November flashlight for the FOMC blackout period

Don't Expect the FOMC to Make Any Big Changes at Next Meeting

When the Federal Open Markets Committee (FOMC) meets in the first week of November there will be many things it is eager to see but few of which will be in clear focus at that point. The paramount concern is the state of the economy, which continues to expand albeit at a significantly slower pace than in the third quarter.1 It has only been six weeks since the September 16 FOMC meeting, which itself came on the heels of a seminal development at the Kansas City Fed's annual Jackson Hole symposium in August when Fed Chair Jerome Powell announced the adoption of a flexible average inflation targeting regime. On that basis, we are not bracing for any major shift in policy or forward guidance at the November FOMC meeting.

The FOMC meeting concludes on November 5, within 48 hours of Election Day on November 3. With mail-in votes expected to play a larger-than-usual role amid the pandemic, the outcome of the election could still hang in the balance from the top of the ticket to down-ballot races. Various Fed speakers in recent weeks have stressed the economic need for additional fiscal stimulus, and the outcome of the election has the potential to influence the complexion and timing of future stimulus.

In this edition of our Flashlight for the FOMC blackout period, we discuss how even in the absence of major fiscal policy developments, the Federal Reserve has a few potential remedies at its disposal for a still-ailing economy and low inflation. These include ramping up its asset purchase program or further easing the terms of its emergency lending programs, such as the Main Street Lending Program (MSLP) and the Municipal Liquidity Facility (MLF). The September meeting included an update to the so-called dot plot and the Summary of Economic Projections (SEP), as well as the initial rollout of 2023 forecasts from FOMC members. We also discuss what these projections might mean for Fed asset purchases in the months ahead.

Will the FOMC Soon Try to Speed up the Return to 2% Inflation?

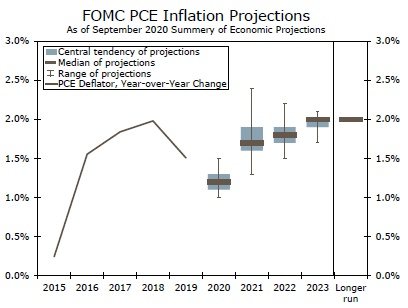

The FOMC is expected to be in a holding pattern at the November meeting, but economic conditions generally, and inflation specifically, could press members to announce accommodative steps in upcoming meetings. The September SEP showed FOMC members generally expected a somewhat stronger recovery in GDP and the labor market compared to June. However, the bulk of the committee did not expect inflation to reach its longer-run goal of 2.0% until 2023. Even then, most members did not expect inflation to exceed the Fed's goal, which would be needed in order for inflation to average 2% over time, as per the committee's recently updated Longer-Run Goals and Monetary Policy Strategy (Figure 1). Between now and 2023, only two of the seventeen committee members anticipated inflation surpassing 2.0% in any given year.

Source: U.S. Department of Commerce, Federal Reserv e Board and Wells Fargo Securities

Importantly, according to the minutes of the September meeting, "many" members' outlook for the economy assumed additional fiscal stimulus to be coming down the pike. Over the past couple of months, there has been a steady stream of comments from Fed officials suggesting more fiscal support is crucial to the next leg of the recovery, and that fiscal policy is a better tool to support the economy at this juncture given the nature of this crisis. With another fiscal package yet to be secured, its size uncertain and its timing increasingly pushed back, a "substantial majority" of participants considered the risk to the inflation outlook as tilted to the downside.

The window for another fiscal package before the election or next January is quickly closing. Moreover, even if lawmakers were able to deliver an agreement soon, a three-year wait for inflation to return to 2% may prove too long for some Fed officials. Therefore, the FOMC is likely to look harder at additional ways in which it can support the recovery at its upcoming meeting.

Further asset purchases are likely at the top of the list, in our view. Currently the Federal Reserve has been buying roughly $80 billion of Treasury securities and $40 billion of mortgage-backed securities (MBS) each month. We believe it is premature to expect an announcement of additional asset purchases at the November FOMC meeting. The election results may be unknown, and we suspect the committee would like to see more data on how a "third wave" of COVID cases is affecting economic activity. In addition, Treasury yields remain extraordinarily low, watering down the impact of additional purchases at the moment.

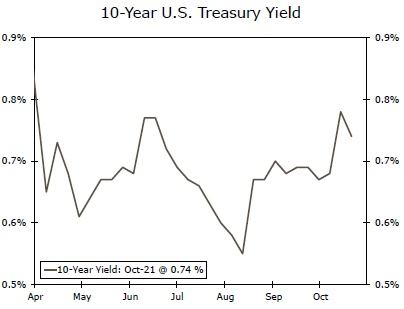

That said Treasury yields have started to grind higher (Figure 2). With the tenuous outlook for inflation, the FOMC may feel compelled to do something soon, and it could potentially announce an increase in Fed purchases as early as its subsequent meeting on December 15-16. While current asset purchases are being undertaken in part to help market functioning, the primary intent of additional asset purchases at this point in time would be to achieve the committee's employment and inflation goals, with purchases therefore likely to be focused on the longer-dated Treasury securities.

What Ever Happened to Those Emergency Lending Programs?

When Congress passed the CARES Act in late March, it included $454 billion for the Federal Reserve to "make loans and loan guarantees to, and other investments in, programs or facilities established by the Board of Governors of the Federal Reserve System...that supports lending to eligible businesses, states, or municipalities." This sizable pot of money was designed to serve as a massive equity infusion into the Federal Reserve to facilitate new types of lending programs/asset purchases outside of traditional, government-backed assets like Treasury securities or mortgagebacked securities.

Perhaps the three most headline-grabbing programs to spring from this equity base were the Main Street Lending Program (MSLP), for lending to small- and medium-sized businesses, the Municipal Liquidity Facility (MLF), which is to be used for lending to state and local governments, and the Corporate Credit Facilities (CCF) for purchases of corporate bonds on the primary and secondary markets. These three areas were segments of the financial sector in which the Federal Reserve had historically played little to no role when it came to direct lending. With the potential to lever up that $454 billion into trillions of dollars, the central bank had the firepower to become a big player in these credit markets overnight.

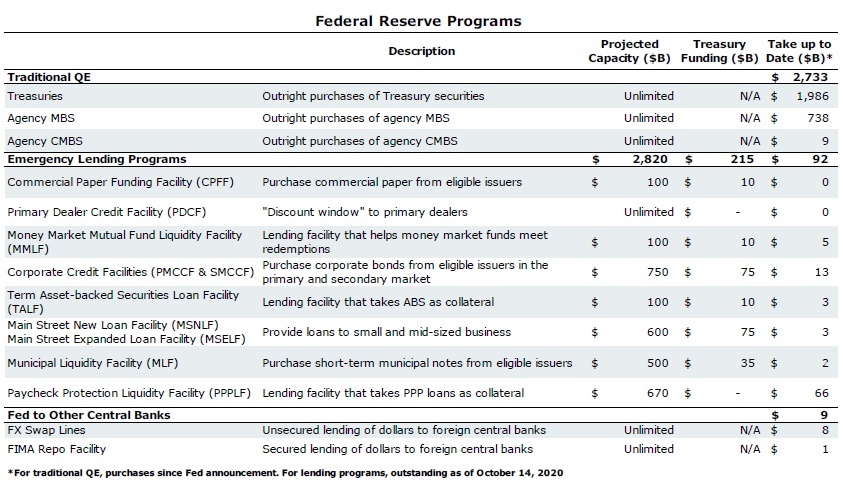

Fast forward to today, and the actual amount of assets the Federal Reserve has taken on to its balance sheet from these programs is quite small (Figure 3). The MSLP has extended about $3 billion worth of credit to small- and medium-sized businesses, and the MLF's holdings are even lower at roughly $2 billion. The CCF has been a bit more active, but at only $13 billion to date, this is merely a drop in the bucket in the roughly $11 trillion corporate bond market.

Source: Federal Reserve Board and Wells Fargo Securities

So why hasn't take-up been more robust? To some extent, the programs' relatively small size reflects the fact that the economic outlook has improved since the spring when they were originally designed. Economic activity is steadily rebounding from its April low, and the unemployment rate has fallen to about 8%, roughly where it was in late 2012. Furthermore, financial market functioning and capital market access have improved, as spreads on municipal and corporate bonds have generally tightened and issuance is robust. To some extent, this is also just the nature of the Federal Reserve's role in economic policy; the Fed is the lender of last resort, and unlike Congress, the central bank cannot simply deliver mountains of cash with no strings attached. As the pandemic has worn on, companies and state and local governments may be thinking more about the long-run viability of their business and fiscal plans, rather than just their short-term access to credit and liquidity. This in turn could lead to a hesitancy to borrow, even at favorable rates.

As time has passed, the Federal Reserve has tweaked some of the terms of these facilities in order to help encourage more utilization. For example, the Fed extended MSLP loans out to five-year maturities, from four years previously, and it made principal payments deferrable up to two years instead of the previous one. And for the MLF, the Fed cut the interest rate spread on tax-exempt notes by 50 bps for each credit category. But, it does not appear these tweaks have been enough to encourage more broad-based take up.

We doubt the FOMC or the U.S. Treasury want to see the nation's central bank recklessly lending in a way that leads to credit misallocation and/or large losses for the Federal Reserve. That said, the $454 billion of financial firepower sitting on the sidelines has certainly been underutilized, and it seems unlikely to play a big role in the recovery anytime soon. Perhaps if FOMC members feel that the Fed's traditional options like quantitative easing are no longer effective, and if they continue to eschew other steps like negative rates or yield curve control, they could more materially ease the terms of the previously discussed lending programs. While it would be difficult to thread the needle, if done effectively, the Federal Reserve could help provide credit to segments of the economy that need it while also using the tools at its disposal to absorb some moderate credit losses currently occurring in the private sector.

Download The Full Special Commentary

Author

Wells Fargo Research Team

Wells Fargo