Navigating the FX landscape: Understanding trends and data available

In today's evolving financial landscape, a comprehensive understanding of the Foreign Exchange (FX) market is essential. In our latest article, Chris and Sal examine FX market dynamics, uncovering trends and discussing how external factors, including Central Bank Monetary Policy decisions, affect market data.

FX market dynamics: Influential factors

Global economic and political landscape

The FX market is subject to constant evolution, influenced by geopolitical tensions and Central Bank monetary policy decisions. Major political events, such as elections and geopolitical conflicts, inject volatility into FX markets, shaping investor sentiment towards currencies

Central Bank monetary policies

Central Banks play a significant role in FX markets through their monetary policy decisions and communication strategies. Following a lengthy period of global low-interest rates, pre-COVID, Central Banks embarked on a period of significant rate hikes to combat rising inflation. However, as some economies are now showing signs of a pending economic slowdown, there is a growing focus on reversing course towards interest rate reduction policies. Major Central Banks, like the European Central Bank (ECB), Bank of England (BOE), and the Federal Reserve Bank (FED), are closely monitoring monthly economic data for signs of decelerating growth and stabilizing inflation. Meanwhile, Central Banks in Asia are instituting stimulus measures to strengthen their economies. For instance, the People's Bank of China (PBOC) is addressing an economic slowdown by encouraging local bank lending by lowering their reserve requirement ratios. Similarly, the Bank of Japan (BOJ) has announced the end of negative interest rates and a departure from its Yield Curve Control policy. Market participants are closely watching Central Bank communications for insights into future policy revisions, with the goal of a smooth transition amidst changing economic conditions

Factors driving central bank decisions - Economic indicators

Central banks, including the ECB, the BOE, and the FED, need to monitor economic data signals to guide their monetary policy decisions. Their primary focus is to identify markers supporting a shift towards a policy of rate reduction, while also trying to avoid acting prematurely. Their aim is to be patient, digest the economic data, and begin their rate reduction policy at the appropriate time. Essentially, to achieve a “soft landing”.

Key economic indicators, such as monthly unemployment figures, wage trends, and inflation markers, such as Consumer Price Index (CPI) reports, play pivotal roles in determining the direction of monetary policies. Recent data from February and March shows nuances in the economic landscape. For instance, in the US, while February's CPI indicated a cooling inflation rate at 3.1% instead of the projected 2.9%, March's report came in slightly stronger at 3.2%, reinforcing the FED's cautious standpoint on rate reductions. Moreover, the US unemployment rate for the past two months came in at 3.9%, accompanied by downward revisions to recent non-farm payrolls figures from prior months, suggesting a potential softening in the labor market. This recent economic data fuels speculation that the FED may look to implement its first rate cuts around mid-year, underscoring the central bank's reliance on economic data for the timing of a policy shift.

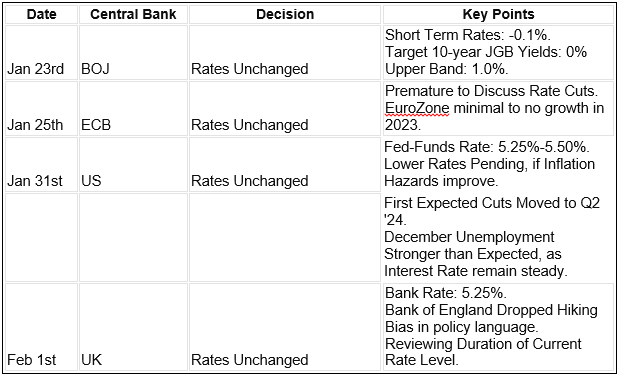

Central Banks (Jan – Feb 2024) decisions and their impact on FX Currencies

Central Banks (March 2024) decisions and their impact on FX Currencies

Examining global central bank decisions in March reveals a mixed landscape. While the BOJ implemented its first interest rate hike since 2007, other major central banks such as the ECB, BOE, and FED, have maintained their current interest rates, adopting a cautious strategy and awaiting clearer signals to potentially action rate reductions. Attention has now turned to the revisions in their policy language statements. Market expectations are leaning towards the FED initiating rate reductions in the second half of 2024, with possibly three rate cuts anticipated. Additionally, the Swiss National Bank surprised markets with a 25 basis point cut to 1.50%, marking the first major central bank to embark on a shift to a rate cut policy.

