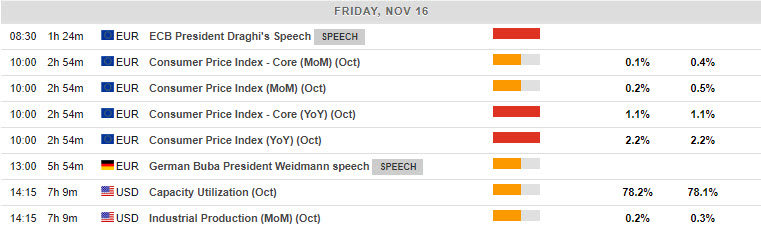

Macro Events & News

FX News Today

European Fixed Income Outlook: The Dec 10-year Bund future opened at 160.54, down from a close of 160.81 on Thursday. The 10-year cash yield is up 0.6 bp at 0.363% in early trade, versus losses of -0.2 bp and -0.4 bp respectively in 10-year Treasury and JGB rates. Gilts led a broader rally in core EGB markets yesterday as the fate of PM May and with her, the Brexit deal hung in the balance, but while both are by no means secured yet, it seems markets are steering into calmer waters going into the weekend. Sterling came back from lows overnight and Gilts are likely to underperform today. UK stock futures meanwhile are actually moving higher, despite the consolidation in Sterling. ECB President Draghi and Bundesbank President Weidmann are both scheduled to speak today, the calendar has plenty of Italian data, but focuses on the final reading of Eurozone HICP inflation for October, which is expected to be confirmed at 2.2% y/y.

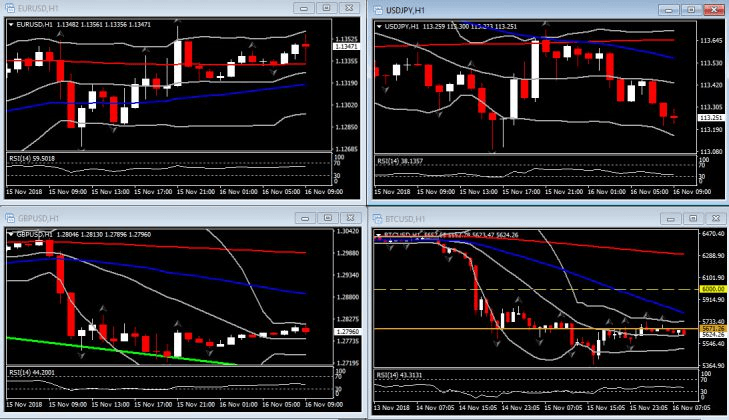

FX Update: The Dollar has traded broadly softer while the Yen has been an outperformer as U.S. equity futures tipped lower after positive Wall Street session yesterday, and amid a flagging sentiment across Asian bourses, even though Chinese markets managed gains. A senior Trump administration official cited by Reuters said that China’s written response to trade demands is unlikely to trigger a breakthrough at upcoming talks between Trump and Xi. USDJPY ebbed back to a low of 113.21, nearing yesterday’s nine-day low at 113.09. EURJPY, AUDJPY and other yen crosses have also declined. EURUSD, meanwhile, has lifted back to the mid 1.1300s after failing to sustain losses below 1.1300 yesterday. Cable, which yesterday posted its biggest daily decline since October 2016 in making a 17-day low at 1.2723, has found a toehold, lifting back to near 1.2800 as Prime Minister May showed tenacity in the face of senior resignation and broadsided criticism of her Brexit plan. More political uncertainty and dramas lie ahead in the UK. Most political punditry seem to think May would survive a confidence vote, if it came to that, while the prospects for the Brexit plan to pass at parliamentary vote, which will take place in early December, is looking uncertain.

Charts of the Day

Main Macro Events Today

EU Final CPI – Eurozone CPI is expected be confirmed at 2.2% y/y. Core inflation remains considerably lower at just 1.1% y/y, but as Draghi started to highlight underlying inflation is starting to move higher as wage growth is picking up amid very tight labour markets.

US Industrial Production – The week rounds out with industrial production projected to rise 0.2% in October, after a 0.3% reading in September, while capacity utilization should be steady at 78.1% in October.

ECB President Draghi and Bundesbank President Weidmann are both scheduled to speak today.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in