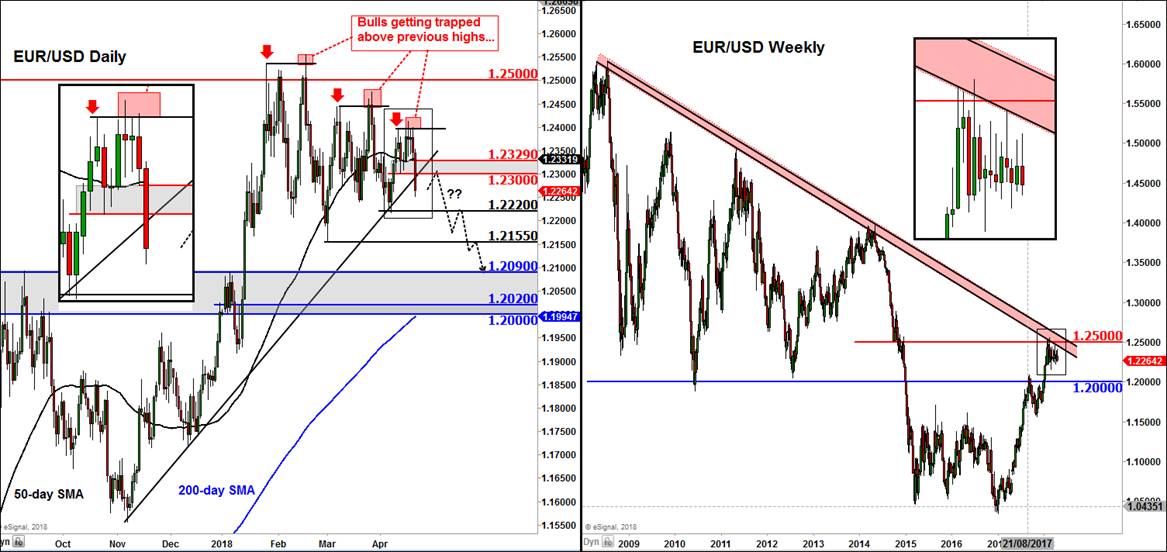

From a technical point of view, the EUR/USD could be on the verge of a breakdown, at least a short-term one. The long-term weekly chart clearly shows that the almost 1.5-year-old rally is stalling around the psychologically-important 1.25 handle, where we also have a long-term bearish trend line converging. On the daily chart, the bearish view is bolstered by signs that the recent breakout attempts have continually failed. In each of the previous three occasions where price has tried to take out its previous swing high, there has been no commitment from the bulls. This is strongly suggestive of smart money distribution phase. They are selling into the rallies, in other words. With price now below the 50-day average and below a bullish trend line, it is now becoming more evident that the path of least resistance is to the downside. We therefore expect the broken support levels to now turn into resistance, starting at 1.2300 and then 1.2330. The next pools of liquidity below market will be underneath the previous swing points such as 1.2220 and 1.2155. We think that this is where price may go towards next as the cluster of resting sell stop orders attract price towards it. Our ultimate bearish objective is at around the 1.20 handle, with intermediate and key support coming in at 1.2090 first – this being last year’s high. We will drop our bearish bias in the event the EUR/USD now makes a higher high above the 1.24 handle.

Figure 1:

Author

Fawad Razaqzada

TradingCandles.com

Experience Fawad is an experienced analyst and economist having been involved in the financial markets since 2010 working for leading global FX, CFD and Spread Betting brokerages, most recently at FOREX.com and City Index.