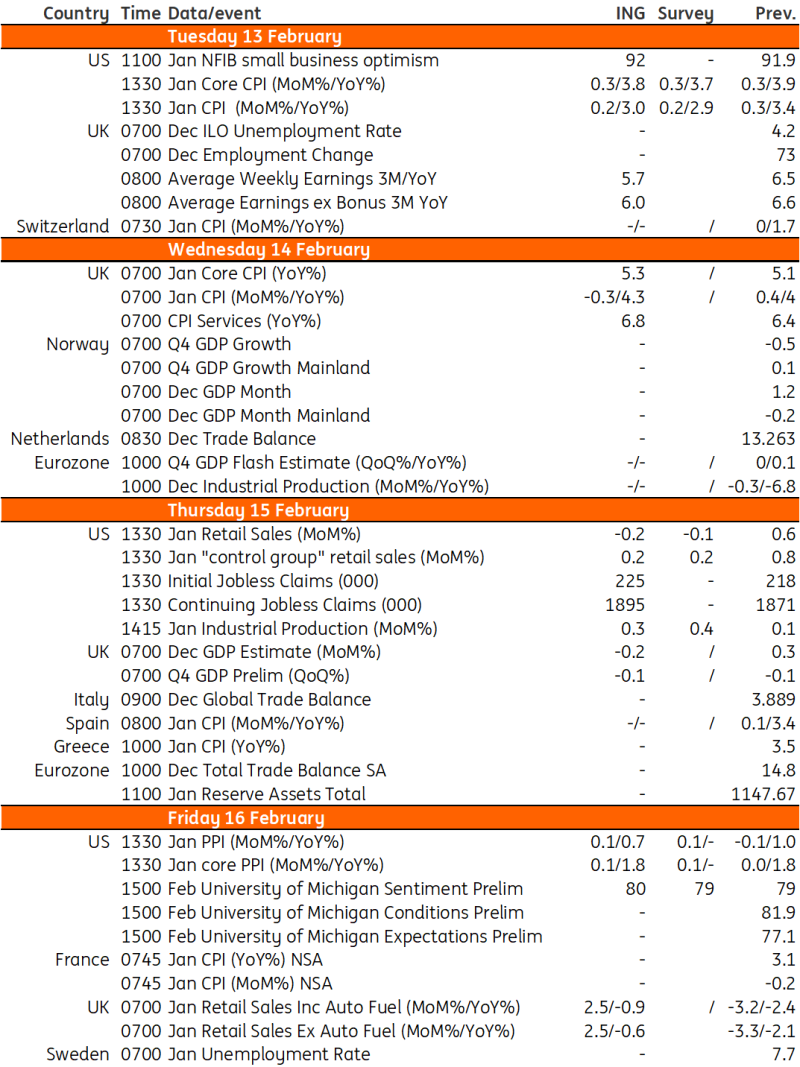

Key events in developed markets next week

The main data highlights in the US next week will be the release of core inflation data along with retail sales, which are expected to come in soft given auto sale numbers. In the UK, keep an eye out for a flurry of data releases including services inflation and wage growth - two driving factors for the Bank of England's next monetary policy decision.

US: We are looking for a 0.3% MoM increase in the core inflation rate

Strong jobs and growth data have diminished the chances of a March Federal Reserve interest rate cut significantly – and even May is no longer the odds on certainty it looked two weeks ago. While officials are still open to the idea of loosening monetary policy, they have pushed back against the chances of an imminent move. We suspect that the Fed recognises its credibility was damaged by its "inflation is transitory" assertion in 2021 only to have to rapidly reverse course with significant rate hikes through 2022 and 2023. The last thing the Fed wants to do is get it wrong again at a key turning point, loosen too soon, too quickly and reignite inflation pressures. It wants to be sure that the data is fully consistent with inflation returning to 2% and staying there.

The Fed’s favoured inflation measure, the core PCE deflator, is already tracking at the appropriate rate and labour market inflation pressures are easing, based on declining quit rates and the slowing employment cost index. However, the Fed would ideally like to see a bit more slack in the jobs market, created by a moderation in growth rates – the “soft landing”. This week’s numbers could point in this direction, with retail sales and industrial production as the activity highlights while consumer price inflation is also scheduled for release. Starting with CPI, it has been posting more rapid month-on-month increases than the PCE deflator, largely due to the heaving weighting of housing and vehicles in the basket of goods and services used to calculate the inflation rate. Rents are slowing in the open market, but the way the series is constructed within the CPI report means those movements take a long time to show up in official data. Manheim used car auction prices suggest vehicle prices will be a depressing factor on January inflation. We are looking for a 0.3% MoM increase in the core inflation rate with the risks skewed slightly in favour of a 0.2% outcome rather than a 0.4% increase.

Retail sales are likely to be soft, given that auto sales numbers already published were poor. Bad weather has certainly played a part, but 20+ year high borrowing costs for credit cards, car loan and personal loans are not helping. There is also growing evidence suggesting that pandemic era accrued excess savings will be supportive for spending. Meanwhile, industrial production is likely to be lifted due to strong utilities demand, but manufacturing is likely to stay subdued given the ongoing contraction signalled by the ISM report.

At the January FOMC meeting Chair Jerome Powell acknowledged that monetary policy is well into “restrictive territory” and it will be “appropriate to dial back” on that at some point this year. We expect that May will be the starting point, by which time we think ongoing subdued core inflation measures will give the central bank the confidence to cut rates. We see the policy rate getting down to 4% by the end of this year and 3% by mid-2025. This will merely get us close to neutral territory – the Fed’s view is that 2.5% is likely the long-term average. If the economy does enter a more troubled period, such as through banking stresses, there is scope for much deeper cuts than we are forecasting.

UK: Services inflation and wage growth likely to remain sticky

Next week we’ll get a huge amount of data on the UK, some of which will have a bearing on when the Bank of England cuts rates. Of greatest consequence for the rate outlook will be services inflation and private-sector wage growth. The former is likely to notch higher, in part because of some volatile moves in air fares. The latter is likely to drop pretty noticeably again, which in part reflects the recent cooling in the jobs market. But both services inflation and wage growth remain too high for the BoE’s liking, and are likely to remain sticky in the first quarter.

We’ll also get growth figures this week, and it looks like the plunge in retail sales in December might have been enough to nudge the economy into another very slight contraction. That’ll mark the second such contraction and will spark lots of headlines about recession, but the reality is that this is a recession in name only. Indeed, we think the outlook for the UK economy is brightening and we’ll see a return to modest but nevertheless positive growth figures this year. However, these GDP figures – particularly the volatile monthly version – are not going to be what determines the timing of the Bank of England's first rate cut.

Key events in developed markets next week

Source: Refinitiv, ING

Read the full analysis: Key events in developed markets next week

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.