Negative Yield Curves to Infinity and a Reader Question Regarding Fraud

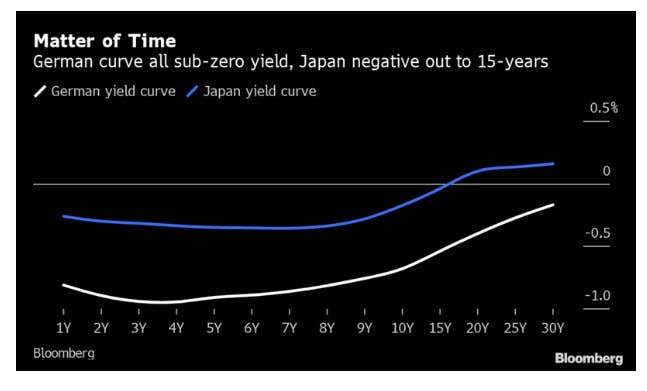

The entire German yield curve is negative for 30 years. Japan is poised to join the club.

Bloomberg reports Japan Lines Up to Join Germany in All-Negative Yield Curve Club.

Yields in the Asian nation are already negative all the way out to debt maturing in 15 years, and buyers from home and abroad have been snapping up longer-tenor Japanese government bonds, adding to the downward pressure.

International investors are profiting by lending dollars for yen via currency forward contracts and plugging the proceeds into JGBs, while domestic players benefit from the slope of the yield curve by borrowing over a short time frame and putting the money into longer maturities where yields are higher.

“Investors are seeking to buy 30- and 40-year bonds while there are positive yields left,” said Tadashi Matsukawa, head of fixed-income at PineBridge Investments Japan Co. “They face the possibility that yields across all maturities will fall into negative territory.”

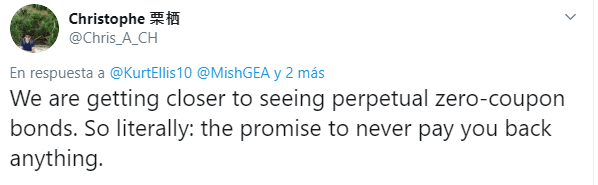

No Brainer

To Infinity and Beyond

Why stop at 30 years or even 40 years?

Why not offer perpetual bonds with a negative yield?

Negative Yields Fundamentally Impossible

Negative yields are fundamentally impossible in the absence of central bank manipulation or monetary fraud.

That is not an opinion, it is a statement of fact. It is impossible for someone to prefer 89 cents ten years from now to a dollar today.

Yet, I see some people whom I respect attempt to explain the matter.

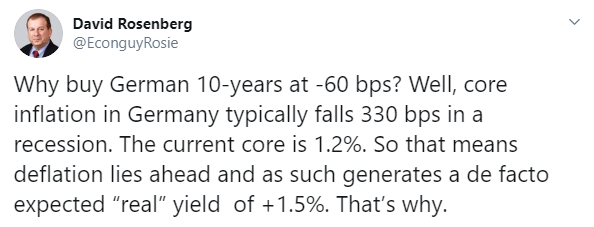

Deflation Ahead

I agree that deflation is ahead, but I am sorry, that's not a valid excuse to buy negative-yield debt.

Currency Component

One of my readers commented "You are forgetting the currency component."

That statement is in apparent "carry trade" sympathy with Bloomberg's "No Brainer".

Excuse me for pointing out there is no risk-free arbitrage.

Carry trades blow up all the time and the next one will be a doozie. I expect many hedge funds will blow up on these kinds of bets.

Logically Impossible

Let's not equate speculative activity with the fundamental impossibility of someone actually preferring 89 cents ten years from now to a dollar today.

That is precisely what Swiss bond yields imply.

Yet, Rosenberg made the same rationalization as my reader.

Safekeeping

Again, note out the difference between safekeeping services and negative interest rates.

One would expect to pay a small nominal storage cost for gold (or cash).

But if one lent gold (or cash), as opposed to placing it in a bank for safekeeping, the yield would never be negative or zero. Never.

That one might choose to speculate in negative yield bets via carry trades or the greater fool's theory does not negate this simple fact: Time preference can never be negative except by central bank manipulation and outright monetary fraud.

Understanding the Point

Question of Fraud

Another reader commented "I don't understand how negative interest rates are fraudulent. The bond issuer is promising to pay fewer dollars upon maturity than the buyer is spending to purchase the bond. There is no fraud."

Of course there is manipulation and fraud.

Once again, Interest rates could never be negative without central bank manipulation.

The ECB engaged in massive QE, printing money out of thin air, forcing banks to take the money, then setting rates negative robbing banks of earnings. That's a huge fundamental mistake and it has backfired already.

If you do not like the word fraud, call it robbery. It is not much different than the playground bully demanding money in return for the right to walk to class unmolested.

Banks have to take the offer. In return, we are now seeing things like banks charging consumers for deposits. Negative interest rates on deposits rob depositors because they are forced upon them.

If something that cannot logically happen, actually happens, look for manipulation and fraud as the obvious explanation.

What's Happening?

- To create "excess reserves" central banks, via asset purchases, flood banks with dollars (euros or yen) the banks do not even want because banks believe they cannot lend them profitably.

- In the case of the ECB, the central bank charges the banks interest on the euros crammed down their throats.

Mathematical Certainty

In Europe, the US, Japan, and everywhere, it is a 100% mathematical certainty that someone has to hold every dollar, every euro, every stock, and every bond 100% of the time.

Please read that two or three times until it sinks in.

Someone must hold every security and every dollar. One cannot sell stocks and buy bonds without someone else doing the opposite.

Given there is a seller for every buyer, only the ownership transfers.

Manipulation, Fraud, or Theft?

In this case, the ECB prints euros the banks do not even want, yet someone has to hold the damn things, 100% of the time come hell or high water, no matter what interest rate the ECB sets.

Then the ECB charges the banks interest on the money printed out of thin air while simultaneously setting the short-term rate negative.

This has destroyed Eurozone bank profitably. In contrast, the Fed paid interest rates on excess reserves, slowly bailing them out over time.

Making Sense of It All

One can label these central bank strategies manipulation, theft, or fraud.

Select the term that suits you best.

But that is the correct way of Making Sense of 100-Yr Bonds yielding 0% and 30-Yr Bonds With Negative Yield.

Also, please consider Fed Baby Steps Coming: What's Powell Up To?

My short answer is the Fed wants to avoid the Eurozone negative rate trap.

Author

Mike “Mish” Shedlock's

Sitka Pacific Capital Management,Llc