Oil price is absolutely central to inflation

Outlook:

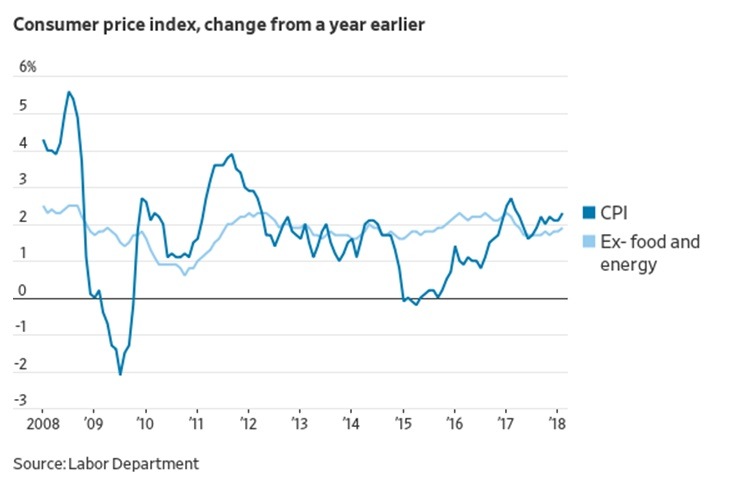

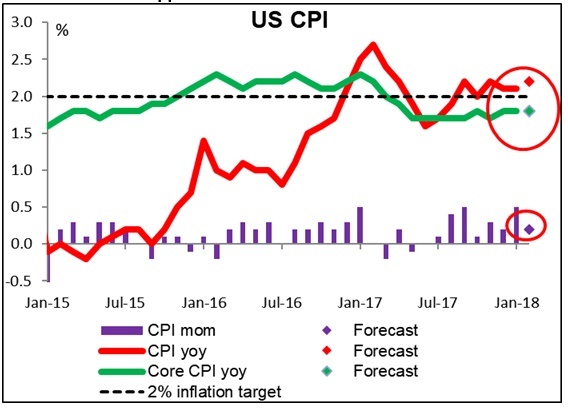

The focus on CPI this morning is misguided. The Fed has a forecast of its measure, the core PCE deflator, meeting the 2% target this year, hence the preemptive hike next week. Core CPI is at 1.8% and the PCE is at 1.7%. So far, so good. But again we have to complain that the Fed excludes food and oil prices on the grounds they have their own cyclical and globally generated moves and cannot be "managed" by monetary policy.

Everyone seems to forget this critical factor when attributing massive power to the Fed. The Fed itself does nothing to disabuse the world of this terrible, awful shortcoming. This is an old hobbyhorse of ours—we neglect oil's contribution to inflation because the Fed does. But oil is absolutely central to in-flation. Go figure.

The US has been raising its contribution to global oil supplies for several years now. Weirdly, oil prices persist in running around $65 as though conditions have not changed and OPEC is still controlling pric-es. Perhaps the US is at the extreme high end of production and output gains will decelerate from here, but the structure of the market has been permanently shifted. The US doesn't exactly control price con-ditions, but prices are not reflecting this tectonic shift, either. The logical deduction of a slowing global economy and less pricing power to OPEC producers is a longer-term, cyclical drop in the price of oil and oil products (gasoline, diesel, etc). Nobody has a crystal ball and political risk is vast, but unless there is a supply disruption somewhere important, supplies are outpacing demand already and the gap is likely to grow, according to the EIA.

Direct and indirect effects will emanate in all directions from lower crude prices. Let's say aviation fuel prices fall alongside crude. Does this mean lower consumer airfares and commercial shipping costs? Oil permeates everywhere. Diesel will cost less, reducing truckers' fees. Fertilizer will cost less, so food prices may fall a little. Actually, food prices may fall a lot if the Trump tariffs invite retaliation against US grain and other agricultural exports. Home heating oil will fall, leaving a little more in household wallets.

The world does not yet see lower oil prices. Goldman has a forecast of Brent at $60 by 2020. The EIA itself has an average of $60 this year and $61 next year, vs. the 2017 average of $54. We are hard-pressed to find anyone forecasting oil down to $45-50, and yet logic dictates that's where it "should" go. We would give a lot to know the Fed's oil price forecast.

A tiny hint: the Saudis are not expecting a drop in oil prices, but investors are leery of the offering price of the 5% of Aramco that was supposed to be listed this year. Now it's delayed a year, in London, anyway, because buyers don't like the $2 trillion price-tag the Saudis are placing on it.

Charts are little help. See below. A downside breakout from the triangle is not the consensus forecast, but not out of the question.

Analysts say we should expect a change in the euro/dollar rate by 30-45 points on release of the CPI news today. Even if it goes further, stiffen your spine and ignore it. Longer-term, markets do not expect a spike in inflation. In fact, the 5-year breakeven expects a dip. Given the Fed hike next week is already baked in, we should expect disappointment over the CPI number to reverberate to the dollar's detri-ment. This is one of those times when the commentariat is well and truly out of sync with the data. Having said that, the last time we had this situation (hourly earnings seeming to rise), markets overre-acted. Just as with the FX market responding uncharacteristically to the corruption story in Japan when corruption stories had no effect for over 30 years, we expect the unexpected today.

Fun Tidbit: Whispers are getting louder that Larry Kudlow will replace Gary Cohn as chief economic advisor to Trump. We know Larry well from days of yore. This is a guy who changes his mind every day when he changes his socks. After supporting supply side economics, aka voodoo economics, he wrote a book admitting it was a dumb idea and had not worked, but ten years later, there he was on TV promoting it again. If we have to have a TV guy, Cramer would be smarter. We know him, too. But Cramer, despite his show-biz antics, wouldn't take the job. He has too much self-respect.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes. To see the full report and the traders’ advisories, sign up for a free trial now!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat