Markets show early cautious consolidation but risk appetite remains low

Market Overview

There is a cautious consolidation across markets, as traders take stock once more following renewed fear of US protectionism and trade wars. Since Donald Trump fired Rex Tillerson there has been a renewed sense of reduced risk appetite that has taken over the markets. Fears of a ratcheting up of trade tensions has certainly played into this, with reports that the US could be ready to hit China with around $60n of trade tariffs. Certainly if this were to be the case, the world’s second largest economy would not take this lightly and be sure to respond in a reciprocal nature. Disputes are also not confined to the trade of goods, with a political dispute between the UK and Russia also taking hold after the UK has accused Russia of what amounts to be a chemical weapons attack on British soil. The UK has already unilaterally responded by a series of measures including the expulsion of 23 Russian diplomats. Will the western allies increase the pressure on Russia through sanctions and would Russia also respond in a belligerent manner? These are all factors that are driving a safe have shift once more. Treasury yields are falling back, whilst the yen is strengthening and equity markets are weaker. However, political factors tend to be short-lived drivers of markets and there still seems to be some uncertainties over forex market trends over the near to medium term. Once more, this morning as European traders take over there is an indecisive feel to market moves. Perhaps the next leg will be taken when there is more clarity on China trade tariffs from the US administration.

Wall Street closed broadly lower with the Dow dragged 1% lower and the S&P 500 -0.6% lower to 2749. Asian markets have though been mixed overnight with the Nikkei +0.1% higher, and European indices are also starting a touch cautiously higher. In forex, there is a mixed outlook for the dollar, with the yen and sterling stronger, whilst the commodity currencies are a touch weaker. In commodities, gold is trading around the flat-line, as is oil which looks to stabilise the selling of the last few days.

Early in the European session traders will be watching out for the monetary policy decision of the Swiss National Bank at 0830GMT, with the expectation that the SNB will continue to hold rates steady at -0.75%. Beyond that there is a series of Fed surveys for the US with the New York Fed Manufacturing (Empire State) at 1230GMT expected to improve to +15.0 (from +13.1 last month) and the Philly Fed Business Index also at 1230GMT expected to slip slightly to a still very strong +23.0 (from +25.8 last month). US Weekly Jobless Claims are at 1230GMT and are expected to again be very low at 226,000 (231,000 last week), whilst the NAHB Housing Market Index at 1500GMT is expected to be 71 (72 last month).