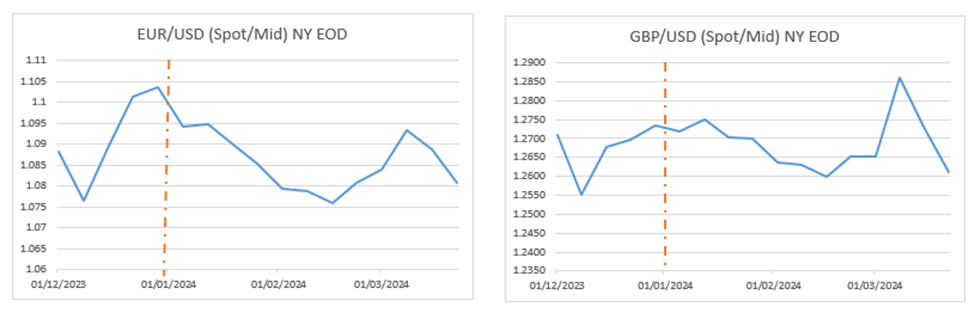

Policy statement adjustments and fluctuations in inflation metrics have significantly influenced currency movements, as evidenced in the analysis below. This analysis is a comparison of the performance of EUR/USD and GBP/USD from December 2023 to end of March 2024. The data points, sourced from TraditionData’s FX market data, represent the end-of-week and end-of-day FX Spot Mid-rates for both currency pairs.

Tracking volatility: A comparative study of EUR/USD and GBP/USD

In the Eurozone, where economic growth has been minimal, the EUR/USD and GBP/USD charts below show similar patterns from December 2023 until the end of March 2024:

In December 2023, there was expectation for US rate cuts to begin in March 2024, causing the USD to weaken against the EUR and GBP. Economic data showed inflation had declined, indicating a “soft landing” was again possible. However, this sentiment quickly reversed in January 2024, due to the resurgence of persistent US inflation, leading to a growing belief that the anticipated rate cuts might be postponed to May or June. Consequently, the USD appreciated in January 2024.

Similar patterns have emerged across the three major world economies and their respective Central Banks – the Federal Reserve in the US, the European Central Bank in the Eurozone, and the Bank of England in Great Britain – with regards to their monetary policies. The assessment of monthly economic data will play a central role in guiding their strategic shifts to rate reduction policies.

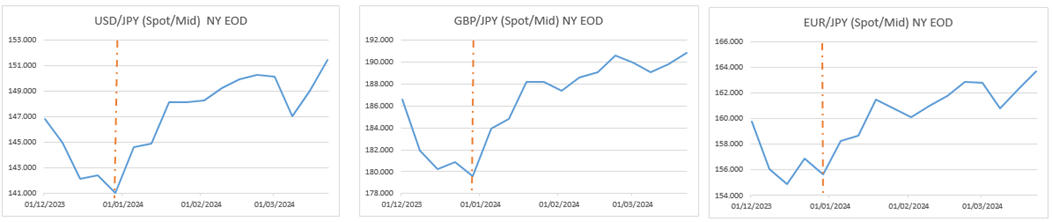

Tracking volatility: Currency correlations USD/JPY, EUR/JPY, GBP/JPY

Comparing USD/JPY, EUR/JPY and GBP/JPY, in the graphs below, we can see currency correlations based on policy language revisions and inflation marker changes:

In December 2023, we witnessed USD depreciation, supported by economic data, which indicated a decrease in inflation. Concurrently, the JPY saw appreciation, driven by statements from the BOJ, hinting at loosening Yield Curve Control (YCC) policies, along with the prospect of ending negative interest rates.

Conversely, in January 2024, USD appreciation gained momentum, driven by robust US inflation data, prompting a shift of market expectations towards prolonged higher US interest rates. This shift in sentiment suggested a postponement of future rate reductions, highlighting the data dependencies faced by these Central Banks.

Consequently, graphs for USD/JPY, EUR/JPY, and GBP/JPY depicted JPY appreciation against all three currencies in December, contrasting with JPY depreciation in January 2024. Despite the central bank's initial rate hike and modifications to their YCC policy in March, the JPY has continued to weaken against the USD, EUR, and GBP since January.

This comparative analysis underlines the dynamic nature of FX markets, influenced by factors such as policy language revisions, economic indicators, and shifts in market sentiment. It highlights the importance of staying informed to effectively navigate these volatile markets.

Navigating the FX landscape with TraditionData's comprehensive offerings

At TraditionData, we provide comprehensive FX market data, empowering market participants to navigate the complexities of the FX landscape. Our data encompasses a wide range of FX products including Spot, Deliverable and Non- Deliverable Forwards (NDFs), and FX Options, providing valuable insights into market trends and price movements.

FX market data

FX market data provided by TraditionData combines Inter-Dealer Broker (IDB) data with modelled analytics, offering insights into the Inter-Bank FX markets.

Our FX data serves a diverse range of customers, such as Global Banks, Corporates, Asset Managers, and Hedge Funds, who leverage TraditionData’s offerings for various purposes, including price discovery, hedging, risk management, and cash flow management.

Given the ongoing revisions in global monetary policies and the prevailing uncertainty in capital markets, accurate and unbiased FX market data is necessary to navigate currency volatility confidently.

TraditionData's FX and FX Options market data packages offer valuable resources to address the increasing need for high-quality financial market data, leveraging our expertise and comprehensive data offerings.

Author

Sal Provenzano

TraditionData

Sal Provenzano Is the FX Product Manager for the TraditionData business and has been tasked with shaping the future of the FX product range.