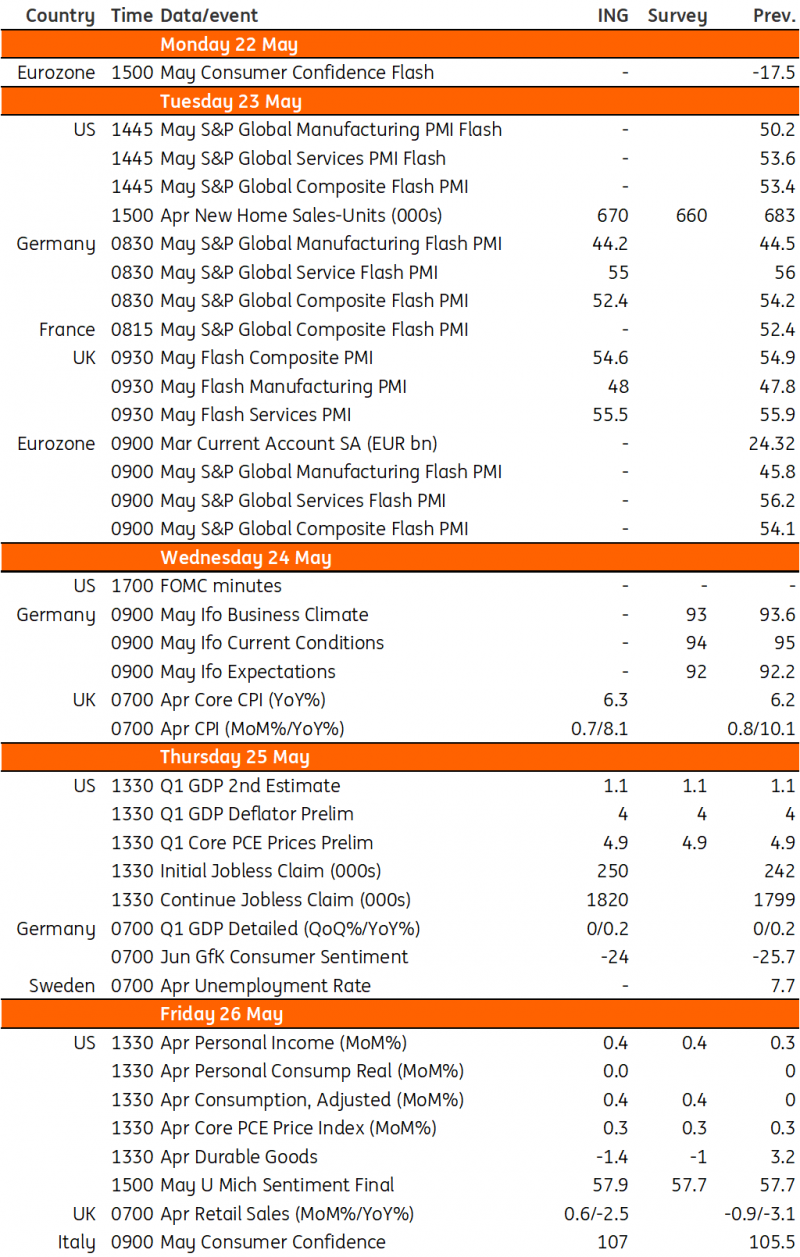

Key events in developed markets next week

With some hawkish comments from Federal Reserve officials and the Fed's favoured measure of inflation looking set to remain elevated, a pause at the June FOMC policy meeting is not a foregone conclusion. For the UK, inflation data next week will heavily determine whether policymakers pause the tightening cycle.

US: Market on edge about a possible June rate hike

Market interest rate expectations have shifted higher over the past week thanks to a combination of favourable headlines offering hope that a default-averting deal to raise the debt ceiling can be agreed upon this coming week, plus some hawkish comments from Federal Reserve officials that mean a pause at the June FOMC policy meeting isn’t a foregone conclusion. These same two issues will dominate market thinking this coming week. Politicians have talked about the possibility that a vote could be held to raise the debt ceiling as early as next week. This would be a very positive outcome, but given the personalities of the people involved, we must remain cautious until the deal is signed and approved. If talks break down, this would lead to a rapid deterioration in market sentiment.

Data includes GDP revisions, the minutes of the last FOMC meeting, and the Fed’s favoured measure of inflation: the core personal consumer expenditure deflator. This inflation measure looks set to remain elevated, which could keep the market on edge about a possible June interest rate hike. Nonetheless, the activity backdrop continues to soften with real consumer spending set to come in flat on the month in April. Recession risks remain high given the rapid tightening in lending conditions in the wake of recent bank failures and we still see the potential for lower interest rates before the end of the year.

UK: Inflation data to heavily determine BoE’s June decision

Next week’s UK inflation data is one of two such releases ahead of the June Bank of England meeting, and will heavily determine whether policymakers pause the tightening cycle, as we expect, or hike by a further 25 basis points. More specifically, this hinges on whether we get an unexpected surge in services inflation, which otherwise looks like it’s close to a peak.

Wage pressures appear to be abating, though slowly, while lower gas prices are good news for the hospitality sector, which represents a large proportion of the recent increase in overall services inflation. We’ll also be watching retail sales which may partially rebound after a very wet March depressed spending, and in general, the prospect of reduced real wage pressure and improving consumer confidence suggests the worst is behind us for the sector.

Source: Refinitiv, ING

Read the original analysis: Key events in developed markets next week

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.