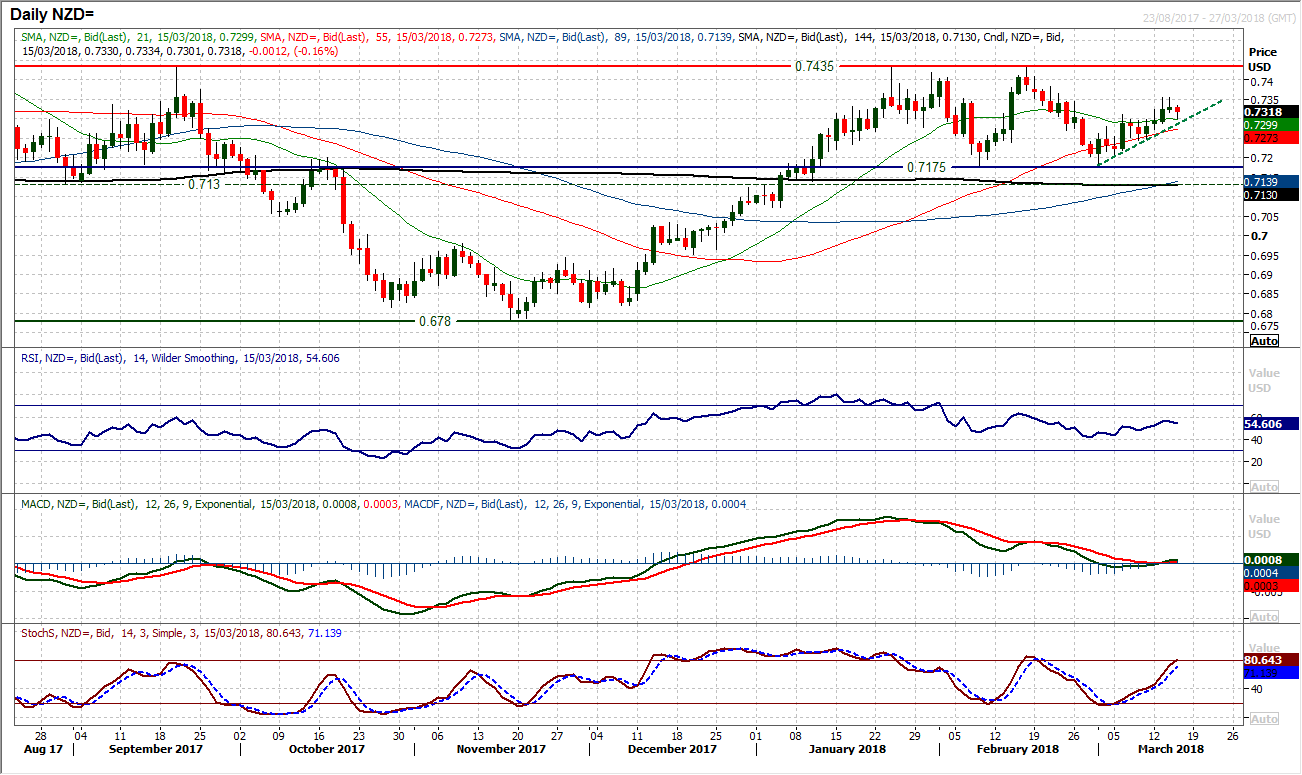

Chart of the Day – NZD/USD

The antipodean commodity currencies (Aussie and Kiwi) have been strengthening recently and this has driven a recovery move against the dollar. For the Kiwi/Dollar this recovery from the key support at $0.7175 is now developing a series of higher lows and higher highs over the past couple of weeks in an uptrend formation that suggests weakness is a chance to buy. The move has now pushed into the upper half of a two month trading range between $0.7175/$0.7435. The bulls will certainly be gaining confidence from the Stochastics accelerating higher with upside potential and now the MACD lines completing a bull cross on the neutral line. The recent uptrend support comes in at $0.7290 today whilst there is a good basis of support around the breakout of last week’s series of highs between $0.7295/$0.7310. This suggests that this is now a good area to look for near term longs. The Kiwi has dipped slightly on a weaker than expected GDP read overnight but technically this looks to be a buy opportunity around the support band. There is further support of the higher low at $0.7245. The hourly chart shows strong configuration on hourly RSI and MACD lines, which are configured to suggest corrections are a chance to buy now.

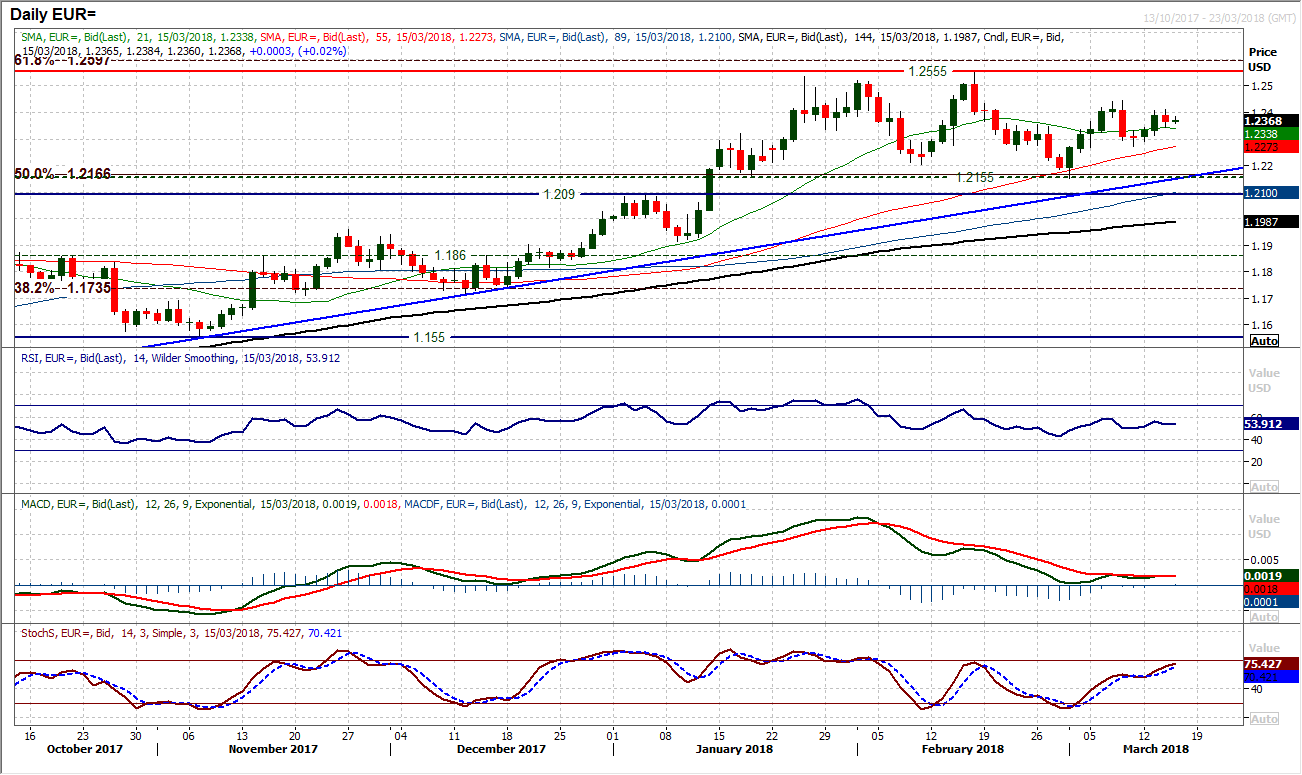

EUR/USD

The euro slipped yesterday on the re-iterated attempts by Mario Draghi to talk down the single currency. However, the subsequent pressure on the dollar meant that little real direction was garnered from the session. The mildly negative one day candlestick formation has though seen the market roll over at $1.2412 which is under the $1.2445 key near term resistance and maintains a rather ranging look to the market still. Across the medium term outlook the market is trading in a 400 pip band $1.2155/$1.2555 and with the momentum indicators slightly positively biased there is still a tendency to buy into weakness. The higher low at $1.2270 is adding to support and the market is trading above the rising moving averages. The hourly char shows a band of support $1.2345/$1.2360 now for today’s session to build from. The balance of indicators favour a test higher.

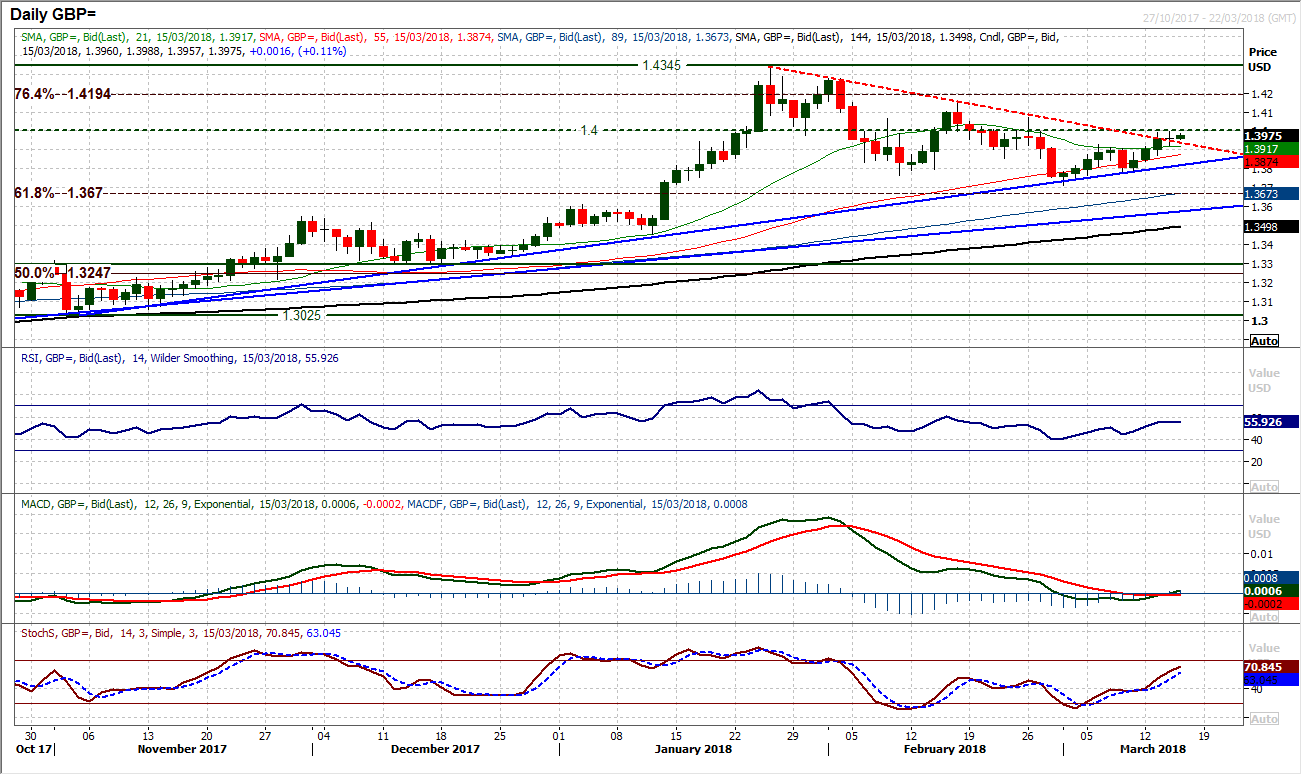

GBP/USD

As with EUR/USD, there is a mild positive bias on Cable pulling the market higher, but there needs to be more conviction in for the bulls to be in real control. The market has now broken the downtrend with the market continuing to eye the psychological resistance at $1.4000. However in the past couple of months the market has seen $1.4000 as a pivot area, especially on a closing basis with several intraday failures. This adds importance to a decisive move clear of the resistance. Momentum indicators continue to improve, with the MACD lines in the process of crossing higher around neutral, whilst the Stochastics and RSI are on improving trends above neutral. Weakness is being bought into and the support of the uptrend since November comes in at $1.3820 today. The near term breakout above $1.3930 is now a basis of support which was tested and held during yesterday’s session. Above $1.4000 opens $1.4070 initially, with $1.4145 the next key reaction high.

