Michigan Consumer Sentiment November Preview: Is a confidence collapse coming?

- Consumer outlook forecast to be stable in November.

- Jobs, unemployment balanced against COVID-19 and closures.

- October's sentiment score was the best since March.

- Expected results will not impact markets or the dollar.

The second COVID-19 wave is upon the country and the overriding question is will consumers respond as they did in March and April?

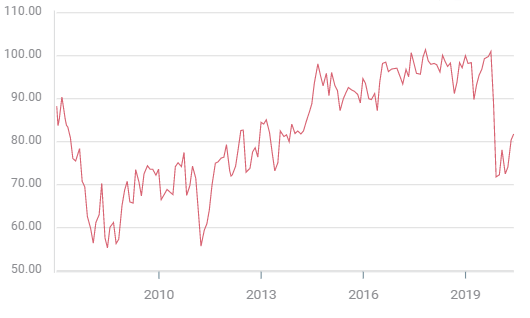

From February to March the Michigan Consumer Sentiment Index plunged from 101 to 71.8 as the nation closed its economy to fight the pandemic. February's score had been the second highest since the financial crash of more than a decade ago. The recovery to 81.8 in September was the highest point since the pandemic began but it is only one-third of the decline and returns the index to its range in 2012-2014.

Michigan's Consumer Sentiment Index is expected to rise to 82 in November from 81.8 in October.

Michigan Consumer Sentiment

Consumer attitudes in the United States are closely tied to the labor market and they are reflected in the Retail Sales and other consumption figures that represent 70% of US economic activity.

What has been the impact of the pandemic job loses on consumer and business spending?

Nonfarm Payrolls, Unemployment and Initial Jobless Claims

About half of the 22.16 million jobs lost from Nonfarm Payrolls in March and April, 54.4%, 12.05 million, have been recovered thorough October.

Last month 638,000 people joined the payrolls,slightly more than the 600,000 forecast but down from 672,000 in September.

Unemployment also improved dramatically falling to 6.9% in October from 7.9% prior and well ahead of the 7.7% prediction. Joblessness peaked at 14.7% in April.

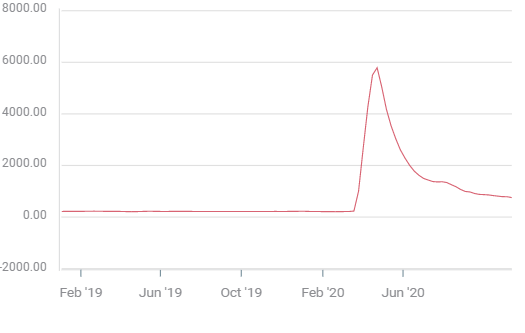

Initial jobless claims have had a similar though greater statistical recovery. From the peak on April 17 in the four-week moving average at 5,790.25 million, the average is down 87% to 755.25 thousand in the November 6 week. Continuing claims were 6.786 million in the latest week and 7.222 million the week before. They are down from 24.912 million the week of May 8.

Initial Jobless Claims, 4-week moving average

Before the improvement in claims should be accounted a success we must remember that in each week since March 13 more people have sought unemployment benefits than ever before in any single week in US history including the height of the 2008 financial crash when claims peaked at 665,000 in March 2009.

Unemployment benefits and a series of state and local extended benefits have cushioned the personal and economic impact of the lockdown induced jobs losses. But the economy remains short 10 million jobs and missing the consumption from that income.

Retail Sales and GDP

The plunge and restoration in consumer and business spending during and after the lockdown months is well known series of events.

Retail sales collapsed 22.9% in March and April. The Control Group fell 9.2%. The Durable Goods category, Nondefense Capital Goods, the business investment analog, shrank 7.9%.

Despite the unprecedented declines, all three of the measures have not just recovered their losses but have posted excellent overall increases for the entire seven month period from March to September.

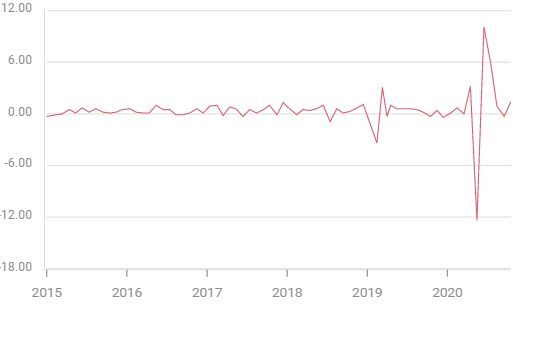

Retail Sales in September at 1.9% were almost triple their 0.7% projection. More importantly, they have averaged a 1.01% monthly increase from March through September. The Control Group, which enters the government's GDP calculation, rose 1.4% on a 0.2% expectation. It's seven month average is 1.27%.

Retail Sales Control Group

Nondefense Capital Goods, were up 1% in September and 2.1% in August. They have had a 0.5% monthly increase from March to September.

These consumption figures would be standouts in a normal economy, in one beset by unemployment they are astonishing. The resilience of consumer spending is reflected in GDP.

Economic growth in the third quarter jumped 33.1% after tumbling 31.4% in the pandemic marred second. The Atlanta Fed GDPNow model is running at 3.5% annualized growth in the fourth quarter.

Conclusion and the markets

The above rendition of economic statistics shows that in the current state of the labor market recovery US consumers retain their spending power. The pandemic has not changed the basic ingredient of the US economy.

The increase in COVID-19 diagnoses and hospitalizations on their own are unlikely to bring about a large drop in consumer spending or sentiment. Not to seem uncaring but the markets and the country have been here before and this time the economy is, at least so far, carrying on without additional major dislocation.

That of course may change.

If and when closures become more extensive and more widespread, beyond the mostly semi-opened restaurant sector, so that unemployment begins to rise, then consumer outlook and spending will feel the effect. When more communities are advised to stay home, as Chicago is starting Monday, or lockdown orders cripple non-essential activity, unemployment must gain, spending will fall and markets cannot fail to notice.

For the moment, consumer sentiment and by implication consumer spending, are stable. Until that changes, markets are unlikely to pay much attention.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.