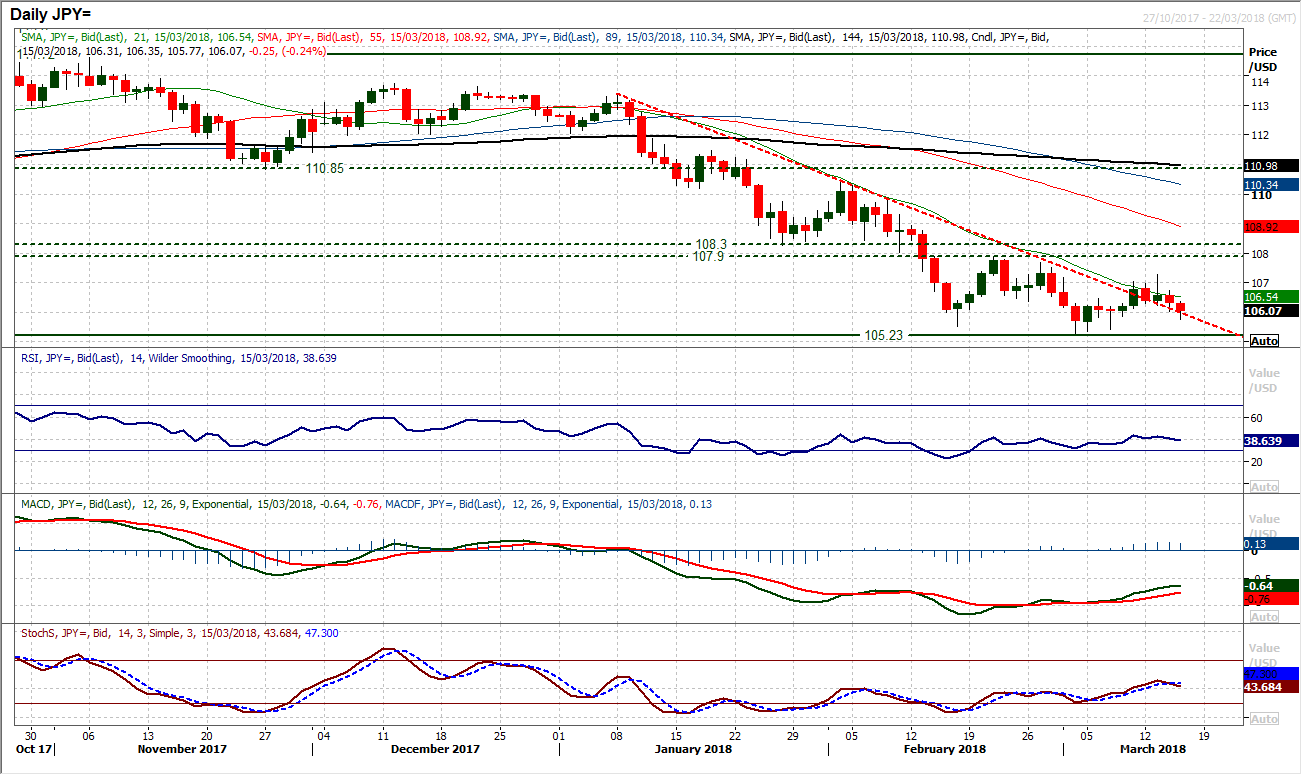

USD/JPY

As renewed concerns over trade wars have arisen, the yen has strengthened again. Subsequently the medium term negative outlook on Dollar/Yen has re-asserted once more. After Tuesday’s failed recovery, a negative candle formation was seen yesterday and a continuation lower today puts renewed pressure to the downside. The momentum indicators have fallen over once more, with the RSI falling into the 30s again, Stochastics crossing lower and the MACD lines also set to top out. The hourly chart shows renewed negative configuration, trading below all moving averages, whilst the near term pivot at 106.35 which had been supportive has been broken and now become a basis of resistance, whilst the reaction high at 107.30 now looks to be another key lower high in place. The market is now selling into near term strength and looks set up to test the old support around 105.50, with the March low at 105.23 and the Average True Range of 83 pips.

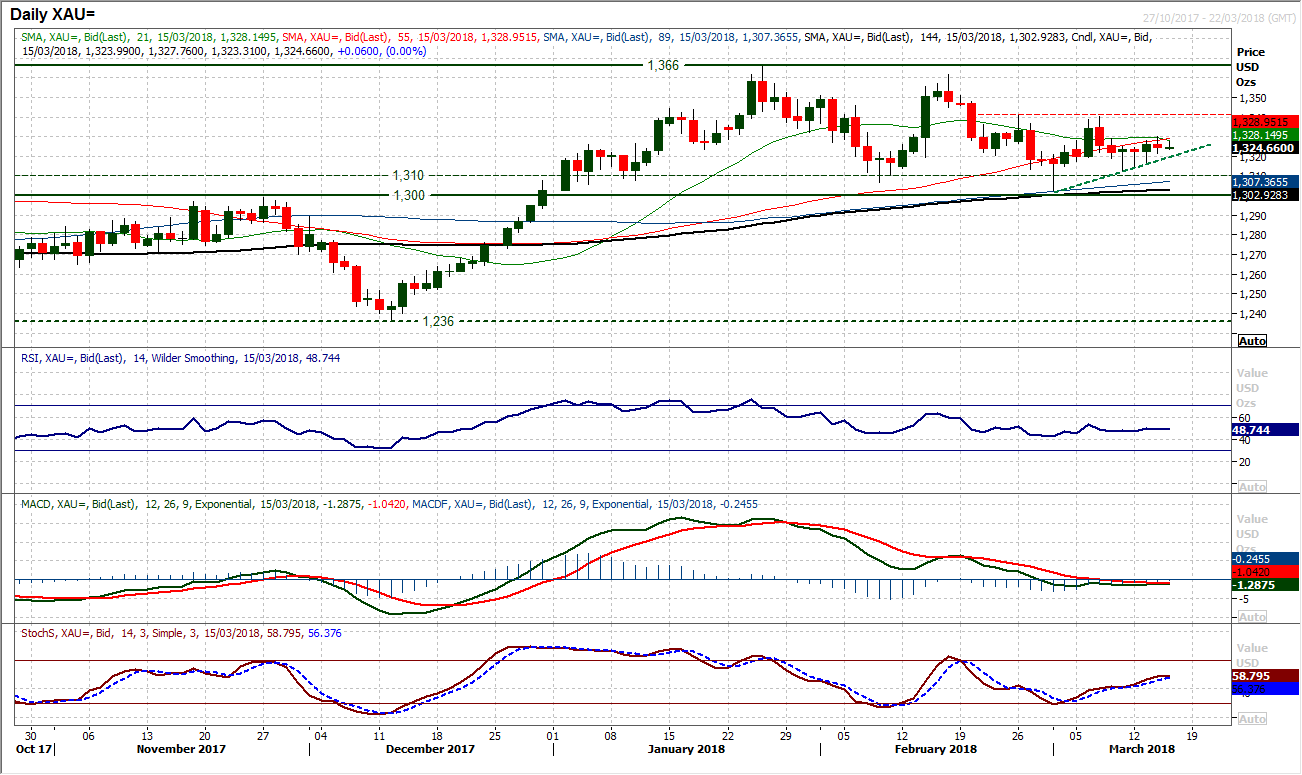

Gold

It is interesting to see the continued lack of any direction that has taken hold in the past few sessions, despite the swings in market sentiment. With risk appetite reducing again and safe haven flows renewing, gold has still barely budged. There is the slightest of positive biases but little, if any, decisive direction to speak of. This comes as once more a very small bodied candle was formed yesterday, whilst the MACD and RSI momentum indicators become almost entirely flat-lined. The market is being supported above the recent lows between $1313/$1316 but there seems to be little appetite to bid up the gold price for a test of the key near term resistance at $1341. A catalyst is certainly needed (seemingly something more than renewed fears of a trade war, or a potential escalation of a dispute between western allies and Russia). The hourly chart shows near term oscillation on RSI between 30 & 70 possibly being tightened further to between 40 & 60. Initial resistance at $1329/$1330.

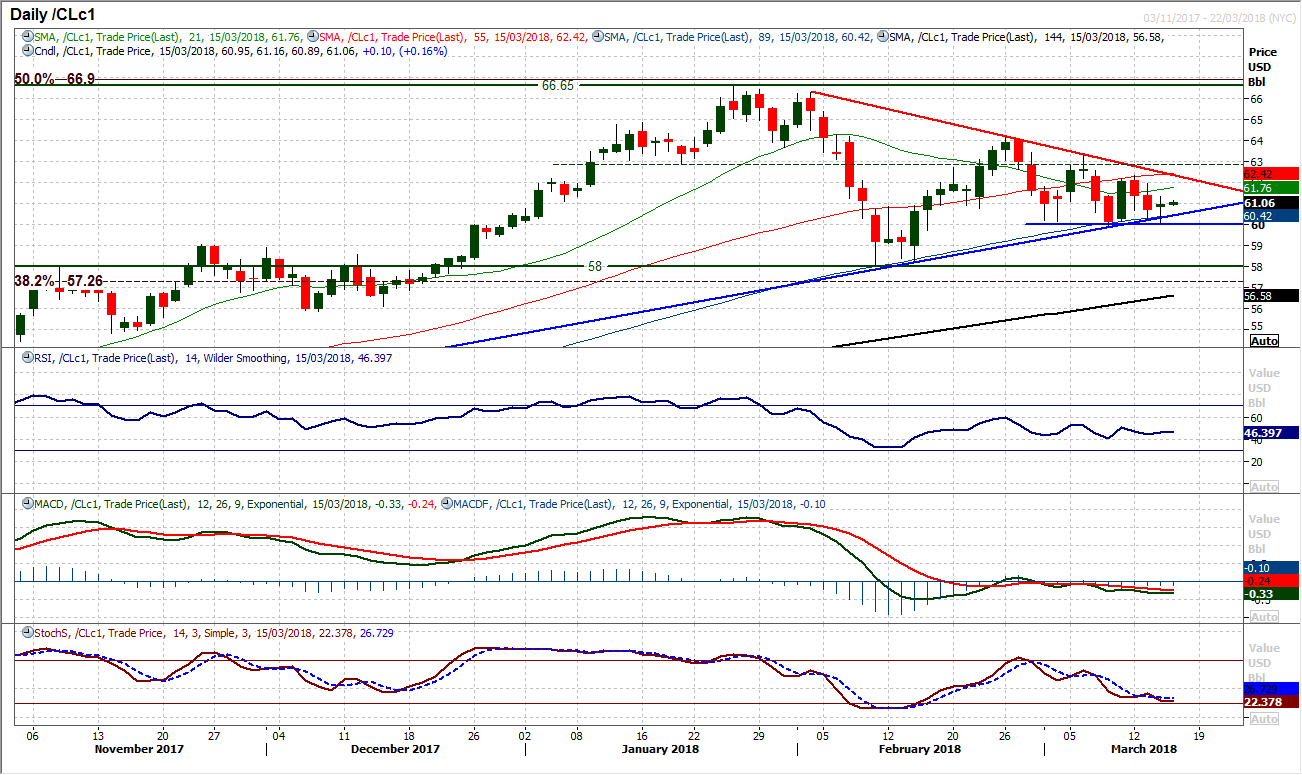

WTI Oil

A rally into the close last night has helped to improve the support of the uptrend since September and the bulls continue to hold under the strain of a corrective move in the past few sessions. The mixed data in the EIA crude inventories resulted in a mild gain on the day and has prevented further pressure on the support that is in place at $59.95. However, concern to the downside increases with the momentum indicators which are dropping away, as the Stochastics look increasingly negatively configured and MACD lines begin to find traction falling below neutral. The intraday rallies are increasingly being sold into, with yesterday’s reaction high at $61.35 being another lower high which adds to the recent run of failed rallies. A confirmed break of the support at $59.95 (on a closing basis) would now complete the downside break from of a descending triangle and would then imply a correction back to test the key February low at $58.05. Resistance at $62.35 is increasing in importance.

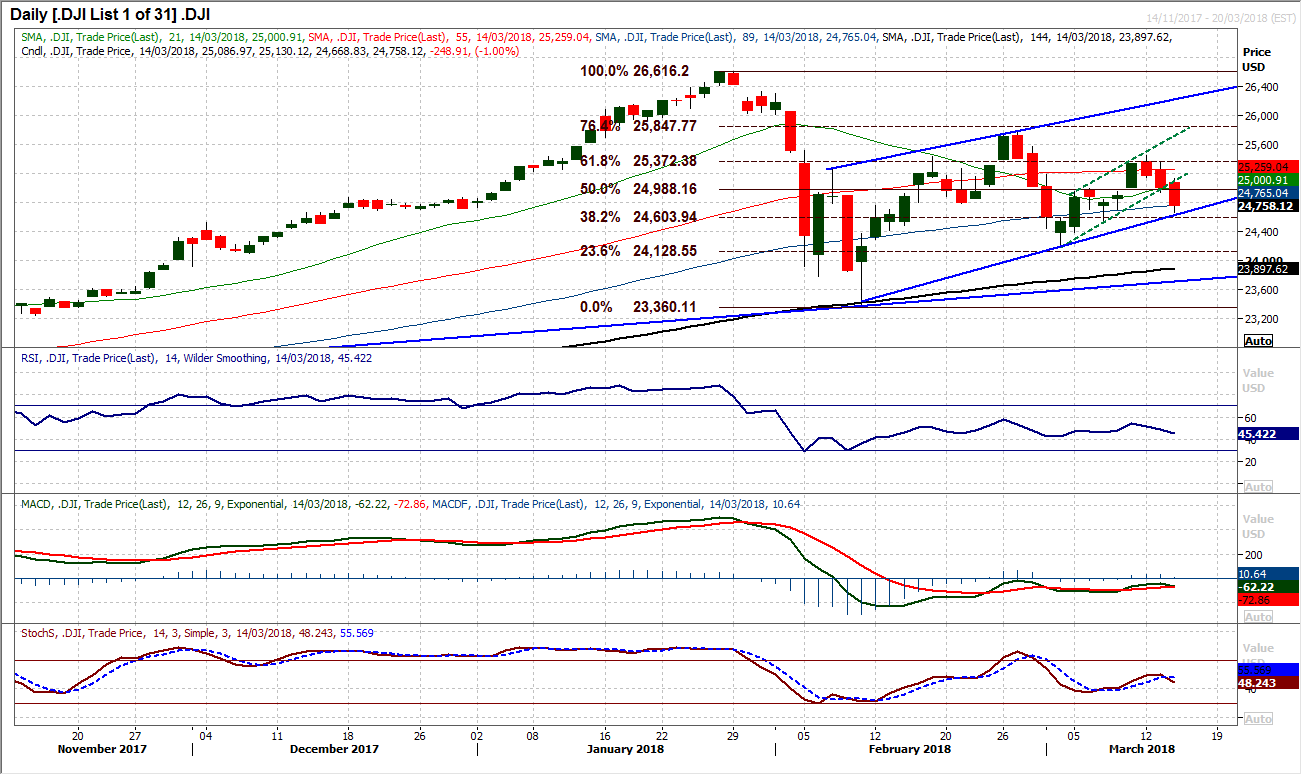

Dow Jones Industrial Average

A third solid negative session for the Dow has now broken the mini-recovery uptrend that had been forming in the past days. This move now raises the issue of whether there will be another retreat back towards the early March low at 24,218. Momentum indicators are now turning into reverse gear in the near term with the RSI falling below 50, the Stochastics crossing lower around 50 and the MACD failing under neutral. This does not bode well for the near term outlook with a retreat towards the 38.2% Fibonacci retracement at 24,604 now imminently on the cards, with the next reaction low at 24,545 that is protecting the 24,218 low. Judging how the Fib retracements have been key turning points for the Dow, the 50% Fib level at 24,944 is a basis of resistance now. The market is also testing the recovery uptrend channel support and a closing breach would add to the increasingly corrective outlook that is taking hold. The hourly chart shows resistance between 24,950/24,500.

Author

Richard Perry

Independent Analyst